Insights

Sprott Insights offers unique analyses and perspectives from the firm’s leading experts on key topics in precious metals and critical materials.

Interview

Why Uranium Could Be the Next Energy Shock Opportunity

John Ciampaglia, CEO of Sprott Asset Management, breaks down why tightening uranium supply, surging global demand from countries like India and China, and renewed nuclear policy support could set the stage for a major move in uranium prices. Ciampaglia joins Jimmy Connor of Bloor Street Capital for a lively discussion on the positive prospects for uranium markets and nuclear power.

Special Report

Why Gold Has Fallen: A Liquidity Story, Not a Broken Thesis

Gold’s sharp March sell-off isn’t a failure of its safe-haven role. It’s the result of a global liquidity crunch that forced investors to sell what they could, not what they believed in. As reserve flows stall and deleveraging runs its course, the same pressures dragging gold down today may be quietly setting the stage for its next rally.

Video

Copper's Investment Case Rewired

It's time to think differently about "Dr. Copper." Steve Schoffstall joins Asset TV's ETF Editor-in-Chief Kristen Myers to discuss how copper's role is shifting from a construction material to a critical enabler of AI, electrification, and the modern economy. See how supply constraints, policy pressures and geopolitics could shape what comes next.

Sprott Precious Metals Report

Gold Rises Above $5,000 in an Evolving Monetary Regime

Gold and silver reached record highs in February amid volatility as markets adjust to a new monetary regime defined by persistent central bank liquidity and rising geopolitical fragmentation. Structural constraints on the Federal Reserve, growing sovereign debt and continued central bank buying—particularly from China—reinforce gold’s role as a strategic store of value.

Special Report

Lithium Enters a New Era of Strategic Demand and Policy Support

Lithium has surged back into the spotlight, with prices rising more than 125% over the past year as demand broadens beyond electric vehicles and governments begin treating the metal as a strategic resource. With supply disruptions, new policy tools and explosive growth in grid-scale energy storage, lithium is increasingly being repriced not just as a commodity, but as critical infrastructure.

Webcast Replay

Copper’s Surge: Rewriting the Investment Case

In this webcast, Steve Schoffstall, Managing Partner and Head of ETFs at Sprott, discusses copper’s evolution from a traditional construction metal to a critical enabler of AI, data centers, electrification and modern infrastructure. He examines the supply-demand forces driving prices higher and what copper’s growing strategic role may mean for portfolios.

Sprott Copper Report

Beyond “Dr. Copper”: Copper’s Strategic Shift

Copper is breaking free from its old “Dr. Copper” reputation as strategic demand from electrification, AI infrastructure and defense drives prices and mining stocks toward record highs. With copper supply tight and demand increasingly mission-critical, the metal is being repriced as essential infrastructure.

Special Report

Why Critical Materials Are Leading the New Commodity Cycle

Critical materials are being repriced as strategic assets in a new commodity supercycle driven by deglobalization, fiscal dominance and energy security, not traditional cyclical demand. As global investment pivots toward electrification and secure supply chains, SETM and METL provide targeted exposure to the companies positioned at the center of this structural shift.

Video

Uranium’s Catch Up Trade: Nuclear Power’s Next Decade of Demand

Uranium is reemerging as a strategic energy asset as AI, data centers and energy security reshape global electricity demand. In this episode of Metals in Motion, Sprott Asset Management CEO John Ciampaglia explains why tight supply, government action, production incentivization and new reactor technology could drive a long-term bull case for nuclear fuel.

Interview

Silver Conference Featuring Maria Smirnova, Sprott CIO

Maria Smirnova, Sprott Chief Investment Officer, joins James Connor of Bloor Street Capital to discuss Sprott's outlook on silver. Smirnova views recent gold and silver volatility as a healthy correction in a bull market, driven by strong fundamentals like supply deficits and rising global demand rather than speculative excess. Smirnova outlines Sprott’s long-term, disciplined approach and stresses patience and conviction.

Special Report

Justin Tolman: The Metamorphosis of a Career, Turning Rocks into Value Investing

For nearly three decades, Justin Tolman has chased discovery across more than 40 countries, applying boots-on-the-ground geology to transform mineral potential into economic value. Discover how a “renaissance geologist” transforms field insight into differentiated investment intelligence in a world where demand for precious metals and critical minerals is only accelerating.

Video

Nasdaq Just for Funds: Sprott’s Steve Schoffstall on SLVR

Steve Schoffstall joins Nasdaq’s Just for Funds to discuss silver in 2026 after its record-setting rise in 2025. The conversation highlights why investors are gravitating to Sprott Silver Miners and Physical Silver ETF (SLVR), which offers a pure-play silver mining strategy combined with physical silver exposure, positioning it as both a diversification tool and a growth-oriented allocation.

Sprott Precious Metals Report

The Changing Global Order Is Repricing Gold

Gold and silver surged to record highs in January before experiencing technically driven sell-offs. Geopolitical fragmentation, capital conflict and eroding confidence in fiat systems is reshaping what investors consider truly safe. In this emerging monetary regime, gold and silver are asserting their roles as neutral, "outside money" with strong long-term drivers.

Sprott Webcast Replay

Top 10 Dominant Drivers of Metals Markets in 2026

As global markets adjust to deglobalization and fiscal dominance, capital is flowing decisively into gold, silver, uranium, copper, rare earths and other critical materials. In this webcast, we break down what’s driving these moves and share our perspective on the most compelling opportunities for the year ahead.

Sprott Uranium Report

Uranium Enters 2026 with Renewed Strength and Strategic Tailwinds

Uranium enters 2026 with renewed momentum as spot prices move back above $100/lb, mining equities reprice materially, and utility demand re-emerges following prolonged under-contracting. Strengthening U.S. policy support and tightening supply conditions reinforce the case for higher incentive pricing and potential upside across physical uranium and mining equities.

Video

Rewiring the Copper Market: AI, Fragmented Pricing, and the Case for a Structural Bull Run

Copper prices have surged to record highs, driven by unprecedented demand from AI data centers, electrification, and grid expansion. In this episode of Metals in Motion, Sprott’s Steve Schoffstall explains why copper’s rally is fundamentally backed, why supply constraints are likely to persist for decades, and how investors can think strategically about copper exposure amid tariffs and market fragmentation.

Sprott Copper Report

Copper’s Momentum: Key Catalysts to Watch in 2026

Copper’s record run is being driven by tightening supply, strategic demand and rising policy risk, setting up a strong outlook for 2026. Major disruptions and collapsing treatment charges highlight a market firmly in deficit. With AI growth, defense spending and grid modernization accelerating demand, we believe copper and related equities remain well supported.

Special Report

Top 10 Themes for 2026

What are the 10 most important themes impacting global markets in 2026? We explore issues from deglobalization and fiscal dominance to the surge in gold, silver and critical materials, and provide our view of where opportunities and risks may be emerging.

Video

Advisor Perspective: How Gold, Silver and Critical Materials Shaped Portfolios in 2025

In this episode of Metals in Motion, Sprott’s Steve Schoffstall and Ed Coyne recap key 2025 performance trends across gold, silver, critical materials and the mining sector. Coyne shares insights from conversations with financial advisors, highlighting the potential advantages of active management and approaches for gaining broader exposure to critical materials.

Interview

ETF Product Development

Steve Schoffstall and Jimmy Connor of Bloor Street Capital discuss Sprott’s hands-on mining expertise and expanding lineup of precious metals and critical materials ETFs. Schoffstall highlights rising investor interest in uranium, lithium, rare earths and other strategic materials as governments move to reshore supply chains and support long-term energy and infrastructure demand.

Interview

Uranium Outlook 2026

John Ciampaglia joins Jimmy Connor of Bloor Street Capital to discuss uranium’s outlook as government support for nuclear energy strengthens. Tightening supply, rising reactor demand and growing institutional involvement are fueling bullish expectations for uranium and related mining equities in 2026.

Sprott Radio Podcast

Uranium Outlook 2026

Host Ed Coyne and Sprott CEO John Ciampaglia recap a surprising 2025 for the uranium market, characterized by flat spot prices that contrasted sharply with strong mining equities and bullish long-term demand signals for nuclear power. Together, Ed and John look ahead to 2026, highlighting the potential for renewed contracting, higher prices and pivotal U.S. policy decisions that are likely to boost demand for uranium and nuclear power.

Insights

Sprott ETFs 2025 Year-End Distributions

This is not intended to be a statement for official tax reporting purposes or any form of tax advice. If you have any questions, please call 888.622.1813 between 9:00 AM and 5:30 PM ET, Monday through Friday.

