If you have trouble viewing the webcast above, please try this: RIA Replay Link.

Download PDF of Slide Presentation

February 21, 2023 | (69 mins 21 secs)

As the world sets aggressive goals to reduce reliance on fossil fuels and move to cleaner energy sources, critical minerals — including uranium, lithium, copper and several others — will be essential. And due to years of underinvestment, demand for many energy transition materials will outstrip supply. The investment opportunity may be powerful. Our webcast will cover:

- Global commitments and rising trends in cleaner energy and energy security

- The growing demand for low-carbon energy alternatives and the proliferation of electric vehicles (EVs)

- How critical minerals such as uranium, lithium and copper drive energy generation, transmission and storage

- The supply-demand scenarios for critical minerals and the potential opportunities for miners

- Opportunities for investors to access these investment opportunities with Sprott Energy Transition ETFs

Featured Speakers

Chief Executive Officer

Sprott Asset Management

Director, ETF Product Management

Sprott Asset Management

Senior Managing Partner, Global Sales

Sprott Asset Management

Webcast Transcript

Millissa Allen, RIA Database: Cover Slide

Ed Coyne: Slides 2-5, Introduction

Ed Coyne: Thank you, Millissa. Thank you all for joining today's webcast. We're very excited to bring this topic to you all. It's a topic that has been discussed around the globe in the last couple of years, but in the last year it's really heated up. And so, we're excited to bring this to you today, and we appreciate your time and attention.

Before we go into this, I want to introduce our two special guests. Some of you have been on our webcast in the past, and you've heard from both John and Steve in the past. John Ciampaglia is our CEO at Sprott Asset Management and is a Senior Managing Partner at Sprott Inc. John has almost 30 years of investment industry experience, and since 2017, serves as CEO of Sprott Asset Management. John plays an active role in development, acquisitions, and marketing of new and existing strategies.

Before joining Sprott in 2010, John was a Senior Member at Invesco Canada. Prior to Invesco, John was at TD Asset Management. John earned his bachelor’s in economics from York University and is a CFA charter holder.

Also with us today is Steve Schoffstall, who's a director of ETF Product Management at Sprott Asset Management. Steve joined Sprott in April of 2022 with over 18 years of experience in the ETF industry. Previously, Steve was a senior ETF Product Manager at ProShares Advisors. Prior to joining ProShares, Steve held varying positions at Vanguard. Steve earned his bachelor’s in finance and his MBA from Penn State University. And I appreciate you both joining us today on today's webcast. Thank you for being part of this.

Before we go into today's webcast, which is "Energy Transition Is Here. Is Your Portfolio Ready?" I'd like to talk for a moment about Sprott as a firm. Sprott is a unique firm and is a global leader in precious metals and real asset investments. Sprott has over 21 billion in assets under management and is a publicly traded company that trades on both the New York Stock Exchange and the Toronto Stock Exchange under the ticker symbol SII.

At Sprott, we offer exchange listed products, managed equities and private strategies. Within our exchange listed products, we have over 16 billion in assets under management, and we allow investors to allocate directly to physical bullion trusts, whether it's gold, silver, platinum, palladium, or more recently, physical uranium. We also offer the opportunity for investors to allocate to senior large-cap mining stocks, as well as junior small-cap mining stocks, whether it's in the gold and silver market or the uranium market.

Today we're going to be talking about a whole new suite of ETFs that we're offering as well for investors to allocate to many of the energy transition minerals and metals that we will be talking about later today.

We also have a suite of managed equities with over 2.4 billion in assets. In this suite, we offer our flagship U.S. Mutual Fund, the Sprott Gold Equity Fund with a ticker symbol SGDLS.

And last, but certainly not least, we have a suite of private strategies at 1.9 billion, which offers bespoke credit investments to mining and resource companies, and is made up of a cohesive team of both credit and finance experts.

With that, I'd like to now turn everyone's attention to today's webcast. Our first speaker is John Ciampaglia. John's going to cover "Energy Transition: The Global Move to Cleaner Energy." Once again, John, thank you for joining us today.

John Ciampaglia: Slides 5-21 The Case for Critical Minerals

John Ciampaglia: Yes. Thank you everybody for making time to hear about our story about the energy transition. For us at Sprott it really started about two years ago when we made our first significant investment in the uranium sector by acquiring a fund. And as we started to talk about uranium with different institutions around the world this term "Energy Transition" was consistently being used in my conversations with institutions. It really dawned on me that these institutions that I would say are fairly sophisticated, different institutional fund managers and family offices around the world, were thinking about the investment horizon as it relates to energy through a very different lens. They clearly put uranium in this category of energy transition. As we engaged more and more with them over the following months, it became very clear to us that this topic was much more encompassing.

