For the latest standardized performance and holdings of Sprott ETFs, please visit the individual website pages: SETM, COPP, COPJ, URNM, URNJ and METL.

Key Takeaways

- A New Kind of Commodity Supercycle:1 The emerging bull market2 is not repeating past cycles, and is being driven by deglobalization, fiscal dominance and the global push for energy, infrastructure and strategic, domestic supply chains.

- Hard Assets Are Becoming Strategic: Governments are prioritizing resource security and domestic supply chains. As a result, critical minerals and metals are being repriced for their strategic importance, not just supply and demand.

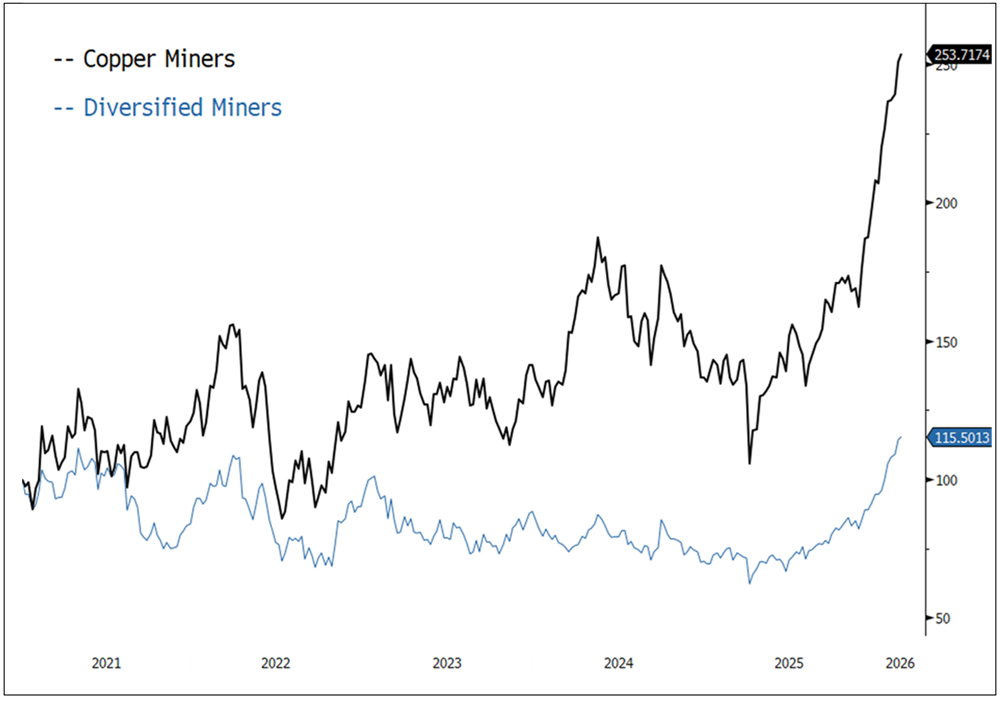

- Copper Is Powering the Next Growth Phase: Copper has emerged as a central metal for power grids, data centers and electrification. Its tighter supply and strategic role are helping copper producers outperform diversified miners (see Figure 2A below).