Interview

Metals & Mining: Year in Review, Future in Focus

Host Ed Coyne speaks to Sprott CEO Whitney George and Senior Portfolio Manager Justin Tolman about the firm's strong performance in 2025, highlighting significant gains across gold, silver, copper and related strategies, driven by resource nationalization and supply disruptions. Looking ahead to 2026, they anticipate continued opportunities, increased investor interest and ongoing M&A activity as the mining and metals space gains broader recognition.

Sprott Uranium Report

Uranium’s Tale of Two Markets

The uranium market's short-term volatility has masked strengthening fundamentals, as long-term prices rise, supply tightens and policy commitments translate into greater demand for nuclear power. With capital flowing into miners, upstream fundamentals improving and policy alignment accelerating, we believe the uranium market is well positioned for a stronger setup in 2026.

Interview

Nasdaq Talk Your Ticker: SETM

Steve Schoffstall joins Nasdaq’s Talk Your Ticker to discuss the Sprott Critical Materials ETF (SETM), highlighting its pure-play exposure to miners of nine essential metals and its role in diversifying portfolios amid rising energy demand and security concerns.

Sprott Precious Metals Report

Gold Holds Gains as Liquidity Stress Emerges

Gold reached its highest monthly close in November 2025, driven by fiscal dominance, rising global debt and the Fed’s pivot to “QE-lite.” We believe gold’s strategic role as a safe haven asset is strengthening amid mounting liquidity stress and shifting global financial dynamics. Silver closed November at an all-time high.

Special Report

Lithium Gains Momentum in 2025

Lithium has entered a renewed bull phase as tightening supply, rising global demand from EVs to data centers, and major strategic investments shift the market from surplus toward potential deficit. Governments, oil majors and tech giants are racing to secure supply, solidifying lithium's essential role in long-term energy security.

Video

National Security, Mining Investment and the Future of Materials: A Critical Crossroads

In this episode of Metals in Motion, Steven Schoffstall, Director, ETF Product Management at Sprott Asset Management, explains how government action and massive private-sector investment are reshaping the critical materials landscape, including rare earth metals. New U.S. equity stakes, global agreements and major nuclear initiatives are accelerating efforts to rebuild secure domestic supply chains amid rising geopolitical tensions.

Video

Sprott on Metals: Today's Opportunities in Gold, Silver, Uranium and Copper

Jacob White meets with Asset TV to discuss Sprott’s focus on precious metals and critical materials, underscoring their rising importance across energy, technology and national security. White notes that 2025 has seen record highs for gold, silver and copper prices, alongside sustained supply deficits that are driving strong investor interest.

Infographic

The Uranium Opportunity

Global uranium mine supply continues to fall short of reactor demand, creating a persistent and widening deficit. With uranium demand expected to double by 2040, these tightening fundamentals underpin a powerful long-term investment case.

Video

Nasdaq Just for Funds: Sprott’s Steve Schoffstall on METL

Sprott’s Steve Schoffstall joins Nasdaq’s Just For Funds to discuss the Sprott Active Metals & Miners ETF (METL) — the only actively managed ETF providing diversified exposure to both critical and traditional metals miners driving the global energy transition.

Sprott Precious Metals Report

The Debasement Trade Broadens Across Precious Metals

In October, gold closed above $4,000 and silver hit record highs amid growing strategic demand, signaling a sustained shift away from fiat-based assets. Major developed economies are increasingly operating under fiscal dominance, driving investors toward hard assets like gold and silver.

Video

Rare Earths and Critical Minerals: The Hidden Engine of Electrification

Sprott’s Steve Schoffstall joins James Connor to discuss the global race for critical materials, from rare earths and uranium to lithium and copper. Schoffstall discusses how investors can gain exposure through Sprott’s suite of innovative ETFs.

Video

Gold Mining Equities: There's Still Room in the Trade

Gold has recently climbed to record highs. In this episode of Metals in Motion, Steve Schoffstall, Director of ETF Product Management at Sprott, joins Thalia Hayden @etfguide to explain why gold is performing well, and why the gold mining trade might still have room for investors to make their move.

Sprott Webcast Replay

Going Beneath the Surface: Active Management in Metals & Mining ETFs

Join Sprott’s expert team for an exclusive webcast replay exploring the powerful forces reshaping the metals and mining landscape, from surging energy demand and AI growth to tightening supply chains. Discover how Sprott’s active, research-driven ETF approach helps investors navigate volatility, and learn more about GBUG and METL.

Sprott Copper Report

Catalyzing Copper: Supply Shocks and Betting Billions

Copper markets rallied in September, buoyed by tightening supply and renewed investor confidence. Copper’s supply squeeze is intensifying as mine shutdowns and years of underinvestment drive inventories to historic lows. New U.S. policy tailwinds are providing support, as the world races to secure critical materials.

Sprott Gold Report

Dips: The Rx for Acrophobia

With gold and silver reaching new all-time highs, we believe there is still opportunity in both the physical and miners markets. We see structural drivers (central bank demand, inflation resilience and declining trust in fiat currencies) that continue to support long-term allocations to gold and silver.

Sprott Precious Metals Report

Gold Leads as Faith in Fiat Falters

Gold surged to record highs as fading confidence in fiscal and monetary policy drove investors toward hard assets. With long-term yields rising and central banks turning increasingly accommodative, markets are signaling a loss of faith in fiat currencies, fueling gold’s breakout and silver’s potential squeeze.

Sprott Uranium Report

Investors Act with Conviction

Uranium prices and miners surged in September, fueled by tight supply and strong utility demand. The rally drew renewed investor interest, with capital flows into uranium equities and ETFs reinforcing confidence in the sector’s momentum.

Sprott Radio Podcast

The Metals that Make the World

Sprott economic geologist and Senior Portfolio Manager Justin Tolman joins Ed Coyne for a deep dive on demand trends for steel, copper and silver and what it might take to successfully invest in the metals that build the world.

Interview

Where Is Spot Uranium Going?

John Ciampaglia, CEO of Sprott Asset Management, joins Jimmy Connor of Bloor Street Capital at the World Nuclear Symposium 2025. Ciampaglia highlights strong global investor interest in uranium, with both specialist and generalist funds viewing nuclear as a long-term growth story. He notes stabilizing uranium prices, lingering supply challenges and growing demand from utilities, AI and data centers.

Interview

Uranium: At the Fulcrum of AI, National Security and Global Energy Demand

John Ciampaglia, CEO of Sprott Asset Management, highlights takeaways from the September 2025 World Nuclear Symposium: surging uranium demand from electricity, AI and energy security, tech ties like Microsoft and constrained supply supporting higher prices and new mining.

Special Report

Steel Meets Rising Global Electricity Demand

Steel is emerging as a strategic material in meeting global electricity demands, underpinning everything from power generation and transmission to electric vehicles and grid modernization. Demand for green steel is accelerating with market forecasts projecting rapid growth relative to traditional steel.

Video

Active Edge: Why Experience Matters in Metals and Mining Investing

Sprott's Steve Schoffstall and Justin Tolman discuss the newly launched Sprott Active Metals & Miners ETF (METL), which provides active exposure to a broad range of metals. Tolman highlights the team’s rigorous investment process combining top-down sector analysis and bottom-up stock selection, and the importance of site visits in evaluating projects.

Sprott Copper Report

Copper Fundamentals Prevail After Tariff Turmoil

Copper rallied in August, with junior copper miners taking top performance honors. Policy momentum is accelerating as copper gains critical minerals status and attracts major investment. Copper miners are enjoying strong margins as copper demand rises to support electrification, AI and defense.

Sprott Precious Metals Report

Challenges to Fed Autonomy Strengthen Case for Gold

Gold has topped another all-time high above $3,600 per ounce, while silver has reached $41, its highest level since 2011. Both metals may be among the strongest-performing asset classes for the year. We explore how erosion of Fed independence heightens policy risk, reinforcing the strategic role of gold and silver.

Sprott Critical Materials Report

Critical Materials Breakout into a New Bullish Phase

The convergence of national security imperatives, energy transition policies and evolving trade dynamics is fundamentally redefining the role of critical minerals. The breakout in the Nasdaq Sprott Critical Materials Index™ is an early signal of this shift, reflecting technical strength and deep structural drivers.

Video

Copper Clash: Tariffs, Trade Shifts and Opportunity

U.S. copper tariffs are reshaping global markets. In this episode of Metals in Motion, Steven Schoffstall, Director, ETF Product Management at Sprott Asset Management, discusses how copper prices are realigning as fundamentals point to long-term shortages and surging demand from the energy transition.