If I think about transitions and history, the reality is our economies and the way we live our lives day to day, have been transitioning for the last couple hundred years. If you think about what we we're doing for energy 200 years ago, well, we were burning wood, and then we discovered we could burn coal, and then we could burn oil, and we could burn natural gas. Each time we did a transition, it was a cleaner form of energy, it was a more dense form of energy, so we could get more energy out of a smaller volume. And then, obviously we developed many new technologies to discover and extract more cost effectively to make these forms of energy more accessible.

In the last 50 years or so, we've also continued that transition. We've adopted nuclear energy; we've adopted solar, wind, geothermal, and more recently, hydrogen. This isn't about an anti-fossil fuel message, fossil fuels obviously play an instrumental role in our economies and our daily lives. I clearly couldn't have come to work today without fossil fuels. And, this is about a transition in our infrastructure and energy systems that have been in place for the last, say, 150 years, and that we think are going to continue to evolve to cleaner forms.

And I thought it was important to set the stage for when we use this word 'Energy Transition,' and clean energy is really about trying to diversify our sources of energy so that we are building, more energy with lower carbon footprints.

Why is all this important? Well, if you go to the next slide, it's really about CO2, that's carbon dioxide emissions. This goes back very long in time. And you can see that historically over the last 200 years, really since the beginning of the industrial revolution, that the amount of CO2 in our atmosphere continues to rise. And yes, there have been some periods where we saw a lowering of CO2, most notably with the COVID 19 pandemic as economies shut down, but the reality is greenhouse gases continued to rise despite our overall efforts to shift to lower carbon emitting energy sources. And there's a number of reasons why, as the world becomes more populated and wealthier and more energy is consumed, but there's still many parts of the developing world that are energy impoverished and would like to share the same kinds of lifestyles that we enjoy in North America.

Governments are focused on this number and scientists because they believe there's a strong link between the amount of CO2 in our atmosphere and changes in the climate. Changes in climate brought about mainly by changes in the jet stream, which can cause – for example, where I live in Toronto, it should be snowing much more than it has been. But, we find that instead of getting snow, we get a lot of rain and ice in the winter of late as the climate seems to be changing.

What are governments around the world doing? Well, 93 countries have pledged net-zero targets. This is basically governments either through law or different policy targets, putting in decrees that they will attempt to lower their overall greenhouse gas emissions by moving to cleaner forms of energy, energy efficiency, adopting new technologies. It's a real wide range of different avenues to try to reduce overhaul greenhouse gas emissions.

In 2021, it was very important that the U.S. returned as a signatory to the Paris Climate Agreement. And from my perspective, in October 2021, at the COP26 forum, that was really when things seemed to accelerate in terms of governments making some pretty significant policy decisions around energy, nuclear energy was a huge beneficiary of those policy shifts, and we see many more policy shifts happening for a number of different reasons.

How are all these net-zero targets basically playing out in our energy systems? Well, we believe will play out in a number of different ways. First of all, there's going to be a transition away from fossil fuels, both in absolute terms, and I think in our relative basis where if we're going to be building new energy capacity, there's clearly incentives to do those with cleaner forms, and I'll get into more detail as we go.

Renewed interest and nuclear power, because it's zero greenhouse gas emitting, obviously is receiving a huge renewed interest globally, particularly in the last 12 months as the dual concern related to energy security has become more front and center for governments around the world.

Moving to electric vehicles and transportation. Shipping is obviously a big focus, and with that obviously requires batteries, whether those are small scale-batteries or large-scale grid batteries that we use to offset intermittency of things like renewable energy.

These are the key areas that we're trying to focus on. Obviously, some parts of our economy are harder to de-carbonize than others, but around energy generation, energy transmission, and energy storage are really the three buckets that we like to think about this thematic.

Let's move a little bit to the next section and talk about where critical minerals fit into this whole thematic. We see a big investment opportunity before us, because all of these clean energy transitions require significant amounts of critical minerals. And critical minerals are basically a broad term that is defined slightly different by different parties, but it really in essence describes, "What are the key minerals that form the raw materials that we will need to enable this transition to happen?" And we like to think of it as a suite of different critical minerals. We've listed some of these on this page here. And they each play a different role, whether it's related to energy generation, energy transmission, or energy storage.

For example, for energy generation, so that's generating electricity, you have nuclear energy, you've got solar power, wind power, hydropower, geothermal. And you can see by the size of those circles, those blue circles, those illustrate how intensive or how important those respective minerals are to that particular item. For energy transmission, that's categorized under electricity networks. You can see copper is really the biggie there.

Under electric vehicles, obviously the batteries are the key part of the vehicle. They require very large amounts of lithium, copper, nickel, manganese, cobalt, graphite, and some rare earths, which are highly magnetic.

And then, obviously things like solar power require a lot of copper. But you know, many people don't know that about 10% of all the silver that gets produced in the world every year goes specifically for solar panels. It's a key element of solar panels.

Let's just keep going in the interest of time. We've kind of identified this suite of different metals and materials that are critical for this transition. And as a result, we see the demand for these critical minerals is going to grow exponentially.