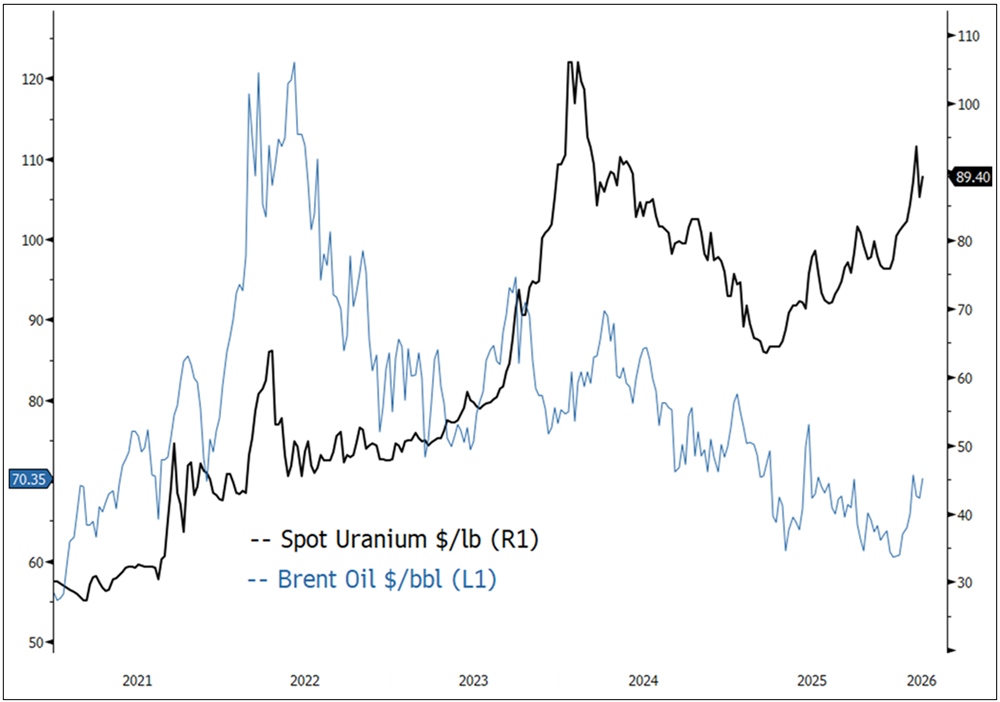

- Uranium Is Rising on Energy Security: Nuclear power is gaining momentum as countries seek reliable, secure baseload energy. This shift is strengthening uranium demand relative to traditional energy sources like oil.

- Targeted Exposure Likely Matters More Than Ever: Broad commodity exposure may lack focus on the critical materials currently leading this cycle. Investors are increasingly focusing on companies tied directly to critical materials and structural demand trends.

This Commodity Cycle Seems Fundamentally Different

Commodity markets entered 2026 with a decisive change in tone. After years of shrinking representation in global portfolios, commodities and resource equities have broken out above multi-year trading ranges, an action that, in our view, marks the developing stages of the new commodity bull market.

Hard assets are being elevated to strategic necessities rather than cyclical inputs.

This cycle, however, looks fundamentally different from prior periods. It is not a replay of the 2000-2014 “build China” era, nor of the inflation and supply-shock–driven commodity boom of the 1970s. Instead, today’s growing commodities market is being shaped by a far more structural set of forces: Accelerating deglobalization, entrenched fiscal dominance, and a technology-driven surge in demand for secure electricity and strategic resources. As trade fragments and geopolitical risk rises, governments are prioritizing sovereignty, resilience and control over critical supply chains. This shift is elevating hard assets—particularly critical materials tied to electrification, defense and advanced infrastructure — to strategic necessities rather than cyclical inputs.

Policy, Deglobalization and the Hard Assets Trade

At the macro level, the current setup is defined by the interaction between fiscal expansion and monetary debasement, reinforced by a fragmenting global order. On the fiscal side, governments are deploying large-scale spending programs to support domestic infrastructure, power generation, grid resilience, defense, and industrial reshoring. On the monetary side, persistent deficits and rising debt burdens have entrenched fiscal dominance, limiting central banks’ ability to maintain real purchasing power and embedding a structural bias toward financial repression.

This cycle favors critical materials tied to electrification, power generation and energy security.

Historically, this combination of expansionary fiscal policy, accommodative monetary regimes and geopolitical fragmentation has been one of the most consistent drivers of sustained outperformance for hard assets. In today’s world, where trade, capital and commodity flows are increasingly weaponized, physical resources such as critical minerals, energy metals and precious metals are being repriced not just by supply and demand but also by security, sovereignty and strategic value.

Nearly all resource commodities and related equities have begun 2026 on a robust footing. However, there is notable differentiation within the space. The movement is not broad-based; it is concentrated in materials tied to electrification, power generation and energy security rather than the bulk commodities (or “bulks”) that dominated the prior cycle.