Video

The Key Drivers of Demand and Volatility in the Precious Metals Space

Nasdaq Trade Talks features Sprott’s Steven Schoffstall and the World Gold Council’s Joe Cavatoni on the key forces driving gold, silver and critical materials, from central bank demand to industrial growth and their role in portfolio diversification.

Sprott Gold Report

A Cure for Financial Dementia

In our view, market euphoria and collective amnesia have left gold miners overlooked despite record profits, soaring margins and aggressive shareholder returns. Gold mining equities are still stuck at bargain basement valuations, and we unabashedly continue to pound the table for precious metals equities and bullion alike.

Sprott Precious Metals Report

Gold Miners Shine in 2025

Gold and silver are up over 25% in 2025, with mining stocks surging more than 50%, yet still undervalued. We see continued upside amid inflation, geopolitical risks and strong fundamentals.

Sprott Copper Report

The Emerging Copper Premium: Policy Risk Meets Physical Scarcity

Copper is being redefined as a national security asset, not just an industrial metal. U.S. tariffs and geopolitical shifts have fractured global pricing and exposed deep supply vulnerabilities.

Silver Report

Silver Investment Outlook Mid-Year 2025

Silver gained nearly 25% through mid-year, and continues to rise in July, as supply remains tight and demand accelerates. With silver crucial to new technologies, the metal is benefiting from powerful structural tailwinds and renewed interest from investors.

Sprott Uranium Report

Uranium’s Mid-Year Momentum

Uranium spot prices jumped nearly 10% in June and uranium miners surged, supported by renewed inflows and global pro-nuclear policy momentum. With AI data centers adding a long-term demand driver, we believe uranium’s structural bull case remains intact.

Video

Copper’s Potential Power Surge: Energy, AI and Beyond

In this episode of Metals in Motion, Steven Schoffstall, Director, ETF Product Management at Sprott Asset Management, discusses copper’s importance to energy and technology, and the associated structural supply deficit resulting from growing demand.

Sprott Precious Metals Report

Gold and Silver Bull Run Continues

Gold and silver have been strong performers in 2025, with both metals up over 25% YTD as global instability drives demand for safe haven assets. Central banks are shifting away from the U.S. dollar, while silver’s breakout suggests a potential supply squeeze ahead.

Interview

Uranium Outlook Mid-Year 2025

John Ciampaglia, CEO of Sprott Asset Management, joins James Connor at the Bloor Street Capital Virtual Uranium Conference to examine the current state of the uranium market. Ciampaglia highlights the market's V-shaped recovery since April and the improved investor sentiment following the absence of tariffs on uranium.

Sprott Copper Report

Copper’s Bullish Setup Strengthens

Copper is surging toward $10,000 per ton as plunging inventories and unexpected supply disruptions expose the market’s tightness. Easing tariff tensions and rising electrification demand are driving bullish sentiment. We believe copper may be heading toward a structural repricing.

Video

COPP Invests in Both Miners and Physical Copper

Beginning June 23, 2025, Sprott Copper Miners ETF (COPP) will provide investors with exposure to physical copper, in addition to pure-play copper miners.

Special Report

Building an Electrified World: The Strategic Role of Critical Materials

As the world races to electrify, demand for critical materials like uranium, copper, silver, lithium and nickel is climbing. These metals are foundational to nuclear power, consumer electronics and high-performance batteries — making them indispensable to meeting rising global energy demand.

Sprott Uranium Report

Uranium’s Bull Market Reawakens

Uranium is back in focus as U.S. nuclear policy accelerates and AI-driven energy demand sparks renewed investor interest. With uranium prices and miners showing strength in May, our outlook remains bullish as fundamentals tighten and sentiment shifts.

Sprott Precious Metals Report

Gold Gains Ground as Faith in the Dollar Erodes

Gold continues its rally as fading confidence in U.S. fiscal policy and the U.S. dollar drives demand for real assets. As we publish, silver is breaking out above $35, supported by structural supply deficits, renewed investor interest and mounting macroeconomic pressures.

Shifting Energy

The White House’s Nuclear Push: What It Means for Uranium Opportunities

In this episode of Shifting Energy (Season 2), John Ciampaglia discusses the major policy shift under President Trump’s new executive orders, which aim to fast-track advanced nuclear technologies and revitalize the entire U.S. nuclear fuel cycle.

Video

Trump’s Executive Orders Set Stage for U.S. Nuclear Expansion

Uranium is back in the spotlight. Steve Schoffstall discusses President Trump's sweeping executive orders to jumpstart America’s nuclear energy industry by streamlining reactor approvals, boosting domestic uranium production and declaring a national emergency over reliance on Russian and Chinese nuclear fuel. With global support for nuclear power building, investors are watching this space closely.

Webcast Replay

Could Silver and Its Miners Shine in Today’s Markets?

In our webcast with Nasdaq, Steve Schoffstall, Director of ETF Product Management, joins Nasdaq’s Jillian DelSignore to discuss silver and silver equity markets, silver’s historic performance during periods of market turmoil, and why the metal and its miners may be a valuable addition to portfolios.

Sprott Uranium Report

Uranium Regains Momentum

Uranium is regaining strength, with spot prices rebounding and momentum returning thanks to renewed utility contracting, tariff clarity and strong long-term fundamentals. The resurgence of the carry trade, rising AI-driven energy demand and China’s ongoing nuclear buildout are reinforcing uranium’s role as a strategic, supply-constrained asset.

Sprott Precious Metals Commentary

A Shaky U.S. Dollar Boosts Gold’s Role as an Alternative Reserve Asset

Gold is gaining prominence as a reserve asset due to a weak U.S. dollar and declining U.S. financials, reaching record highs while equities and bonds fell. We believe this positions gold as a potential anchor for a multi-asset reserve system. Given silver’s correlation to gold, we believe its monetary value will reassert itself in time.

Interview

Sprott CIO on Gold/Silver Miner Selection and Silver Outlook

James Connor of Bloor Street Capital speaks with Maria Smirnova, Sprott CIO, about the firm’s approach to gold and silver miner selection. Smirnova remains bullish on silver, citing a deep supply deficit and its essential role in electrification, despite prices lagging gold due to weak central bank demand and stagnant supply.

Video

Nasdaq’s Just for Funds: Introducing the Sprott Active Gold & Silver Miners ETF (GBUG)

Steve Schoffstall recently joined Nasdaq’s Just for Funds to discuss the launch of the Sprott Active Gold & Silver Miners ETF (GBUG), the only actively managed ETF focusing on gold and silver mining companies. Given current market volatility, gold is proving its value as a portfolio stabilizer, while investors may benefit from diversification and the flexibility of an active strategy to navigate the complexities of the mining sector.

Video

Why Does a Pure-Play Strategy Matter in Silver Miners?

SLVR is a silver mining and physical silver ETF that offers a pure-play strategy that allocates approximately 70% to silver-focused companies. SLVR offers investors a targeted and differentiated way to gain meaningful exposure to silver.

Shifting Energy

Safe Havens: The Enduring Stability of Precious Metals in Turbulent Times

In this episode of Shifting Energy (Season 2), Steve Schoffstall, Director, ETF Product Management and John Kinnane, Director, Key Accounts at Sprott Asset Management, chat about how investors are navigating bumpy markets and global trade wars with assets like gold and silver.

Sprott Uranium Report

Is Uranium’s Bull Market Over?

Recent market events have put pressure on uranium, but we continue to believe in the resilience and long-term bullish outlook for physical uranium and uranium mining equities. Our positive outlook is supported by uranium's growing structural supply deficit and global policy support for nuclear power.

Sprott Gold Report

The Return of Exter’s Inverted Pyramid

Gold has been rising on strong official sector demand, fueled by concerns over the U.S. dollar and global instability. While Western investors have focused on potentially overvalued stocks, gold and mining equities offer potential upside as other assets struggle.

Sprott Copper Report

Copper’s Record-Setting Rally and Reversal on U.S. Tariffs

Copper prices reached record highs in March, driven by tariff fears and U.S. demand. Despite recent market volatility, copper remains a strategic asset with strong long-term fundamentals, supported by rising global energy demands and U.S. policy shifts.

Sprott Q1 Precious Metals Report

Gold's Strength Amid a Crisis of Confidence

Gold's record-breaking rally in Q1 2025 reflects mounting investor anxiety over stagflation, policy volatility and a fraying global economic order. U.S. tariffs and policy unpredictability have elevated the risk of stagflation, fueling demand for gold as the lone liquid safe-haven asset. We also believe silver is potentially poised to break out.