On this slide here, you can see the International Energy Agency back in May 2021. They forecasted a couple of different scenarios. One is called the current stated policies scenarios. Those are basically governments around the world that are putting into different laws or implementing different energy policies. And they we're saying, "Yes, these policies materialize as envisioned.’

What impact could there be on the demand for some of these critical minerals? You can see lithium is the clear winner. Under the demand for current stated policy scenario, you can see that the demand for lithium itself would increase 4000%. It's astounding. It's not a coincidence that the best performing commodity over the last two years has been lithium. Lithium has been really the key element for EVs that has been under the most supply constraint and bottleneck.

But as you can see from some of these other bars, graphite is going to grow exponentially. Cobalt, nickel, manganese, rare earth, which is a whole collection of minerals that are very hard to pronounce. And then, finally, copper, we envisioned seeing material growth over time as more electrification occurs as more EVs consume copper, et cetera.

This is why we think there's a very interesting investment opportunity here, because if you think about the goals that everybody would like to accomplish in terms of de-carbonization and transition, we're going to require significant amounts of these minerals to deliver against them.

Moving to the next slide. As I mentioned a little earlier, there's still a large part of the world that we describe as energy impoverished. They would love to have the lifestyles we enjoy and the energy abundance that we enjoy. And we think that energy demand is only going to increase, which is going to put further pressure on this goal to de-carbonize. Unfortunately, energy production from things like coal is still very prevalent, and in many emerging markets, because it's very cheap, coal is very plentiful. In more developed markets, we've moved away from coal, and we've shifted to cleaner sources. Coal is going to remain a fairly sizable part of our energy grid. I think most people are surprised when I tell them that 20% of all the electricity produced in the United States is still from coal. Most power plants west of Mississippi are still very coal dependent. But as I said, we see a big shift happening, and as these plants come to end of life, they will be decommissioned and they're being replaced with cleaner sources and particularly renewable energy, and we think increasingly nuclear power.

Let's move to the next slide. This is just a snapshot of the United States, and obviously the United States is not expanding, its energy footprint as quickly as say, an emerging market. But it gives you a little bit of a sense of how this shift is already underway. If you look at the new capacity planned in the United States in 2023, for example, you can see that 54% of all the new energy capacity planned in the United States is actually going to be solar. Solar obviously is very dependent on your location. You're seeing in the southwest, a lot of solar installations are being put into place. You're seeing nuclear power finally being added to the grid. In Georgia, there's a large power plant coming online this year.

Wind is obviously a part of the mix. And you can see natural gas plants are still being added. Why? Because, natural gas is significantly cleaner than coal. And then, battery storage is another part of the grid solution. We see this trend happening around the world where you're not seeing new coal plants being built, with the exception of places like China and India. Most of the world is trying to move away from those legacy forms of energy because they're less safe and dirtier.

Let's go to the next slide. I'm going to talk a little bit about electric vehicles. And I think, you have to take a global perspective when you think about electric vehicles because quite frankly, most of the world outside of North America seems to be ahead of us in terms of adoption of electric vehicles. Last year, we think electric vehicle adoption experience a tipping point. A tipping point is basically a point where you achieve a certain level of adoption whereby it then accelerates. We've seen this in the adoption of other technologies, and we think EVs and other hybrid vehicles have hit this point in the last 12 months.

This is obviously happening because of incentives, this is happening because of consumer choices, and quite frankly, choice. If you look at a lot of the EVs that are being produced right now, and the EVs that are going to be coming to market over the next few years, they are much more attractive than the first generation and second generation EVs that are available to us.

The OEMs [original equipment manufacturers], these are the car companies, are making huge investments to transform their production lines to have a greater balance between two EVs. For example, General Motors, their goal is to produce 1 million EVs sold by 2024 and have 30 new models. Ford and Honda, for example, they want to have 40% of their new car sales, EV, by 2030. Toyota, VW, all the major car companies have different goals of a similar nature. Right now they're going through a massive process of transforming their production to accommodate this expansion and growth.

The EU Parliament last week actually voted to ban internal combustion engines by 2035. That's not existing cars in the road, this would be new car sales. This is a very lofty goal, and I'm not convinced they'll even be able to achieve it because the supply chains that have to be built out in order to meet this 2035 deadline, I think are pretty substantive. Nonetheless, governments around the world are providing incentives and OEMs are responding to this shift to electric vehicles.

Let's talk a little bit about why that's important. While EVs are a key driver of critical mineral demand. As we see greater adoption of EVs, we need to acquire more critical minerals. If you view it as the amount of the volume of the material per vehicle, and this just illustrates a typical conventional car, an internal combustion engine, about 75 pounds of critical minerals would go into a typical car. But, if you look at an electric vehicle, you can see that number goes up to about 450 pounds per vehicle.

Why? Well, you have a whole lot of copper, you have a whole lot of nickel, cobalt, and these are very heavy materials. It’s not just the volume or the weight of the materials, it's obviously the value of these materials is pretty significant. And this is why, when you look at the cost of an EV, they are higher than a typical internal combustion engine car because they require many more materials to be built. This is one of the reasons why governments around the world are providing incentives to try to normalize the cost differential between typical gasoline and diesel cars to EVs.

