The global transition to clean energy is driving demand for critical minerals like uranium, copper and battery metals such as lithium and nickel. These minerals are crucial for nuclear power, electric vehicles, wind, solar, and hydropower.

Video Transcript

Todd Rosenbluth: Todd Rosenbluth, head of research here at VettaFi. Thanks for joining us for our latest webcast. This one's sponsored by Sprott Asset Management. We're here to talk about rethinking energy exposure. Now, the transition to cleaner energy is something that I'm sure you hear a lot about throughout the media. It's especially true given the global legislation and a focus on 2050 for net-zero carbon emissions. These goals involve a shift towards electric vehicles, getting more of those on the road. Still, there's a lot of uncertainty about what this means for investors and advisors and how this can help them with their energy allocation. I'm excited we'll dive into this topic on a couple of different levels with the team at Sprott.

There are a few things I want to go over with you before we dive into the overall presentation. We will ask lots of questions of my fellow panelists, but you might have some of your own that you want us to cover. Please submit those using the Q and A box in the bottom right corner of the screen. We'll get to as many of those questions as we can. Now, if you're looking to bone up on the material on this topic, the team from Sprott has put together great resources in the folder widget. There are white papers, fact sheets, and information specifically on the gold, silver and critical minerals channel. That's available on the ETF Trends website.

Lots of great insight for you, and I know you'll learn a lot throughout this presentation because, as you'll see on the next slide here, I'm joined by Steve Schoffstall, who's part of the Sprott Asset Management product management team. He's been with the company for a while but previously was part of the ProShares team, focusing on their dividend growth suite and product launch initiatives. Steve, I'm excited to have you join us. Thanks a lot.

Steven Schoffstall: Great to be here, Todd. Thank you. As you mentioned at the onset here, the energy transition is making itself known in the media, and the way we look at that is it's not anything new. If you go back throughout history, we've been transitioning our energy sources. If you go 150 or 200 years ago, we mostly burned wood in coal to generate our energy. By the time we entered the 1950s, we started to see natural gas, at least in the U.S., produce about 17% of our electricity. By the time we moved into the '60s, we started to see oil move front and center on a global scale, and that's when nuclear energy started to get commercialized. This transition is just the next phase that we're entering.

As we go through this deck here, what you'll see is there are several opportunities that are emerging with a focus on cleaner energy, and that can mean a lot of different things to different people. We'll get into that as we go, but from our standpoint, there are a few things that we see happening as we transition to those net-zero global commitments. 97 different countries now are targeting net-zero emissions, some as early as 2050, which seems to be the standard benchmark. This transition means, at least in our opinion, we don't expect to go completely away from fossil fuels. We could particularly, as we move through the next decade, decade, and a half or so, we could see a growth in our usage of fossil fuels. We do think that in the long term, looking several decades out, there is a place for those fossil fuels, particularly natural gas in our energy supply chain.

One of the things that we think we may start to hear more about, and we're seeing it across the energy transition industry and when we look at what governments are doing, is a renewed interest in nuclear power. We'll talk a little bit about that as we go, what leads us to believe that we're at a new renaissance time with nuclear power, and how it's being embraced now on a more global scale than, say, five or 10 years ago. Then finally, as it relates to the global transition, on the battery storage side and particularly EVs, we expect to see significant demand for a number of critical minerals from those. The battery storage is the batteries in the electric vehicles, but also does back up renewable energy sources like solar, wind, and hydro. With that, we can move to the next slide and discuss some of the investments we're starting to see in the energy transition.

If we look back at 2022, that was really a banner year for global investment in the energy transition. If we look at some Bloomberg research and other research that's been out about last year, we see that about $1.1 trillion on a global scale was invested in the energy transition. That's significant for two reasons. One, it's the first time that we breached that trillion-dollar investment mark. Secondly, it also put investment in line with what we were seeing for fossil fuels, so two significant milestones last year. Within that, we saw almost 500 billion dollars on a global scale dedicated to electrified transportation. That would be everything from EVs to building out charging infrastructure to light commercial, electric vehicle applications and things that follow suit there.