Sprott Webcast Replay

A Closer Look at Gold and Silver, Metals and Miners

Gold and silver provide a powerful blend of potential wealth preservation, inflation mitigation and portfolio diversification. This webcast provides insights from John Hathaway and Maria Smirnova on the key technical drivers influencing gold, silver and precious metals mining equities.

Shifting Energy

Global Trade Wars: Unraveling the Impact on Critical Materials Markets

In this episode of Shifting Energy, Thalia Hayden interviews Steven Schoffstall, Director, ETF Product Management at Sprott Asset Management about how the global energy shift and market volatility are impacting precious metals and critical materials. Schoffstall provides valuable insights into what's happening with gold, silver, uranium and copper.

Video

Introducing Sprott Active Gold & Silver Miners ETF (GBUG)

Sprott’s Steve Schoffstall introduces GBUG, an actively managed ETF focused on gold and silver miners, using a team with deep industry expertise to identify investments. With a long-term, value-driven approach, it aims to provide exposure to precious metals while navigating market shifts.

Interview

Trump Tariffs: Disruption or Opportunity?

Are tariffs set to disrupt gold, silver and uranium markets? Find out how potential trade barriers could impact prices and create arbitrage opportunities. Kitco’s Senior Mining Editor and Anchor Paul Harris interviews John Ciampaglia, CEO of Sprott Asset Management, at the 2025 BMO Global Metals, Mining & Critical Minerals Conference.

Sprott Uranium Report

Tariffs, Tensions and the Uranium Opportunity

We see market volatility as an opportunity, with uranium’s spot price offering an attractive entry point for investors. Despite Trump tariff policy and geopolitical uncertainties, uranium’s strong long-term fundamentals—supply deficits and rising nuclear demand—remain intact.

Educational Video

The Era of Critical Materials: Powering Our Planet Toward a Brighter Future

We explore the essential minerals driving the energy revolution, from copper's role in electrification to uranium's impact on nuclear power, and the rise of battery storage technology. Join us on a journey through the periodic table to understand how these critical materials are needed to meet the rising global demand for energy.

Special Report

GBUG and The Case for Active Management

Sprott Asset Management has launched GBUG which seeks long-term appreciation through value-oriented, contrarian investing. Sprott's active management team looks to capitalize on the wide dispersion of returns within the mining sector and the potential for silver to catch up to gold's rise.

Sprott Critical Materials Monthly

Critical Materials Markets Shake Off DeepSeek Disruption and U.S. Policy Rollbacks

Critical materials showed resilience in January amid global volatility. We take a deep dive into China's growing leadership in clean technology investments, the disruptive impact of DeepSeek's AI model and the implications of U.S. policy changes on the energy transition and critical materials supply chains.

Video

Introducing Sprott Silver Miners & Physical Silver ETF (Nasdaq: SLVR)

Discover the unique advantages of Sprott Silver Miners & Physical Silver ETF (SLVR), a new ETF offering exposure to both silver miners and physical silver. With rising industrial demand and a tightening supply, SLVR provides investors with a strategic opportunity to benefit from silver’s dual role as a precious and industrial metal.

Sprott Uranium Report

Uranium Markets Trumped by Uncertainty

The uranium markets experienced volatility in January, with prices dipping despite strong miner performance. Key factors included the emergence of the Chinese AI model DeepSeek and the return of the Trump administration.

Shifting Energy

Energy’s Silver Lining: A Precious Metal Powering the Future

In this episode of Shifting Energy (Season 2), Thalia Hayden chats with Steven Schoffstall, Director, ETF Product Management at Sprott Asset Management about silver miners, investing in silver and how the silver market is tied to the global energy shift.

Interview

Uranium Outlook for 2025

Sprott CEO John Ciampaglia remains bullish on the uranium markets, citing rising term prices, increased utility interest and the global nuclear renaissance fueled by clean energy needs and AI-driven power demands. Ciampaglia expects uranium prices to strengthen as pent-up demand grows, driven by reactor life extensions, new builds and geopolitical supply disruptions.

Sprott Radio Podcast

Silver 2025

Pinch point is the term Sprott’s Maria Smirnova uses to describe the current supply-demand picture for silver in 2025. Smirnova joins host Ed Coyne to walk us through how silver’s growing demand is coming up against a static supply pipeline.

Special Report

Top 10 Themes for 2025

What forces will shape the markets in critical materials and precious metals in 2025 and beyond? We identify 10 critical macro and market themes investors should watch in the coming year.

Sprott Gold Report

Recalibrating Our Crystal Ball

Gold was a strong performer in 2024, gaining 27.22% to end the year at $2,624.50, fueled by geopolitical tensions, central bank purchases and bond market struggles. These strong gains occurred with negligible participation or interest from investors in North America or Europe. Key catalysts for a gold rally could include stock or cryptocurrency downturns, bond market disruptions or a U.S. dollar reset.

Shifting Energy

Uranium Unleashed: How Mining Stocks Fuel the Nuclear Comeback

Sprott's John Kinnane and Steve Schoffstall explore the growing opportunities in the uranium and nuclear energy markets. They discuss how pure-play uranium miners, supply-demand dynamics and shifting geopolitical policies are positioning this sector as a promising investment frontier for 2025 and beyond.

Silver Report

Silver's Impressive Strength in 2024

We believe that silver continues to offer a compelling investment opportunity due to its unique market dynamics. For investors, a diversified portfolio that balances physical assets and mining equities may offer exposure to silver's stability as a store of value and its growth potential as a critical industrial metal.

Special Report

The Uranium Miners Opportunity

We believe uranium mining equities are poised for growth as demand for nuclear power increases, driven by AI data center needs and electricity demand. Geopolitical shifts, such as Russia’s export restrictions, and global pledges to triple nuclear capacity by 2050 highlight supply chain importance. This creates a compelling case for uranium miners, which are supported by strong market fundamentals.

Sprott Uranium Report

Uranium Markets Impacted by Market Signals and Uncertainty

The uranium market remains strong despite recent spot price declines, with tight supply, rising demand and long-term fundamentals driving a bullish outlook. Global support for nuclear energy is growing, with ambitious commitments to triple capacity and junior miners playing a key role in addressing supply deficits.

Insights

Sprott ETFs 2024 Year-End Distributions

This is not intended to be a statement for official tax reporting purposes or any form of tax advice. If you have any questions, please call 888.622.1813 between 9:00 AM and 5:30 PM ET, Monday through Friday.

Interview

Nuclear Power and Critical Materials: A Post-Election Outlook

What’s the potential impact of the incoming Trump administration on nuclear power, clean energy and critical materials? Thalia Hayden of ETFguide talks with John Ciampaglia about what potential changes may be on the horizon for U.S. energy policies and some strategies for investment portfolios.

Interview

Real Assets in Focus: Gold, Silver, Copper and Uranium

Unlock the power of real assets investing with Sprott’s Masterclass video. Dive into gold, silver, copper and uranium with industry experts Ed Coyne, Ryan McIntyre and Steve Schoffstall as they reveal strategies to navigate global uncertainties and identify opportunities. Discover how to leverage precious metals and critical materials to potentially build a resilient, future-ready portfolio.

Sprott Critical Materials Monthly

Batteries and Minerals Driving Global Electrification

Batteries and energy storage continue to underpin electrification trends, solidifying their role as a cornerstone in the global shift toward sustainable energy. Support is being strengthened by strategic investments from governments and corporations, and resilient demand for critical minerals like lithium, copper and nickel.

Interview

Why Tech & Big Investors Are Turning to Uranium & Gold

John Ciampaglia, CEO of Sprott, joins James Connor to discuss why gold is increasingly viewed as a safeguard against economic uncertainty and why uranium has become essential to powering big tech's ambitious AI expansion.

Shifting Energy

The New Power Play: How Tech Giants Are Embracing Nuclear Energy for Data Centers

Nuclear power is creating a buzz in media circles. Thalia Hayden of @etfguide talks with John Ciampaglia about the powerful comeback of nuclear energy and how tech giants are embracing nuclear energy for data centers.

Sprott Uranium Report

Big Tech Targets Nuclear Energy to Support AI Ambitions

Big tech is turning to nuclear energy to fuel the massive power needs of AI-driven data centers. They're striking bold deals to develop small modular reactors (SMRs), sparking a surge in uranium demand and helping to support clean energy innovation. At the same time, global uranium supply remains inadequate to meet both current and future reactor requirements.