Let's move to the next slide and give you a little sense. If you peel back the cross section of an electric vehicle, just to give you a sense of where they go. Lithium-ion batteries, I think is a term most people are familiar with. When you look at a typical EV battery, it's made up of a cathode and anode. The cathode is the most expensive part. These are primarily nickel based battery, so they are comprised of nickel, cobalt, manganese, and lithium. Lithium is the universal element across all the battery chemistries. You cannot basically remove lithium out of your battery. No matter what, it is kind of the universal element across all battery chemistries.

The anode is made up primarily of graphite, and then the motor has some rare earth related to their magnetic qualities. And then obviously, there's a whole lot of copper inside these battery cells and EVs. This is where the demand is coming. As more EVs are built, you can see the direct relationship to the different components of the car.

I'm going to shift a little bit to policy. And I'm going to talk a little bit about — I've labeled this slide strategic priorities, but I think as I reflect on it, I think it really comes down to national security and energy security. This is really driving a huge part of this thematic. It really started back in June, 2021 when the White House published a report entitled "Building Resilient Supply Chains, Revitalizing American Manufacturing and Fostering Broad-Based Growth." This report focused on a number of key industries that the U.S. government was very focused on reshoring, which is basically building local supply chains. And they were related to semiconductors, pharmaceuticals, batteries for EVs, and other large scale application, critical minerals and materials. That could be for energy transition, also can be for the defense sector.

This, to us, was one of the key policy decisions signaling that this reindustrialization theme is underway. About a year after that, in June, 2022, the Minerals Security Partnership was signed by the US, EU, UK, Japan, South Korea, Australia, Canada, Sweden. This was a partnership with the goal to strengthen the global supply chains for battery metals specifically.

And you might ask, "Well, why all this focus and fanfare on this? Why are governments so focused on this?" The answer is that, countries like China control very large parts of these supply chains today, and there are growing concerns related to national security that we cannot basically outsource all these critical supply chains to countries that one day may not be so friendly as trading partners. Obviously, the invasion of Ukraine by Russia has heightened these concerns about being cut off from strategic minerals and supply chains, specifically related to uranium and nuclear fuel processing, but other minerals such as nickel palladium, other things where Russia is very dominant. More recently with the Inflation Reduction Act, which I acknowledge has one of the worst labels ever, if you actually peel inside of that piece of legislation, it is really about this reassuring theme, providing financial incentives and credits to encourage development of local supply chains, renewable energy, nuclear energy, electric vehicles, subsidization and adoption. There are big, big policy shifts going on around the world. And this is not just the United States, this is becoming a much more global phenomenon.

This is also cascading down to the individual public companies. And, on this slide here, I've just kind of created some recent headlines around recent developments. I find it fascinating that the Department of Energy is extending loans to lithium companies that are trying to develop deposits in state of Nevada, for example, I don't know Lithium was one that not too long ago, got a significant loan.

Redwood materials. They've secured a $2 billion Department of Energy loan to boost its EV battery operations. They're also located in Nevada. And, the more recent one is General Motors. They recently announced about a week ago, they're going to invest 600 million in an equity investment in a company called Lithium Americas. Why? Because they are very focused on securing the critical minerals they need to build out these supply chains. I think a few years ago, if you said to an investor, you know, OEMs are going to make equity investments in mining companies, they would laugh you out of the room. But this is now the reality. People are so focused on building out these supply chains because some of these policies are actually in laws in different countries, whereby they will no longer be able to produce ICEs in the future that companies are taking action and securing their own supply.

There is a bit of a race here going on right now. Could the government involvement in the sector create some distortions? Yes, that's absolutely possible. Governments should not be getting involved in free markets, but the reality is, this is now a national security and energy security issue, and they are providing the incentives and the policies and the support from a regulatory and permitting process to make this become a reality. We think this is a really fascinating development, and one that no one really thought about a year or two ago.

Let's keep moving along in the interest of time. One of the areas that we've received tremendous investor interest in the last two years has been in uranium. And why does this really tick off two of the major boxes related to energy transition and energy security? First of all, nuclear has the highest energy capacity of any form of energy, so yes, the world is trying to build more wind and solar because it has a lower carbon footprint, but as you can see from the left side of the chart here, they don't have high-capacity factors because the wind doesn't blow all the time, and obviously the sun is intermittent as well.

You need to offset that intermittency with reliable, what we call baseload energy forms, and baseload energy only can come from sources of energy that we can control. We can control the amount of output from a coal fired power plant or a natural gas fire power plant, or a nuclear power plant. And so, these are the ideal complements to offset intermittency of renewables.

Energy emissions as measured by greenhouse gas by per gigawatt hour. You can see that solar, wind and nuclear really win the race here. They're very low emitting. And at the very bottom you see coal, it's the highest. And this is one of the forms of energy that the world is trying to migrate away from.