A Clear Internal Rotation Within Resources

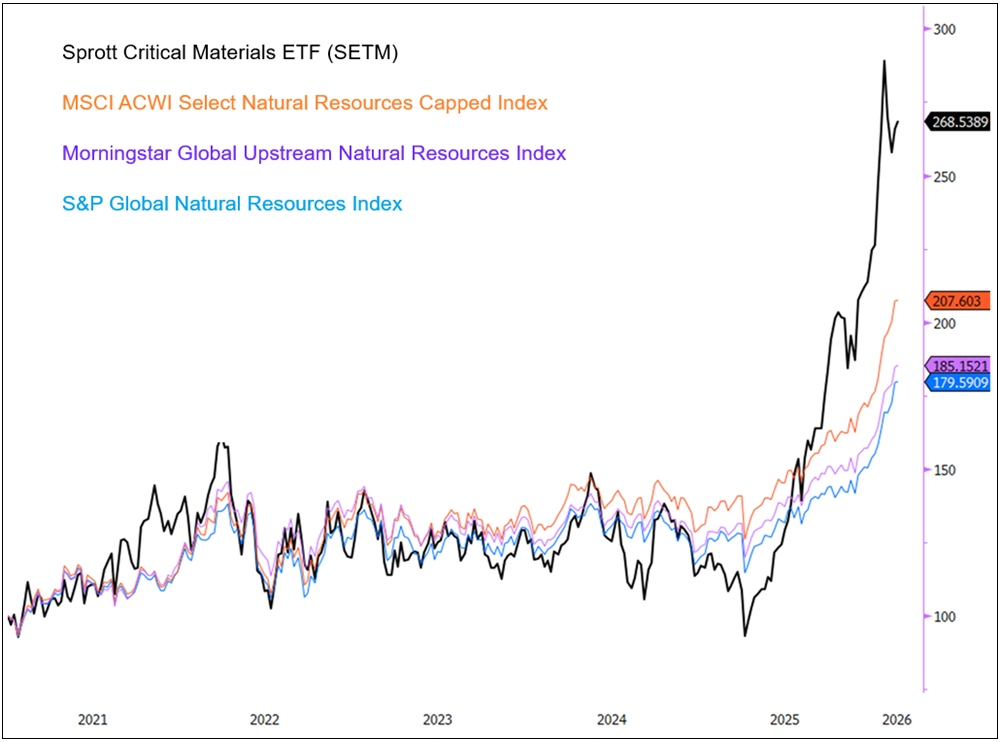

This internal rotation is evident in performance. Over the past year, the critical materials sector has significantly outperformed the traditional natural resource equities sector. For example, the Sprott Critical Materials ETF (SETM) has delivered a substantially higher return than broad natural resource benchmarks, as highlighted in Figure 1. From the April 8, 2025, lows, the marked relative performance trend between critical materials1 and traditional natural resources2 appears to be in the early stages of a structural shift.

The composition of these exposures helps explain the divergence. SETM is tilted toward commodities central to today’s economic priorities, including copper, uranium, lithium, rare earth elements, and silver. In contrast, broad natural resource indices remain heavily weighted toward large, diversified miners, large integrated energy companies and other broad economic sectors, such as chemicals, paper and forest products, packaging and agriculture, which were essential to the last China-led cycle.

Figure 1. Critical Materials versus Traditional Natural Resources in Total Returns 3 (1/1/2021 - 2/18/2026)

Source: Bloomberg. Data as of 2/18/2026. S&P Global Natural Resources Index tracks companies engaged in the ownership, management, or production of natural resources, including energy, metals and mining, and agriculture-related businesses, MSCI ACWI Select Natural Resources Capped Index (USD) represents companies in the energy, metals and mining, and agriculture sectors, with issuer weights capped to limit concentration, and Morningstar Global Upstream Natural Resources Index measures the performance of companies primarily involved in upstream natural resource activities, such as exploration, development, and production of energy, metals, mining, and agricultural inputs. Past performance is no guarantee of future results.