Sprott Q3 Precious Metals Report

Gold and Silver Enjoy Continued Rally

Gold and silver prices surged in Q3 2024, driven by central bank buying and macroeconomic factors. While gold experienced a historic price increase, silver's price was influenced by both its precious metal value and industrial demand. YTD through September 30, gold is up 27.71% and silver has gained 30.95%.

Sprott Critical Materials Monthly

U.S. Electricity Grid Remakes Itself to Meet Surging AI-Led Power Demand

Demand for electricity over the next decade will put pressure on the U.S. power grid to keep pace. New investment in power-hungry industrial facilities is driving demand, especially the data centers that support artificial intelligence (AI), U.S. reshoring initiatives and the steady electrification of the transport sector.

Sprott Webcast Replay

Investing in Critical Materials: A Diversified Approach to a Long-Term Opportunity

In our webcast with Nasdaq, John Ciampaglia discusses the rapid emergence of technologies like AI, the race to upgrade power grids, continuing global decarbonization goals and growing middle classes. He gives an overview of how the critical materials behind energy—such as uranium, copper, nickel, lithium and more—are likely to remain growth-oriented investment opportunities for the long term, and how to invest in them in a single allocation.

Sprott Uranium Report

Uranium Markets Shake Off Summer Doldrums

The uranium market has faced short-term volatility, including price declines driven by geopolitical tensions and economic concerns. Despite these challenges, the long-term outlook remains strong. Supply uncertainties from key producers like Kazakhstan and Russia are contributing to this volatility, but the fundamental supply-demand imbalance suggests further growth potential.

Shifting Energy

The Fourth Industrial Revolution: Reshaping Global Energy Markets

Sprott's Steve Schoffstall discusses how AI, robotics and quantum computing are integrating into the overall global economy and how these developments will reshape the global energy landscape. Learn about electricity production and technological innovation and how to invest in the opportunities they provide.

Shifting Energy

An Inside Look at the Global War for Lithium, Copper and Critical Minerals with Author Ernest Scheyder

Author and acclaimed Reuters journalist Ernest Scheyder discusses his book, The War Below: Lithium, Copper, and the Global Battle to Power Our Lives, with Sprott's Steve Schoffstall in this exclusive interview.

Sprott Critical Materials Monthly

The Unstoppable Rise of Renewable Energy

Renewable energy is rapidly replacing fossil fuels as costs decrease and efficiencies improve with increased deployment, making it much cheaper than traditional energy sources. This shift, driven by the exponential growth of renewables, electrification, and efficiency, is expected to significantly alter global power dynamics as fossil fuels are phased out.

Special Report

The AI Revolution and Data Centers: A New Frontier in Energy Demand

Significant investments in AI-related tech stocks have helped push the S&P 500 Index to record highs this year. The rapid growth of AI is significantly increasing the energy demands of data centers, which is likely to lead to a surge in demand for critical materials.

Special Report

Lithium: Short-Term Opportunities for a Long-Term Trend

This might be an ideal moment to re-evaluate lithium miners given their potential to benefit as the global energy transition continues. The current dip in the price of lithium miners presents a potential short-term opportunity, given the strong future demand and supply imbalance.

Sprott Uranium Report

Uranium Case Strengthens

The uranium spot price has remained range-bound between $85 and $95 per pound, and ended the first half at $85.34 (June 30, 2024). Uranium miners fell in June, but bounced back in early July, outperforming the commodity YTD. Over the longer term, physical uranium and uranium miners have demonstrated significant outperformance against broad asset classes, particularly other commodities.

Sprott Q2 Precious Metals Report

Gold’s Record-Setting Quarter and Silver’s Resurgence

Gold has been on the move since Q2 ended, after having gained 12.79% year-to-date as of June 30, gold's best six-month start since 2020. Gold enjoyed strong support from central bank buying. Silver closed Q2 at $29.14, its highest quarterly close since Q3 2012. Silver was supported by the gold breakout and global monetary expansion policies.

Sprott Critical Materials Monthly

Fourth Industrial Revolution Fuels Global Competition for Critical Minerals

The world is in the midst of a fourth industrial revolution (4IR) as technological developments like artificial intelligence (AI), robotics, IoT, genetic engineering and quantum computing bring about an unprecedented integration of the digital, physical and biological realms. Electrification and energy are pivotal to advancing 4IR technologies, and the resulting demand pressures on critical minerals like copper, lithium and uranium are supporting a new commodity supercycle.

Shifting Energy

Copper and AI: Understanding the Opportunity for ETF Investors

In this episode of Shifting Energy (Season 1), Thalia Hayden of @etfguide talks with John Ciampaglia, CEO of Sprott Asset Management, about the growing energy requirements of AI and how uranium, copper, silver and other metals may benefit.

Shifting Energy

Uncovering Big Opportunities and Demand in Nickel for Investors

In this episode of Shifting Energy (Season 1), Thalia Hayden of etfguide talks with Steve Schoffstall, Director of ETF Product Management at Sprott Asset Management, about the nickel growth story, what's driving it and the investment opportunities now and ahead.

Interview

Gold Outlook with John Hathaway

What will take the gold price higher? John Hathaway, Senior Portfolio Manager, provides his thoughts on why gold isn't moving and what will take it higher.

Sprott Uranium Report

Uranium Miners Lead Market Higher

Thus far in 2024, the uranium spot price has stabilized between $85 to $95 per pound after a significant 88.54% increase in 2023. This phase indicates a healthy correction within a bullish market cycle. Uranium miners have shown improved performance, catching up to gains in the spot price.

Sprott Critical Materials Monthly

A New Copper Supercycle Is Emerging

The copper market is entering a new supercycle, built on several rising geopolitical and market trends contributing to a strong bullish outlook. Demand is surging as countries invest in clean energy and protect their access to copper, while supply is constrained by a lack of new mine development.

Sprott Silver Report

Silver’s Critical Role in the Clean Energy Transition

Silver is a critical player in the global shift toward cleaner energy. Solar panels and EVs, both essential for curbing greenhouse gas emissions, rely heavily on silver. Other new technologies, including AI, have also sparked demand for silver, while overall silver supply has declined.

Sprott Webcast Replay

Gold and Silver: Precious Metals On the Move

Replay our webcast, focused on gold and silver, and featuring John Hathaway and Maria Smirnova. Gold is enjoying strong support from central bank buyers like China, and silver is benefitting from increased demand for PV solar panels.

Sprott Critical Materials Monthly

AI's Critical Impact on Electricity and Energy Demand

The rise of AI and data centers is likely to significantly increase global electricity demand, creating challenges for power grids but also opportunities for stable, clean energy sources like nuclear power. AI data centers are also likely to support increased demand for copper.

Special Report

The Case for Investing in Nickel Miners

Nickel's future looks promising due to its role in achieving net-zero emission goals. Stricter regulations and government support for electric vehicles are driving up demand for nickel, which will benefit nickel mining companies in the long run. Nickel-intensive batteries are also increasingly being used in large-scale energy storage systems that employ thousands of NMC batteries to power renewable energy projects.

Special Report

Nuclear Revival: A Resurgence for Uranium Miners

Rising global commitments to nuclear energy are helping to make uranium a compelling investment. While spot uranium prices have come down slightly after a significant rise, we believe there is room for growth given that demand is expected to climb as the need for low-carbon energy sources intensifies. We believe that uranium miners can add growth potential and diversification to investor portfolios.

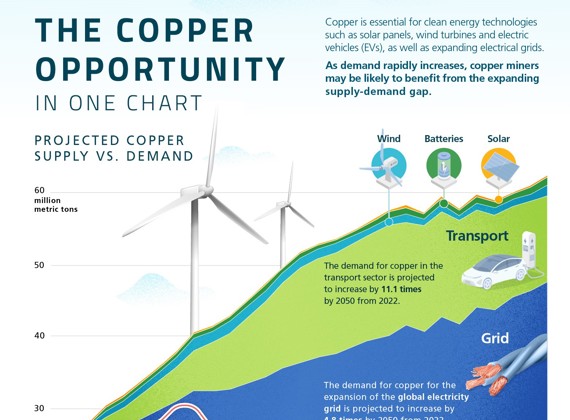

Infographic

The Copper Opportunity in One Chart

As the world embraces clean technologies, the search for and expansion of copper mines will be essential. Early investors who gain exposure to copper mines may benefit from the rapidly increasing demand.