The other part of the uranium story is about supply and demand. It's a critical mineral. It cannot be thrifted away, it cannot be substituted. And one of the key parts of the thesis related to uranium is about the supply-and-demand fundamentals. As you can see there, we have been essentially under-producing uranium for a number of years and expect to, going forward.

Why? The world basically closed a lot of the uranium mining capacity as the price of uranium collapsed following a multi-year bear market, and now we're trying to play catch up and reopen mines and start new mines to ensure that there is security supply for the growing number of nuclear reactors around the world. There are about 434 nuclear reactors around the world. The United States still has, despite not really adding a lot of capacity for many years, still has the largest fleet of nuclear reactors, produces 20% of all U.S. electricity, and over half of the low greenhouse gas electricity annually.

The price of uranium hit bottom at around $18 a pound. And more recently has been trading between $50 and $60 depending on contract term. We think that the incentive price still needs to continue to grow higher in order to develop new uranium mines, and that's why uranium is part of this energy transition design that we've put together with these products that Steve will talk about.

And just to flip to the next slide, I'll talk a little bit about copper. Copper is obviously kind of the backbone of the story. It's critical for transmission of electricity, but also used extensively, as I said, in EVs and wiring. And you can see that, again, we have another critical mineral where copper demand is expected to outpace copper supply.

Why is the copper supply lagging? Well, it's been lack of investment. You have low commodity prices for years and years and years, and that does not incent any new exploration, it doesn't finance new development of mines, and so, you get yourself into a hole, and it's hard to come back out. This lack of investment has clearly, I think, had an impact on many different commodities, which is why I think commodities have come back to life the last couple years. And then more specifically in the case of copper, many of the biggest and oldest copper mines in the world that are located in places like Chile, they're coming to end of life, the grades, that's the percentage of ore of copper in the ore continues to fall. That makes it more expensive to find. And you know, at the end of the day, unless the prices of these commodities go up, you won't have an incentive price to get financing and to build new capacity. We think higher prices cure many of these supply deficits that we see in a number of commodities. And with that, I'm going to pass it back to Ed.

Ed Coyne: Thank you, John. That was extremely insightful and I know you're going to stick around for us. I was just looking at the Q&A box, we've got 63 questions currently, which we're going to do our best to cover as many as we can, but please stick around for the back end of this webcast as well to address some of those questions. With that, I want to now shift gears and turn it over to Steve. Steve's going to cover Sprott Energy Transition ETFs and give more of an overview on the funds themselves and talk about how you can potentially look at these ETFs as a way to help diversify your portfolio. So Steve, thank you for joining the webcast today.

Steve Schoffstall: Slides 22-29 Sprott Energy Transition ETFs: Overview of Funds

Steven Schoffstall: Thanks, Ed. Happy to be here. John spent a good deal of time going through the investment themes behind the Energy Transition. Here on the next slide, we'll begin talking about the different investment opportunities that are available to take full advantage of those themes.

When we started about with the Energy Transition suite, we really wanted to create a suite that offered the ability for investors to access pure-play exposure to the minerals that are critical to the world's transition to clean energy. And what we mean when we say 'pure-play exposure', we're really talking about those companies that have a lot of their revenue or their activity dedicated to that individual part of the sector that they're looking to be involved in, whether it be lithium or uranium, so we wanted to provide that. We think that's one way that really separates our suite apart from other investment products that are out there. And, we also wanted to focus on the companies that are providing the, whether it's physical materials or the mining companies that are actually bringing these products to market, these critical minerals to market.

There are a number of challenges that take place when you're looking to access this part of the market, and we'll talk through that in the coming slides. But I did already touch on the pure-play nature of this market. One of the things that we brought to this process when we created this suite was our decades of experience that we have in the mining industry. And we really wanted to leverage that and bring about a product suite that we thought really provided the exposure that someone looking to access this theme would be interested in.

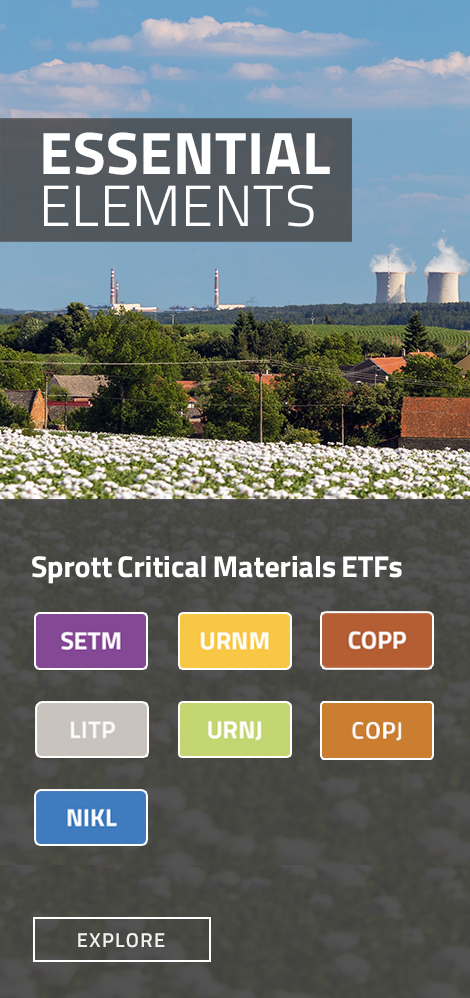

We worked with Nasdaq to create an index series, so currently the Nasdaq portion of our suite covers four ETFs, which we'll talk about here in a minute, but we're really focused on providing some optionality within the energy transition space for investors.