Some estimates show that if we look at the International Energy Agency, they could expect up to 350 million electric vehicles on the road globally by the start of 2030. That's one of the key drivers behind the energy transition here and would represent about a 45% annual increase as we go through the decade. We do have this large-scale investment that we're seeing on a global basis, but we're also seeing a trend where particularly Western nations brought on by the COVID-19 pandemic and the war in Ukraine are looking to re-shore some of their energy sources. That can be sources that we haven't traditionally had large industries for, like battery metals, the mining and manufacturing of batteries, and then also uranium. We're seeing that come on.

When you look at this slide we have about $400 billion (official estimate) of clean energy funding from the Inflation Reduction Act, which is the largest clean energy act in the past year in the U.S. Some independent estimates, say that number could grow closer to a trillion dollars by the end of this decade. There is a lot of money floating around, not just in the U.S., and I think we're at a different point where a lot of this investment has been happening overseas and it's just now starting to make its way here.

Moving forward to the next slide, what does that mean from a practical perspective? Since the Inflation Reduction Act was passed, the number of projects here in the U.S. has exploded. There's about 80 billion dollars of private investment that has occurred. If you look at those large red circles, those represent battery manufacturing. We have a battery belt emerging from Michigan down to Georgia. We have several factors that are coming into play. We have federal money coming in and supporting these industries. We have battery makers, particularly in South Korea and Japan, investing money here to take advantage of tax incentives either now or into the future. Then we also have state governments that are trying to win business and bring these new industries to their local economies, so they're also providing tax incentives, and you're seeing that a lot in the south and then also in the northern Midwest. Moving to the next slide.

When we talk about the energy transition, we tend to think of it in three different phases. We have energy generation, and within that bucket, we have things like uranium, silver and rare earth metals. I think Uranium's self-explanatory for its use in nuclear power. A lot of people aren't familiar with the usage of silver in the energy transition. About 10% of all silver that's mined is used in the energy transition, particularly around solar panels. Given their permanent magnet properties, rare earth elements are used in wind turbines and electric vehicles. Then on the battery storage side, we have lithium, nickel, cobalt, graphite and manganese, all of which play important roles in battery storage. Tying these two pieces together is copper. Copper is one of those elements that conducts electricity very well. It's light, highly recyclable and could be used in many applications. Pretty much anything with electricity that passes through it will have some amount of copper in there, so we tie that together with those elements.

Moving to the next slide, we can briefly discuss how they're used within the energy transition. I mentioned uranium. I think we're good there with the nuclear standpoint. What I want to do is focus on copper just for a second. Copper is one of those things, as I mentioned on the previous slide, that does filter across the entire energy transition. Anytime we put up a solar or wind farm, all of that electricity has to reach the grid, and that's all being done by copper. As we increase our usage of EVs, we start to see the need to build out these electrified charging stations and infrastructure. Again, that's all going to be run by copper.

Then you see a significant amount of copper in the production and building of EVs. If you look at a normal gas-powered car, you'll see about 48 pounds of copper in that car. For an electric vehicle, that jumps up closer to 180 to 190 pounds of copper, so there is significant resource demand on the EV side. We talked about all the other minerals that we saw and listed the five battery metals that we look at. Different battery chemistries can impact to what degree they're used in EVs. Still, electric vehicles are driving this transition, along with electric power generation, and they go hand in hand. We must build additional generation capacity as we increase our electricity demand for charging EVs. Next slide, please.

Todd Rosenbluth: Steve, I think this next slide will talk about just the growth we've seen in the electric vehicle space and what it means for critical minerals.

Steven Schoffstall: That's correct. There used to be the adage, and I've seen political cartoons in the last five, or six years, it would show somebody plugging in their EV and on the back of the outlet is a coal-fired power plant. This notion of, the EVs are clean, but the energy that they're using to power those EVs isn't very clean. What this is depicting is that as you start going throughout the first half of this decade here, is we're seeing an increasing amount of our electricity come from clean energy sources. Currently, that's about 40% on a global scale. Once we reach about 2050, the expectation is that we'll be above 75, nearing 80%.