Sprott Uranium Report

Miners Ignore Softer Uranium Price

The uranium market showed mixed performance in March: the spot uranium price fell but miners' stocks rose due to long-term positive outlook for uranium demand. With no meaningful new supply on the horizon for three to five years, we believe the uranium bull market has further room to run.

Sprott Critical Materials Monthly

Battery Storage Is the Technological Cornerstone for a Sustainable Energy Future

The energy sector has experienced a remarkable transformation, primarily driven by the rapid growth and integration of renewable energy sources. Central to this transition is the advancement of battery storage technology, a critical enabler that promises to reshape how we generate, distribute and consume electricity. As we examine this evolving landscape, it becomes evident that battery storage is a technological cornerstone for a sustainable energy future.

Sprott Q1 Precious Metals Report

Gold Is on the Rise and Reaches All-Time High

Gold reached an all-time closing high and is up 8.09% YTD (as of 3/31/2024) after rising 13.10% in 2023. We believe several fundamental factors are in place for gold to move higher, in particular, strong central bank buying. We also see three drivers for a higher silver price: 1) silver tracks rising gold due to central bank buying, 2) reflation trade and 3) increased solar panel demand.

Shifting Energy

The Copper Growth Story

In this episode of Shifting Energy (Season 1), Thalia Hayden @etfguide talks with Ed Coyne, Senior Managing Partner and Steve Schoffstall, Director of ETF Product Management at Sprott Asset Management about the copper growth story, what's driving it and the investment opportunities now and ahead.

Interview

The Elements of Energy: Uranium and Copper

Learn how renewed interest in nuclear power, rising global energy demands, and the transition to clean energy are driving investment opportunities in uranium, copper and their miners.

Sprott Webcast Replay

Uranium and Copper: The Elements of Energy

Electricity demand is expected to grow 86% by 2050. At the same time, most of the world is committed to seeking zero-carbon emissions and increasing nuclear energy capacity. At the center of this growth and transformation are uranium and copper – two critical materials that are in high demand and limited supply. These materials and their miners are potentially attractive investment opportunities.

Sprott Radio Podcast

Nickel: The Hidden Metal

Used in far more than just coins today, nickel is the hidden metal that’s everywhere in our modern world. To walk us through its fascinating story, Ed Coyne is joined by Gary Coates from The Nickel Institute.

Sprott Uranium Report

Uranium Bull Market Takes a Healthy Pause

Uranium markets pulled back in February after a rapid rise—in our view, this is a healthy pause in the ongoing uranium bull market. Announcements from Kazatomprom and Cameco underscored the uranium markets' structural supply deficit, while global governments continued to champion the benefits of nuclear energy.

Interview

Nasdaq TradeTalks: How the Demand for Copper Could be Impacted by the Transition to Cleaner Energy

Steve Schoffstall visits Nasdaq TradeTalks to talk about Sprott’s continued expansion in the critical minerals sector, including the launch of Sprott Copper Miners ETF (COPP). Steve touches on the demand for copper in the ongoing global energy transition and what it means for the copper market overall.

Interview

Nasdaq Investment News: Copper and its Role in the Transition to Cleaner Energy

Ed Coyne stops by Nasdaq Investment News to discuss copper’s role in the energy transition, its current status in the market and how Sprott is capturing the potential opportunity with the Sprott Copper Miners ETF (COPP) and the Sprott Junior Copper Miners ETF (COPJ).

Sprott Critical Materials Monthly

Global Investment Pours into Renewable Energy

February was a lackluster month for critical materials, but the backdrop remains very positive. The global commitment to clean energy hit a new milestone in 2023 as investment in energy transition surged to an unprecedented $1.77 trillion, led by electrified transport. Over the past 10 years, investment in global energy transition has grown at a 24% compound annual rate, several times the global GDP growth rate.

White Paper

A New Era: How Critical Minerals Are Driving the Global Energy Transition

Critical minerals are essential for the global energy transition as we gradually phase out CO2-intensive energy sources with cleaner sources, including nuclear, solar, wind, hydro and geothermal energy and greater use of electric vehicles (EVs). We believe the unique supply and demand dynamics for critical minerals will underpin potential investment opportunities in the years ahead.

Shifting Energy

The Nuclear Energy Comeback and Uranium Powering It

John Ciampaglia, CEO of Sprott Asset Management, joins Thalia Hayden on Sprott’s new video series, Shifting Energy. They discuss surging uranium prices, the latest nuclear renaissance and potential investment opportunities. The series was created in partnership with ETF Guide to keep viewers on top of energy transition investment opportunities.

Sprott Radio Podcast

All Eyes on Uranium Part 2

Per Jander from WMC is back for Part 2 of our All Eyes on Uranium series. Per and host Ed Coyne discuss the recent production guidance announcements from Kazatomprom and Cameco and the overarching issue of the structural supply deficit in uranium.

Special Report

Copper: Wired for the Future

The demand for copper in energy grids, electric vehicles and clean energy technologies, combined with diminishing ore grades and limited inventories, underscores copper's growing importance. We believe copper prices and miners are likely to benefit from the growing supply-demand gap.

White Paper

Copper: The Red Metal's Central Role in Powering Our Net-Zero Carbon Future

Today, in the United States alone, copper is a crucial element in nearly 7 million miles of electrical transmission and distribution wires. This white paper introduces the trends that are driving copper markets and copper miners, and explains our positive outlook for growth.

Sprott Uranium Report

Uranium Price Returns to Triple Digits

Uranium price surged 11% in January to $101 per pound, fueled in part by Kazatomprom's cut in guidance for 2024 production by ~14%. Junior uranium miners were top performers for the month, climbing 18.78%. Supply uncertainties continue to dominate markets, given the situation in Niger and possible bans on Russian uranium.

Sprott Critical Materials Monthly

The Emerging Renewable Energy Economy

A significant transition is underway in global energy production. The era of renewable energy is emerging and beginning to reshape power generation. Recent trends suggest that this shift is no fleeting phenomenon but a fundamental transformation powered by the relentless fall in renewable energy costs. The world is investing heavily in renewables. Some 62% of total global energy investment is now directed to clean energy.

Infographic

Nine Critical Energy Minerals For Investors

Low carbon energy technologies are driving increasing demand for minerals critical to the energy transition.

Sprott Radio Podcast

All Eyes on Uranium Part 1

Per Jander joins host Ed Coyne for the first of a series of podcasts covering all the latest developments in uranium. Part 2 will be recorded and released after the upcoming announcements from Kazatomprom and Cameco in early February.

Interview

Sprott is Bullish on Uranium as Governments Shift to the Energy Source

John Ciampaglia, CEO of Sprott Asset Management, sits down with Andrew Bell of BNN Bloomberg to discuss the uranium market and Sprott’s growth in the space. Campaglia: "We’ve been very active in educating the market and investors about the uranium thesis since we acquired the Uranium Participation Corporation in July of 2021."

Special Report

Top 10 Themes for 2024

What forces are likely to drive energy transition materials and precious metals markets in 2024 and over the next decade? We discuss 10 critical macroeconomic and market-specific themes ranging from deglobalization and climate policy to the new commodity supercycle and a potential silver price breakout.

Educational Video

Nuclear Waste: Dispelling Fears and Myths

Nuclear waste is not something to be feared. The care with which it is handled and stored contributes to the fact that nuclear power is one of the safest forms of baseload energy generation known to humanity. In this video, we dispel the many fears and concerns about spent nuclear fuel.

Sprott Outlook

What a Year for Uranium and Nuclear Energy

2023 provided the long-awaited inflection point for the uranium contracting cycle whereby we have finally achieved replacement rate levels. We believe the era of uranium inventory destocking and utility complacency is over. Long-term security of supply concerns, fanned by lingering geopolitical risks and the challenges of expanding primary production, are likely the key themes to watch.

Interview

Sprott Energy Transition ETFs

The Sprott Energy Transition ETFs are a suite of ETFs designed with the potential for revenue and asset growth by investing in the miners of critical minerals that enable clean energy generation, transmission and storage: Lithium, Uranium, Copper, Nickel and several others.

Sprott Radio Podcast

The Lowdown on Uranium Demand

Justin Huhn, founder of Uranium Insider, joins host Ed Coyne for a deep analysis of the uranium fuel supply chain and the challenges to satisfy expanding demand. "This year alone, demand is around 200 million pounds and supply is about 160 million pounds. That means we're about 40 million pounds short."