As far as our lineup goes, with the advent of URNM, we do have five ETFs dedicated to the space, as well as one physical trust that we have out there. And what you get with the ETFs is you really do have the convenience and liquidity that is offered for accessing these global markets, which may be difficult for individual investors or smaller investors to access on their own. We provide the diversification through the form of an ETF, which you will just buy in your brokerage account and hold it alongside your stock or bond investments that you already have.

On this slide, we outline a little bit of our product offering and with a focus directly on the energy transition suite. We really wanted to provide some optionality, as I said, to investors interested in this overall theme. We do provide some a focus on individual metals. John mentioned about two years ago how we really took a step into this space with the physical uranium trust. This is a fund that allows investors to trade a close end fund, and it is backed by U308 uranium. It is publicly listed on the TSX and is also available to U.S. investors as well.

Last April, we added to our lineup with URNM, the Sprott Uranium Miners ETF. This is a pure-play U.S. listed ETF that provides exposure to uranium miners and physical uranium. If you don't want a hundred percent of your investment to be in physical uranium, but you do believe in this story and would like to have access to physical uranium in your investment, URNM actually does have about a 15 to 17% investment in physical uranium. That provides the physical allocation coupled with the pure-play mining allocation.

Most recently, we rounded out our uranium offering, when earlier this month we launched the Sprott Junior Uranium Minors ETF, ticker URNJ. This is a junior product that really now kind of completes our uranium lineup from the physical to the all-cap offering, and now the junior offering for investors that are so inclined in that space.

Also, earlier this month, we launched our Sprott Energy Transition Materials ETF, ticker, SETM. This is our broadest offering in the energy transition space, and may be most suitable for investors that want access to the energy transition theme, but may not have the background or expertise to make a call on one of the individual critical minerals.

And then finally, we offered two additional ETFs, earlier this February as well. It's been a busy month with four fund launches, which the first of those is the Lithium Miners ETF, ticker, LITP, and then, the Junior Copper Miners ETF, ticker COPJ. And again, these are providing pure play exposure, which isn't readily available in the market prior to the launches of these products.

In the next two slides, we'll talk a little bit more about the critical minerals that are included in SETM, so that will be our focus, and the index construction process. But before we get into index construction, when we set back and looked at "What did we want to include in the energy transition space?" John mentioned this wheel that we think of kind of three different buckets. We have the energy generation, transmission and storage aspect that we think through.

So starting in that green box, the green part of the circle, we're focused on mainly the battery metals. While most people are somewhat familiar with lithium, cobalt and nickel, combined, those metals account for about 23% of the minerals by weight in a typical EV battery. While maybe most top of mind for most investors, it's by far not the largest component by weight when we look at storage batteries.

When we add manganese and graphite, we now get to a part where we're accounting for about 56% of the minerals in a typical EV battery. It really allows us to go past just those big three that most people are familiar with and capture more of the storage market.

We talked about copper earlier and his primary use of conducting electricity. It really does as the chart, John showed the dots on it. It really does span across all three of these buckets. Anytime that you have electricity, usually copper's involved, given its ability in conducting electricity and its durability. When we start looking on the generation side of the things where copper's concerned, anytime that you replace a power plant with either wind or solar, you could expect about two to three times the copper relative to a gas fire plant, is needed for the construction for that wind and solar. As we do transition away from gas or other fossil fuels to generate our electricity, copper seems to play a bigger role in that.

And as a firm, one way we've wanted to differentiate our lineup is by including uranium in our critical minerals space, so we do believe that uranium is key to the energy transition. And as John mentioned, its ability to generate reliable baseload energy with very little CO2 emissions. Because of this, the European Parliament actually added Nuclear Energy to its list of green investments in 2022, and Canada also did add uranium to its list of critical minerals in 2022 as well. We do see on an international level from governments starting to recognize the role that nuclear is likely to play in the longer-term energy transition.

To determine which companies make the cut. On the next slide, we'll talk about our Index Construction Process and exactly how we're delivering value through this partnership with Nasdaq. We'll focus on this discussion with the Sprott Energy Transition Materials Index, the Nasdaq Sprott Index, which is the index that is tracked by SETM. There are some nuances between each of these indexes, such as the minimum market cap for inclusion in the index or deviations to the waiting scheme. But talking through the process for SETM's index will give you an understanding of the overall selection process and how rigorous the process to get included in the index actually is.