Copper Over Bulks: Powering the Next Growth Phase

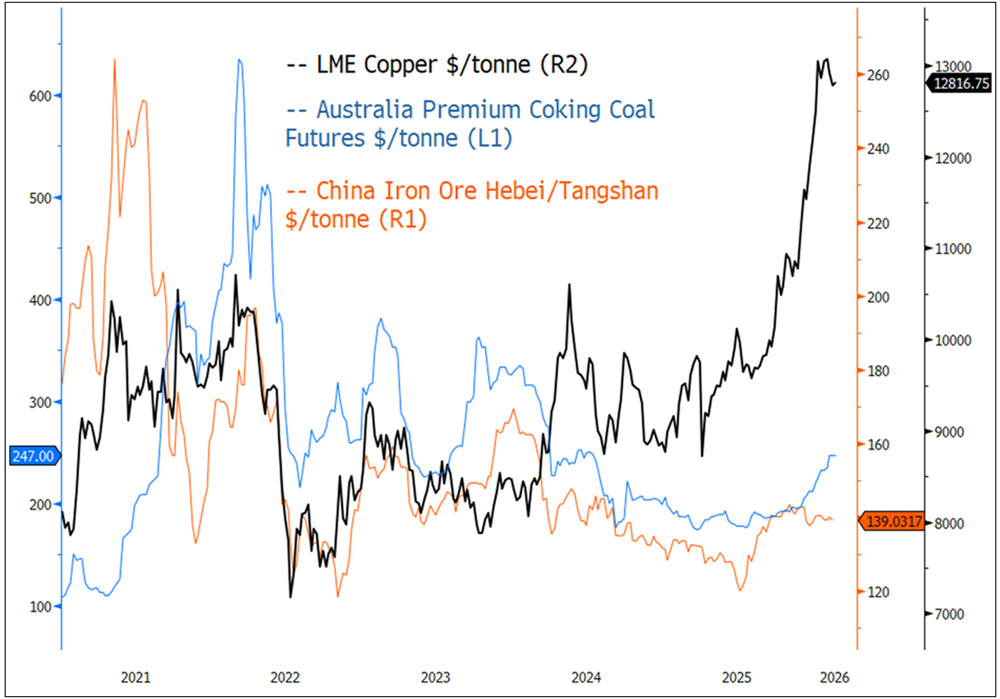

One of the clearest expressions of this shift is the relative performance of copper versus bulk commodities. During the 2000s, iron ore and metallurgical coal benefited from the construction of scores of cities in China and the infrastructure required to support them. That demand profile is unlikely to be repeated.

Copper’s supply-demand balance is structurally tighter and more strategically important than that of traditional construction-linked commodities.

This commodity cycle’s growth engine looks different. The world is not building scores of new cities; it is creating thousands of data centers, expanding high-capacity transmission networks, upgrading grids and electrifying transportation and industrial processes. Copper sits at the center of nearly every one of these trends. As a result, many copper-focused producers have increasingly outperformed large, diversified mining companies, whose earnings remain more closely tied to bulk commodities.

It took time for markets to recognize this fundamental shift. However, the relative performance now reflects a growing consensus: Copper’s supply-demand balance is structurally tighter and more strategically important than that of traditional construction-linked commodities. In Figure 2A, we highlight the relative performance of LME Copper versus iron ore and metallurgical coal. In Figure 2B, we highlight the relative performance of a basket of four copper miners versus a basket of four large, diversified miners.

Figure 2A. Copper vs. Bulk Commodities (Iron Ore and Met Coal) (2021-2026)

Source: Bloomberg. Data as of 2/18/2026. London Metal Exchange (LME) Copper futures contracts represent the market price of Grade A copper cathode, quoted in U.S. dollars per metric tonne, and are widely used as the global reference price for physical copper transactions. Australia Premium Coking Coal Futures Index reflects the market price of premium coal exported from Australia. China Iron Ore Hebei/Tangshan Index tracks domestic iron ore concentrate prices in Tangshan, Hebei Province, commonly referencing ~66% Fe iron ore concentrate, used as a key indicator of supply demand conditions in China’s primary steelmaking hub. One cannot invest directly in an index. Past performance is no guarantee of future results.

Figure 2B. Copper Miners vs. Diversified Miners in Total Returns (2021-2026)

Source: Bloomberg. Data as of 2/18/2026. Copper Miners is an unweighted average of four copper miners, Freeport, Teck, Antofagasta and Hudbay,4 representing the four largest copper miners, as measured by market capitalization, with ≥ 50% copper exposure. Diversified Miners is an unweighted average of four diversified miners, BHP, Rio Tinto, Anglo American and Vale, representing the four largest diversified miners as measured by market capitalization. There is no guarantee the companies were or will be profitable. Past performance is no guarantee of future results.

Uranium Versus Oil: Energy Security Redefines Leadership

Another contrast can be seen between energy metals and conventional hydrocarbons. Crude oil markets remain characterized by ample supply and a long-term decline in their intensity of use per unit of global GDP (gross domestic product). By contrast, uranium is entering this commodity cycle with constrained supply and rapidly improving demand fundamentals.

In a world increasingly defined by energy security concerns, nuclear power remains the most secure energy source.

The resurgence of nuclear power is being driven less by environmental considerations than by national energy security. As geopolitical risk rises, reliable, secure baseload power has moved to the top of the energy policy agenda. Nuclear energy, which is high density, dispatchable and domestically securable, sits at the apex of the energy-security and national-security hierarchy. Utilities are rebuilding long-term uranium contract coverage, governments are extending reactor lifespans, and new capacity is being planned across multiple regions.