Sprott Uranium Report

Uranium & Nuclear Get Boost from COP28

The U3O8 uranium spot price broke through $80 per pound, gaining 8.39% in November and is up 67.10% YTD; uranium stocks followed suit. COP28 was dubbed the "nuclear COP" in recognition of nuclear power's increasing importance and a growing awareness of a uranium supply-demand gap.

Sprott Critical Materials Monthly

Lithium-Ion Technology Solidifies Lead in EV Battery Stakes

The long-term trajectory for EVs is positive despite the recent slowdown. The EV industry is navigating the typical challenges of early technology adoption, with continuous investments and technological advancements driving the transition to electrification. Lithium-ion batteries (LIBs) are the preferred battery technology for EVs, thanks to their superior technical properties and significant investment in their development and infrastructure.

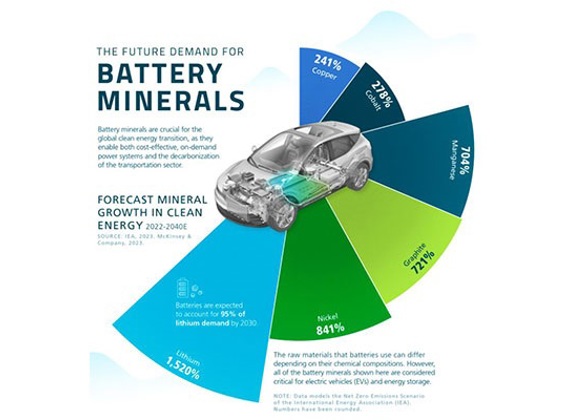

Infographic

The Future Demand for Battery Minerals

Battery metals are expected to account for 95% of lithium demand by 2030. Battery minerals are crucial for the global clean energy transition, as they enable both cost-effective, on-demand power systems and the decarbonization of the transportation sector.

Infographic

The Global Uranium Market in 3 Charts

The uranium market is experiencing increased demand, driven by its integral role in clean energy generation through its use in nuclear power.

Interview

Uranium Market Outlook 2024

Per Jander and James Connor discuss the uranium market, highlighting the catalysts for sharp increases in uranium prices in 2023, including increased utility and producer activity, production shortfalls from major players like Cameco and Orano, and geopolitical uncertainties affecting supply. Per Jander expresses optimism for the uranium market, emphasizing strong demand, ongoing long-term contracting discussions and potential supply disruptions as factors that could contribute to further price increases in 2024.

Sprott Uranium Report

Higher Uranium Prices Allow Miners to Resume Production

The uranium price increased in October, reaching a 12-year high at $74.48 per pound. Although uranium mining stocks pulled back last month, the stronger uranium price has boosted producer revenues and the potential for mine restarts and new developments. A growing supply deficit is helping to support higher price levels as the West focuses on reshoring supply chains.

Sprott Radio Podcast

Battery Materials Deep Dive

Daisy Jennings-Gray from Benchmark Minerals Intelligence joins host Ed Coyne for a deep dive into today’s battery metals markets.

Sprott Critical Materials Monthly

Energy Security and the Shifting Focus from Oil to Critical Minerals

As the United States advances in its pursuit of clean energy, it is strategically redirecting its energy security emphasis from oil to critical minerals. This dynamic shift is designed to decrease reliance on oil, and diminish the influence of oil geopolitics and the sway of petrostates such as Russia.

Interview

Uranium Rally in Early Innings, Sprott Asset Management CEO Suggests

John Ciampaglia, CEO of Sprott Asset Management joins CNBC Fast Money to talk about the uranium market and share Sprott's views on the benefits of nuclear energy and the need for energy security.

Interview

The Energy Transition to Uranium and Battery Metals

Ed Coyne, Senior Managing Partner, sits down with Gillian Kemmerer of Asset TV to discuss the energy transition to uranium and other battery metals, and what investors should take into consideration in this space. He also shares Sprott's outlook on gold.

Sprott Precious Metals Report

Central Banks Support Gold & Solar PV Demand Buoys Silver

Despite a pullback on gold investments, demand from sovereigns and central banks remains unwavering. Over the past decade, China has been committed to bolstering its gold reserves to enhance its economic and geopolitical standings. Silver is likely to be in high demand as the energy transition expands, given it is critical to solar PV panel technology, EV batteries and 5G cellular service.

Sprott Critical Materials Monthly

Silver Demand Grows as Solar Leads Renewables

Uranium's performance helped the energy transition complex close higher in September. From a macro outlook, solar panels are emerging as a critical player in the global energy transition. Evolving technologies in renewable energy, especially in the solar space, are driving a surge in silver demand which may likely outpace supply over the next decade.

Interview

Rethinking Energy Exposure with Mineral and Mining ETFs

The global transition to clean energy is driving demand for critical minerals like uranium, copper and battery metals such as lithium and nickel. These minerals are crucial for nuclear power, electric vehicles, wind, solar, and hydropower.

Sprott Radio Podcast

Take What You Can Get

With demand for nuclear fuel growing and supply facing challenges, the prevailing sentiment at the recent World Nuclear Symposium in London was “take what you can get.” Just back from the event, John Ciampaglia and Per Jander join host Ed Coyne to update us on the full story.

Sprott Uranium Report

Uranium Rally Gains Power in September

Uranium and uranium mining stocks posted their best month in two years, as the price of U3O8 reached a 12-year high. YTD as of 9/30/23, physical uranium has risen 51.88% and uranium mining equities have gained 23.93%. Positive sentiment toward nuclear power is growing, and the WNA estimates that uranium demand will double by 2040. Western nations are strategically maneuvering to reduce their dependence on Russia for both uranium supplies and related services.

Video

How the Uranium Market Works

Per Jander, WMC Technical Advisor to Sprott Physical Uranium Trust, draws upon his years of experience as a uranium trader to reveal how the market works. Who are the buyers and sellers, how is uranium transacted and how will the market evolve moving forward? Per answers these questions and more to give investors a better understanding of the dynamics of the uranium trade.

Special Report

Pro-Nuclear Sentiment Ignites Uranium Opportunities

The global nuclear power industry is experiencing a revival. Geopolitical events and a surge in energy demand have shifted sentiment positively, with countries investing in new nuclear reactor builds, restarts and extensions. This has created a growth opportunity for uranium miners, especially as the uranium supply is facing challenges in meeting current and future demand.

Sprott Webcast Replay

The Great Power Shift: Uranium, Battery Metals and the Energy Transition

The clean energy transition and worldwide energy security goals are fueling a global power shift. This shift has reignited interest in nuclear power, accelerated electric vehicle (EV) adoption and spurred renewable energy deployment. In this environment, uranium, lithium, copper and other high-demand, short-supply critical minerals are vitally crucial — and potentially attractive as investment opportunities.

Sprott Uranium Report

Strong Fundamentals Anchor Uranium's Rise

Uranium and uranium mining stocks had a strong month in August. YTD as of 8/31/2023, spot uranium and uranium mining stocks have climbed 25.49% and 21.52%, respectively, outperforming the frothy S&P 500 TR Index's YTD return of 18.73%. We believe the uranium bull market is intact and favorable supply-demand dynamics will likely continue to provide support.

Sprott Critical Materials Monthly

U.S. Taking Center Stage in Cleantech Investment

Uranium had a strong month in August, contrasting with the decline of most energy transition metals due to China's economic troubles and shadow banking woes. The investment capital spurred by the U.S. Inflation Reduction Act (IRA) is turning the U.S. into a cleantech powerhouse, reshaping global economics. The old China-led commodity supercycle is giving way to a new U.S.-based supercycle focusing on clean energy and innovation.

Special Report

Electric Vehicles and the Growing Opportunity for Lithium Miners

Electric vehicle (EV) adoption has surged in recent years, creating unprecedented demand for lithium, a critical component of EV batteries. With lithium demand expected to rise substantially in the years ahead, lithium miners are at the nexus of the global EV transformation.

Sprott Radio Podcast

The Great American Nuclear Renaissance

With the introduction of the Inflation Reduction Act, US policy makers have reset the landscape for nuclear energy. Ed is joined by Benton Arnett from the Nuclear Energy Institute to walk us through the details.

Sprott Uranium Report

Stars are Aligning for Uranium and Nuclear Energy

Uranium continued to outshine other commodities, with U3O8 surging 16.35% and uranium miner stocks climbing 9.11% YTD as of July 31, 2023. The growing embrace of nuclear energy is driving demand and sparking a resurgence in uranium mine operations. The U.S. opened its first new nuclear power facility in 30 years (Georgia Power's Plant Vogtle) and is actively legislating to reduce dependency on Russia's nuclear supply chain.