With that, we're seeing EVs ramp up in the second half of this decade. We'll talk about in a few slides here what that means for lithium, but as the EVs are increasing in adoption, we're seeing the power for those EVs is increasingly coming from clean energy sources. To give you an idea, last year, we had about 16 and a half million EVs on the road globally. This year, we're closer to 25 or 26 million EVs, so a significant jump—about 60% just in the last year. As I said earlier, we might see about a 45% increase throughout the remainder of the decade. Next slide, please.

I want to talk a little bit about the lithium demand. What we're seeing, and it's evident, if you track that yellow line, that's what we're seeing from a lithium supply perspective. We expect to see over to about the middle part of this decade a small surplus in lithium as we move through 2025 or 2026. As we start to see greater adoption of EVs, we expect not quite a hockey stick increase in the amount of lithium demanded, but it's a very significant increase in lithium.

Several things are going to factor into meeting that demand. One will be increasing the number of mines that are producing. Right now, we have a significant permitting process in most mining jurisdictions around the globe in which it can take 10 to 15 years, or perhaps even longer to get a mine from discovery to operational where it's starting to contribute meaningfully to the lithium supply. I think a lot of work must be done to expand the mines. On the miner side, we're starting to see more mergers and talks of acquisitions as those miners are looking to procure those mines that are already either operational or near operational.

We're also seeing at the same time automakers face mandates as they're expanding their EV aspirations, particularly as it relates to those either selling vehicles within California, which is basically everyone, or producing within Europe. Many mandates are starting to pile up, requiring these automakers to phase out their internal combustion engines for new vehicles by 2035. Some automakers are being a little more aggressive on their own accord and looking at a 2030 date or even a 2040 date on the less aggressive side. Still, we expect to see a significant increase in the amount of lithium demanded as we move into the next decade and we must look for new ways to shift that supply and demand paradigm. We're starting to see some new emerging technologies, which we won't delve into here, where we can extract lithium from sources that weren't an option before and in some cases, alongside oil and gas wells. With that, I think we can move to the next slide.

I mentioned nuclear upfront. One of the things that sticks out about our view on the energy transition relative to maybe some other asset managers is we think that nuclear energy is going to play a very prominent role as we move through the transition. We're starting to see significant evidence to support this. If you look back, the last time we had significant momentum in the uranium market was around 2011, around the Fukushima incident in Japan. At that point, many countries started planning to phase out their nuclear power plants, including Japan, South Korea and some European countries.

What we've seen now, within the last year, six months or even a few years, is some of those same countries, like Japan, and South Korea are extending the life of their existing nuclear power plants, and they're also making plans in some cases to add to the nuclear power plants. Japan's bringing on several plants that have been offline since they turned them off in 2011, and we expect that to continue to contribute to the increase in nuclear power on a global scale.

What I wanted to include in this presentation was just a quick view on a global scale—what does nuclear energy and its growth look like as we move through the transition? Currently, there are about 435 reactors that are online. I think many people are surprised to know that about 100 of those are in the U.S. Prior to a new reactor coming online in Georgia five or six months ago, we haven't built new reactors for a few decades. You're starting to see this push internally in the U.S. to embrace nuclear energy. We expect to see another nuclear power plant in Georgia, another reactor come online either in the first or second quarter next year, and we're starting to see bipartisan support and, investment and commitments from our government to incentivize nuclear energy.

One of the driving factors behind that is Russia, a large player in the uranium enrichment process. With their ongoing war in Ukraine, it's something that we're trying to pull away from the Russian economy so that we can develop our own fuel sources here as it relates to nuclear. There are about a dozen or so bills at various stages going throughout Congress that are contemplating the best way to do that and incentivize local or friendly production, whether in Canada or Europe, of not only physical uranium but also enriched uranium. Next slide, please.

This is just a view of where we see the current supply and demand dynamics with physical uranium. Going back to 2011 or so, and even before that, a lot of the uranium that nuclear power plants were consuming was coming from this buildup of stockpile that happened during the Cold War. We were running off for the better part of two decades of this stockpiled uranium, and there wasn't a need to add significant mining capacity. When you fast forward to where we're at today, we start to see that uranium production capacity is looking to peak here in the next couple of years. We see this growing supply and demand gap, similar to what we see with many other critical minerals. There's going to be a lot of work that needs to be done to get these mines up and running. It's not an easy task.