We start at the top of the investment universe. On a global scale, we look at about 90,000 countries or more which off the bat are considered in our equity universe. And from there, we're reducing that universe by looking at third-party databases, competitive analysis and research that we're performing in-house. Once we establish this new eligible universe, we calculate what we've referred to as an Intensity Score. And this Intensity Score is a proprietary calculation that is used to measure how much of the firm's revenue or the operations are dedicated to whichever critical mineral that we're examining.

To arrive at that Intensity Score, we research and quantify each potential company's exposure to the energy transition material, and we filter out companies that don't meet our index criteria. In the case of SETM, a company must score 50% or higher. Roughly speaking, that means 50% or more of their operations or assets have to be dedicated to one of the energy transition materials that we saw on the previous slide.

Once we have an index selected, at that point, we have to go through the constraint process. This usually includes minimum and maximum market caps. We also have some daily trading volume requirements for a company to be included. And one of the things we're doing in this index series is we are excluding China Asia from being added to the index. And to reduce index turnover, we also apply buffers at the index constituent level for market cap and trading volume requirements. And the thought there is, particularly if you look at Junior Uranium, for example, if a company has been doing really well and grows above the maximum market cap, as long as it's within a tolerable range, it is eligible to remain in the Junior Minor Index.

And then finally, once we have all these securities and the waiting set for the index, we go through this process actually twice a year on a semi-annual basis in June and December to make sure that we're capturing the full investment universe for each one of these critical minerals.

After going through the construction process, we're left with the index represented in the screen here that you see for SETM. It's important to note that SETM is the only ETF that provides pure-play exposure to a broad range of critical minerals and mining equities that are essential to the transition to cleaner energy. These critical minerals, we've touched on some deeper than others. They include uranium, copper, lithium, nickel, cobalt, graphite, manganese, rare earth, and also silver. The expense ratio for SETM is 65 basis points. And when we look at the index holdings of the fund, we'll see that it's about a 40, 40, 20 split when we look at large and mid-cap, both having about a 40% allocation, roughly 35 to 40%, and small-cap around 20% allocation. It is fairly well-diversified amongst market capitalizations. There are currently 111 securities in the index, so it's fairly broad in its approach. And, as I mentioned earlier, is a good option for someone who may not have a full grasp on the individual minerals, but wants to play the energy transition investment landscape.

In SETM's case, we do have a cap on individual minerals within the index at 25% to any one material. The current constituents show copper at about 26%. The reason that's above the 25% cap is because at those semi-annual index rebalances, the cap of 25% is applied and throughout each half of the year, it may fluctuate based on market conditions, but every June and December, that cap is reset back to 25%.

When we look at the combined exposure of copper, lithium, and uranium, you can see it makes up roughly 75% of the index. It's important to note that while cobalt is very important to the energy transition, particularly in the battery storage segment, you can see it has about a 32 basis point weight in the index currently. There are very few companies out there that actually only mine cobalt that would meet our strict criteria, rather, it tends to be a byproduct of nickel and copper mining activity. To the extent that we do have copper at 27% and nickel at 9%, it's likely that some of those mining companies will also provide exposure to cobalt, whereas there's not just a large pool of specific cobalt companies.

One of the questions that we get typically is, with the energy transition, it kind of doesn't really fit into any one of the buckets so cleanly, "What's the best way that somebody can utilize this?" Probably, the most obvious allocation for Energy Transition ETFs would be for commodities exposure. While these are equity based and with the exception of our Sprott Physical Uranium Trust, you know, they are providing exposure to commodities through the business that the underlying companies are engaged in.

Given the size of many of the companies in these strategies, we talked about SETM about the 40% mid-cap and 20% small-cap, they may very well fit into a small-cap and or a mid-cap bucket. If that's something that's in your mandate, there may be a spot there as well.

As we look to shift focus away from fossil fuels, and I just want to reiterate something that John said earlier about how that reliable baseload power is something that is needed to back up for times when the sun doesn't shine, the wind doesn't blow, and we may be a drought and hydro is producing. We do believe that there's a baseload that needs to be in place to account for those times. This does have a potential to fit into your energy sleeve. You know, whether it's through the generation on the uranium side or the wind turbines to rare earths or silver for the solar panels.

Someone looking to diversify their existing exposure to equity holdings might find that their exposure to these elements is really underrepresented in their current portfolio, and they may benefit from adding, whether it's SETM or one of the other funds to their alternative allocation.

While ESG isn't one of our screening processes for these ETFs, the materials mined by the underlying holdings are actually essential to the future of achieving ESG goals set forth by nearly a hundred nations. If that is something that's important to you, you know, this really is driving the energy transition forward. Without the mining, you can't really have an energy transition, so that's I think something that often gets overlooked when people start talking about the energy transition, they may show a little skepticism around the premise of it. But, you know, it's a fact of the matter, if you want to transition, you have to have mining to be able to do that.