Sprott Energy Transition Materials Monthly

Growing Urgency to Modernize U.S. Power Grid

Given increased electricity demand and the risks posed by climate change, the U.S. power grid desperately needs modernization. There is an immediate need to expand the grid’s capacity, increase its resilience and support its most vulnerable components – the transmission and distribution lines. This is driving the development of energy storage systems and V2G (vehicle-to-grid) technology and is a major copper demand driver.

Interview

Investment Opportunities in the Energy Transition

John Ciampaglia discusses the energy transition on Nasdaq Trade Talks with host Jill Maladrino. Ciampaglia explores transformative investment opportunities in the energy transition, from the explosive growth of EV battery materials to the resurgence of nuclear energy. Discover how the shift toward decarbonization and critical mineral supply chains is fueling long-term market potential.

Sprott Precious Metals Report

Central Banks Flex Gold Market Muscle

In the first half of 2023, the gold bullion price rose by 5.23% despite competition from a euphoric equity market. Even with contrasting approaches, central banks and investment funds became the main players shaping the gold market in the first half of the year. Central bank buying drove demand, and gold is reverting to its historical role as a significant reserve asset as central banks seek to diversify amid geopolitical uncertainties.

Sprott Radio Podcast

Where Will the Gigafactory Feedstock Come From?

Joe Lowry, aka Mr. Lithium, joins Ed Coyne to walk us through all things lithium, including where ”Elon's first principle's rhetoric falls off the side of the table”.

Educational Video

Copper: The Essential Power Player in the Energy Transition

As the world seeks to reach net-zero targets and transition to cleaner, renewable forms of energy, copper is a requirement—but the amount of copper needed to successfully facilitate the energy transition is staggering. Learn about this critical mineral, its uses and how copper miners may be well positioned to benefit from increased investment in the low-carbon and renewable energy sector.

Sprott Uranium Report

Supply-Demand Gap Ignites Uranium Rally

Uranium markets rallied in June with the U3O8 uranium spot price adding 2.61%. U3O8 has climbed a healthy 15.95% YTD, while most other commodities have lost ground. Greater focus on the uranium supply-demand gap helped boost uranium mining stocks in June, with junior miners up 18.88%. Positive momentum in reshoring supply chains continues, given looming sanctions on Russian uranium.

Sprott Critical Materials Monthly

EV Battery Independence and the New U.S. Manufacturing Supercycle

Energy transition metals miners posted strong results in June, with uranium mining equities leading the group. The U.S. is entering the early stages of a manufacturing supercycle driven by massive energy transition investment, which includes building a secure and resilient domestic EV battery supply chain. The U.S. and EU are likely to replace China as the primary drivers of future metals demand, as China's two-decades-long commodities dominance has likely crested.

Special Uranium Report

Key Facts about Spent Nuclear Fuel

Chemical reactions of fossil-fuel plants release more radiation into the environment than the operation of nuclear energy plants — 10 times more. Most nuclear-industry waste is relatively low in radioactivity, and only a small amount is produced. Estimates put the total waste from a nuclear reactor supplying one person's electricity needs for a year at the size of a standard brick.

Sprott Radio Podcast

Uranium Update from Per's Cabin

Just back from the World Nuclear Fuel Market 49th Annual Meeting, Per Jander joins Ed Coyne for an update on uranium markets. The theme was “Mind the Gap”, not a nod to the London Underground but rather the pressing need for increased uranium production as countries ramp up nuclear power capacity.

Sprott Uranium Report

Uranium Remains Resilient, While Threats of Nationalism Rattle Equities

The U3O8 uranium spot price gained 1.58% in May,* increasing from US$53.74 to $54.59 per pound as of May 31, 2023. Uranium has posted a healthy 12.99% year-to-date return as of May 31, and continued to show strength and diversification relative to other commodities, which declined 13.16% YTD (as measured by the BCOM Index).

Sprott Precious Metals Report

Geopolitical Risks Enhance Gold’s Role as a Reserve Asset

Gold attempted to breakout above $2,050 in early May before drifting lower as the U.S. debt-ceiling drama deepened and the U.S. dollar strengthened. At the same time, global central banks have been accumulating gold at a record pace. This highlights gold's role as a neutral reserve asset that has the potential to mitigate increasing counterparty risks amid escalating geopolitical tensions.

Sprott Critical Materials Monthly

The West Moves to Weaken China's Hold

Lithium and lithium miners staged a sharp rebound rally in May and were the positive exception among critical minerals. The sector was weighed down by China's faltering recovery, ongoing global growth concerns and the U.S. debt ceiling drama. China’s dominance in critical minerals poses risks to the West’s manufacturing base and national security, highlighting the need for onshoring and friend-shoring energy transition supply chains.

Interview

BENZINGA: Steve Schoffstall Discusses Uranium and Energy Transition ETFs

Sprott’s Steve Schoffstall joins Benzinga’s Michael Murray and Anne-Marie Baiynd to discuss uranium, lithium and Sprott’s energy transition ETFs—including URNM, URNJ and LITP on Benzinga’s State of the Markets: ETF Capital Insights.

Sprott Precious Metals Report

Gold Rides Higher on Recession Fears

The gold market continues to be bullish as the probability of a recession rises, regional banking stress resurfaces and the Fed seems determined "get inflation down to 2%, over time". Globally, we are entering a more challenging period featuring subpar economic growth, increasing risks to systematic financial stability, stubbornly high inflation and rising geopolitical risks. Against this backdrop, we believe gold should perform well, even if the U.S. debt ceiling disaster is averted.

Sprott Critical Materials Monthly

Nationalization and Surging M&A Highlight Secular Strength

The long-term secular growth outlook for energy transition materials got several boosts in April, despite tepid performance for the month. Chile's decision to nationalize its lithium reserves reinforces the metal's role as a global strategic economic asset. M&A activity has heated up in the copper mining sector with lofty bids, including Glencore's $23 billion rejected offer for Teck Resources at a 20% premium.

Sprott Uranium Report

Uranium’s April Breakthrough

The U3O8 uranium spot price climbed 6.01% in April, closing the month at $53.74. The U3O8 price reacted positively to China's bullish comments about its ambitious plans to expand its nuclear energy capacity to supply 18% of its electricity needs by 2060, up from 5% today. YTD, the uranium spot price has gained 11.24% as global acceptance of nuclear energy increases and positive momentum builds within the uranium industry.

Sprott Radio Podcast

Hello Copper!

Host Ed Coyne and Nick Pickens from Wood Mackenzie discuss the bullish outlook for copper in 2023. Copper is key to electrical power generation and transmission, and sits at the center of the energy trilemma: the challenge of balancing cost, sustainability and security of supply.

Sprott Critical Materials Monthly

How Deglobalization is Changing the Dynamics of Securing Critical Minerals

Commodity prices weakened in March in reaction to financial system stress and recession fears. As deglobalization accelerates, unfettered access to critical minerals is not likely to last. The old system of free and fair access to commodities, including critical minerals, is moving toward one marked by interregional competition, and unstable availability and pricing. China has moved aggressively to acquire critical minerals in the past 20, but we believe the West has near-unmatched capabilities and is a formidable competitor.

Sprott Uranium Report

Uranium Proves Resilient in March

The U3O8 uranium spot price fell slightly in March, from $50.85 to $50.70. YTD through 3/31/2023, uranium has gained 4.93%, demonstrating resilience relative to other commodities (down 6.47% as measured by the BCOM Index). Along with other equities, uranium mining stocks fell in March, victims of the selloff following the U.S.'s biggest banking crisis since 2008. Positive headlines on nuclear power restarts continued in March.

Sprott Precious Metals Report

Gold Bulls Run Faster as Fed Tackles Banking Crisis

In March, gold posted its highest monthly close since July 2020 and rounded out a solid Q1 2023 gain of 7.96%. Gold is now up 21.38% from last autumn's low (9/26/22) following the most aggressive central bank purchases in decades and gold investment flows catalyzed by the U.S. banking crisis. We are very optimistic given that many significant long-term bullish macro factors for gold have become stronger, while some shorter-term cyclical gold bearish factors have faded.

Sprott Radio Podcast

Phone A Friend - How Uranium is Bought and Sold

Treva Klingbiel of TradeTech and Per Jander at WMC Energy join Sprott's Ed Coyne to discuss the inner workings of uranium pricing and contracts, the future of nuclear energy generation capacity and the development of SMRs.

Educational Video

Nickel: A Battery Metal Powering the EV Revolution