In a world increasingly defined by energy security concerns, nuclear power remains the most secure energy source. Furthermore, recent geopolitical developments in Venezuela and Iran highlight the growing risk of crude oil interdiction. As competing global power blocs develop, securing one’s domestic energy supply while denying one's adversary access to energy can often serve the same strategic end.

Figure 3. Uranium vs. Crude Oil (2021-2026)

Source: Bloomberg. Data as of 2/18/2026. Spot uranium is the current market price for uranium fuel (U₃O₈, often called “yellowcake”) available for near term delivery, typically within months. Brent Oil is a global benchmark price for crude oil, based on light, sweet crude produced in the North Sea. It is quoted in U.S. dollars per barrel and is used to price most internationally traded oil. Past performance is no guarantee of future results.

The Broader Critical Materials Complex

Beyond copper and uranium, we believe other components of the critical materials complex also exhibit favorable fundamentals. Lithium and rare earth elements benefit from growth in battery storage, electrification and high-efficiency motors. Silver occupies a unique position, supported both by rising industrial demand and its monetary characteristics in an environment of persistent currency debasement.

This isn’t a typical commodity cycle. Critical minerals are being repriced as national security assets.

Despite these dynamics, many asset allocation discussions around natural resources investments continue to emphasize broad exposures seen in prior cycles. History suggests that this lag in recognition is typical. In the early stages of the 2000s commodity boom, skepticism was widespread, but price moves ultimately far exceeded consensus expectations. We believe a similar pattern is unfolding today, particularly in critical minerals where supply constraints meet policy-driven demand, while global inventory systems fragment.

Importantly, price sensitivity is lower than many assume. The construction of power grids, data centers or electrified infrastructure is considered a national security priority; high copper prices will likely not deter it. Instead, the cost is absorbed, often through additional fiscal spending and monetary expansion, reinforcing the debasement tailwind for real assets. In short, governments are likely to literally print the money to facilitate the buildout of these strategic assets. We do not see the same urgent outcome for chemicals, forest products, packaging, agriculture, etc.

Positioning for a Structural Cycle

These shifts are structural rather than cyclical. They reflect multi-year policy commitments, long project lead times, and a decade of underinvestment across key supply chains. In this environment, broad “own everything” exposure to resources may produce sub-optimal returns. We believe targeted ownership, focusing on the commodities and companies aligned with electrification and energy security, could offer a more compelling risk-reward profile.

Sprott has specialized in natural resource investing for decades, with dedicated teams across metals and mining in public and private markets. To express the themes outlined above, the firm has developed targeted strategies such as the Sprott Critical Materials ETF (SETM) and the Sprott Active Metals & Miners ETF (METL).

Sprott Critical Materials ETF (SETM)

To express this structural shift, the Sprott Critical Materials ETF (SETM) offers targeted, rules-based equity exposure to the companies most directly tied to electrification, power generation and energy security. The strategy is built around critical materials that sit at the center of today’s investment cycle, including copper, uranium, lithium, rare earth elements and silver, which are essential to building energy generation, transmission and storage systems at scale. In an environment increasingly defined by deglobalization, supply chain sovereignty, and fiscal dominance, critical materials are being repriced not only by traditional supply and demand, but also by strategic value and resilience requirements. SETM is designed to reflect that leadership profile through concentrated exposure to the critical materials complex that is most directly leveraged to these themes.

SETM provides pure-play access to a range of critical materials necessary to meet the rising global demand for energy.

Further, SETM has been uniquely designed to create “pure-play”5 exposure within critical materials equities. Drawing on Sprott’s long history in metals and mining investing, Sprott quantifies each company’s exposure to critical materials and works with Nasdaq to ensure that at least 50% of revenue and/or assets is from critical materials. We believe this is a core differentiator for SETM by concentrating the portfolio on constituents that are most directly leveraged to the targeted commodities, rather than on diluted or incidental exposure.

SETM’s pure-play exposure is also systematically maintained over time, rather than being set once at launch and left untouched. SETM’s benchmark6 is rebalanced on a semi-annual basis, which is an important feature because the critical materials and mining universe is dynamic, with frequent new discoveries, mergers and acquisitions, shifts in corporate strategy and changing business mixes, especially among smaller companies. By refreshing the universe and reapplying the exposure framework at each rebalance, the portfolio is designed to remain aligned with the objective of delivering consistent pure-play exposure to the critical materials.