Given the structural growth that we are expecting in the energy transition space, we're seeing that through investments on a global scale, we're seeing companies do that on their own accord or as John mentioned, accessing different funding options from governments, there is a strong case to be a part of a thematic portfolio. And one of the things we like to talk about when we do start talking about a thematic allocation is we really look for those trends that are much longer term in nature. This isn't expected to be a flash in the pan that is here today, gone tomorrow, but given the amount of investment, which we'll talk through briefly on the next slide and what we're seeing across the globe, this has some legs to stay around for the long term.

And finally, technology. I know we spent most of the time talking about this suite in the context of the energy transition, but if you step back a little bit and think about history up until 2015, consumer electronics were actually the largest consumer of lithium. That's the point where EVs took that mantle over from consumer electronics, but they do still have a considerable need for lithium and lithium-ion batteries. There is a technology at place here that we did not focus on that.

Just to wrap up and summarize here briefly. These are pure-play indexes that we've created with Nasdaq. We want to make sure investors are getting access to the investments that puts them in what we believe to be a good position to take a part in this theme. We are the first suite of the energy transition ETFs to provide that pure-play exposure. That pure-play aspect is one thing that makes us different. It's not watered down with companies that might be a little farther down on the supply chain, maybe consumers of these critical minerals, but they are the ones bringing it to market.

As John did, he detailed government net-zero actions and the actions that the governments are taking to transition us away from fossil fuels. When we look at the investment, it really is a mind boggling dollar figure. Last year, some estimates have put the overall global investment at about $1.1 trillion that was invested in the energy transition sector. And that's significant because for the first time, the energy transition investment equal data fossil fuels. So this is a massive market, and I think that also lends the fact, with 1.1 trillion still coming into fossil fuels, that's likely not something that's going to go away altogether. But this large investment, it was a 31% increase over what we saw in 2021.

For the rest of the decade, if we were to step back and say, "Well, what kind of growth can we see going forward?" From 2023 out to 2030, we could expect to see about three times that amount invested on an annual basis if we are going to be on track to meet our 2050 net-zero goals that many governments are working towards. Every year that we don't hit that, I'll call it, 3.9 trillion or so, it just puts us a little further behind. When you get to the 2030s, that annual investment actually jumps up to about 6.9 trillion on average if we were to stay on pace for 2050 targets.

And this brings us to our fourth point. We did talk about the upstream aspect of the funds and how we're really investing at the top of the supply chain with those that are bringing the minerals to market. It's just another thing that we believe where those companies are most well positioned to benefit as price setters as opposed to consuming the minerals, but rather benefiting from the increases in price.

And then finally, John touched on this a little bit. I won't stay on it too long, but world governments have gotten involved in several ways. If you look at the Inflation Reduction Act signed into the law last year, there's almost 370 billion that went towards improving energy security and the clean energy transition. Where it relates to clean energy, you're talking about 270 billion for loans and grants and tax incentives, for wind, solar, and storage. And about half of the funding for nuclear and EVs will account for another 15 to 16% of the overall investment. The Infrastructure Bill provided $65 billion for renewable energy projects. And in October of last year, the current administration awarded about 2.8 billion in grants to boost U.S. production of EV batteries and the minerals used to build them. And plans are also being made to provide 5 billion to fund EV chargers on national highways. So that would be money that goes to the states to build out that electric charging grid.

The Repower EU plan is the European Commission’s plan to make and accelerate the clean energy transition and to make Europe independent from unreliable suppliers. They also want to do away with the price volatility that are typically associated with fossil fuels. As part of that plan, about 300 billion is being provided to support investment in energy transition reforms.

Finally, when we look at sustainable finance policies, a lot of asset managers and other firms that are lending money at banks are starting to take into account ESG factors when making those lending decisions. And we're seeing this issue take a more prominent role at the World Bank, the IMF, and the European Union, which just led a little more credence to the overall narrative that we have. And with that, Ed, I'll turn it back to you.

Wrap Up

Ed Coyne: Thank you, Steve. And, thank you for that insight. You know, we're going to make, I was looking at the questions coming in, so we're actually getting close to a hundred questions, so we're clearly not going to have time to answer all those. Rest assured, we will be responding to everyone via email and or phone calls to address each and every question.

In the event your question is not answered on today's webcast, a member of the Sprott Asset Management team will reach out to you directly. If you would like to have a conversation to further discuss the ideas that were covered during today's event, please click the blue confirm button in the meeting request box on your screen. And with that, I'll send it back to you, Ed.

Important Disclosures

An investor should consider the investment objectives, risks, charges and expenses of each fund carefully before investing. To obtain a fund’s Prospectus, which contains this and other information, contact your financial professional, call 1.888.622.1813 or visit SprottETFs.com. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

Diversification does not protect against loss. The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the fund, typically in blocks of 10,000 shares.

The Sprott Active Metals & Miners ETF is new and has limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott ETFs. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.