Sprott Active Metals & Miners ETF (METL)

Another way to potentially capitalize on this emerging commodity supercycle is the Sprott Active Metals & Miners ETF (METL). It is the only actively managed metals ETF product, and it is built on Sprott’s decades long specialization and leadership in the natural resources sector. The strategy leverages deep, bottom-up industry expertise across geology, mine economics, jurisdictional risk and portfolio management to construct a well-balanced blend of key metals and mining equities with what we view as the strongest risk-reward profiles. Rather than tracking an index, METL is designed to reflect informed judgment about where value is emerging within the global, critical metals complex. METL is laser-focused on the themes outlined in this article.

METL is actively managed by a global leader with more than four decades of specialized leadership in metals and mining investments.

METL’s active approach allows the portfolio to focus on companies with quality assets, improving fundamentals and leverage to structurally important metals (discussed above), while seeking to avoid riskier capital-intensive projects, marginal cost producers and dilutive business models. METL’s active strategy is unconstrained by fixed rules on market-cap weighting, benchmark composition or predefined commodity buckets, giving its portfolio managers the flexibility to allocate across commodities as supply-and-demand fundamentals evolve and strategic products emerge and mature.7 Security selection is driven by disciplined research, continuous management engagement and an emphasis on asymmetric risk-reward return profiles. At the same time, METL’s portfolio managers are balancing commodity and country exposure, market depth and portfolio liquidity.

Critically, METL has the capability to anticipate and respond to changing geopolitical and supply-demand scenarios in real time, including shifts in commodity prices, policy signals, capital markets conditions and relative value within the sector, all while maintaining the tax efficiency, liquidity, and low-cost structure of an ETF. METL offers investors a flexible, efficient vehicle to potentially capture emerging opportunities and mitigate risk, without being constrained by static rules.

A Multi-Year Investment Cycle Is Taking Shape

For us, the investments required to meet future demand for power generation, grids, data centers and critical materials supply chains are inherently multi-year endeavors. Supply growth remains constrained by long development timelines and a lack of new discoveries, while policy support and strategic urgency continue to build.

We see considerable room for continued outperformance from select commodities and the associated equities. Volatility is inevitable, but in our view, this is the type of environment where specialist expertise, disciplined security selection, risk mitigation and responsiveness to changing conditions could add meaningful value as this new commodity supercycle unfolds.

Footnotes

| 1 | A commodity supercycle is a prolonged period of broadly rising commodity prices driven by sustained, structural demand growth that outpaces supply, typically linked to major economic, industrial, or geopolitical shifts rather than short term market fluctuations. |

| 2 | A bull market is one where prices are rising. |

| 3 | From April 8, 2025, to Feb 18, 2026, the total return of Sprott Critical Materials ETF = 203.80%. From April 8, 2025, to Feb 18, 2026, the total return of S&P Global Natural Resources Index = 62.23%; MSCI ACWI Select Natural Resources Index = 70.43%; Morningstar Global Upstream Natural Resources Index = 59.80% |

| 4 | As of 2/27/2026. Sprott Copper Miners ETF (COPP) is allocated to Freeport (25.66%), Teck (9.22%), Antofagasta (9.44%) and Hudbay (5.32%). Holdings subject to change. |

| 5 | The term “pure-play” relates directly to the exposure that SETM has to the total universe of investable, publicly listed securities in the investment strategy, based on Morningstar's universe of Natural Resources Sector Equity ETFs as of 2/28/2026. |

| 6 | METL’s active-management strategy relies on the fund-adviser’s judgments about the growth, value, or potential appreciation of an investment, which may prove to be incorrect or fail to have the intended results, and could adversely impact METL’s performance. |

| 7 | Nasdaq Sprott Critical Materials™ Index is designed to track the performance of a selection of global securities in the critical materials industry. |

Important Disclosures & Definitions

Specific companies discussed have been included based on objective, non-performance-based selection criteria. There is no guarantee the companies were or will be profitable and may not be representative of any actual investments.

An investor should consider the investment objectives, risks, charges, and expenses of each fund carefully before investing. To obtain a fund’s Prospectus, which contains this and other information, contact your financial professional, call 1.888.622.1813 or visit SprottETFs.com. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the funds, typically in blocks of 10,000 shares.

The Sprott Active Metals & Miners ETF, Sprott Active Gold & Silver Miners ETF and the Sprott Silver Miners & Physical Silver ETF are new and have limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott ETFs. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.