If you go back to 2010 or 2011, the incentive price for which uranium miners could mine uranium profitably was about $50. That number is closer to 75 or $80 a pound for uranium today. To give you some context, since June, we've had a big run-up in the price of uranium. We're sitting at about

$70 a pound, so we're not quite at those incentive prices yet for more mines to make sense to start bringing more capacity on. Then, finally, one next slide.

Great. I wanted to take a moment before we get into the Q and A to focus on the energy transition options and how investors can take advantage of this potential opportunity. One is our physical uranium trust. We put this fund to market about a little over two years ago. It stores physical uranium. It's a closed-end fund. It's listed in Canada, and also trades OTC in the U.S. under ticker SRUUF. It's about a four-and-a-half billion-dollar fund that stores physical uranium, much like you might see with other gold ETFs where they store physical gold. This just houses uranium. Then, we wanted to provide a number of ways for investors to express their views in the energy transition.

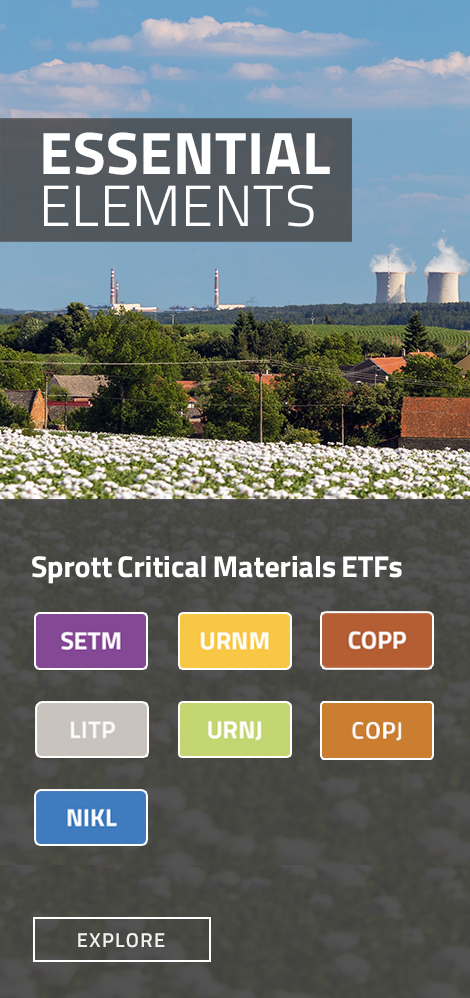

One of the things I like to tell investors we hear from is that the energy transition can be somewhat polarizing. Some people are in favor of it, some don't see the merits behind it, but at the end of the day, with the amount of money that we're seeing flow into the sector and the emerging companies that we're seeing, it's undeniable that there is this emerging investment opportunity there. We wanted to provide a few different solutions for those who want to potentially take advantage of that investment opportunity. SETM, which is our broader-based fund, it's the Sprott Energy Transition Materials ETF. That actually invests in those nine critical miners and producers of those nine critical minerals I mentioned earlier on that flywheel, covering the generation, storage and transmission of cleaner energy.

These are all pure-play strategies, and we're focusing upstream on the supply chain so we don't have to worry about which battery chemistry is going to be the predominant chemistry used by different auto manufacturers or if new technologies are coming out. All those technologies will harness the materials that these miners are bringing to market, so we wanted to focus on that upstream application and make sure that we're focusing on companies in ETM's case where at least 50% of their revenue is coming from mining those critical minerals or producing those critical minerals.

Just by way of index methodology, we go through a very rigorous process where we look at each individual company in the index, quantify how much of their revenues are coming from the different critical minerals, and then assign an intensity score. For example, suppose 80% of their revenues come from mining battery metals included in the index. In that case, approximately 80% of their float-adjusted market cap will be included in the overall index calculation and weighting scheme.

Then, for those wanting a little more targeted exposure, we have LITP, the only pure-play lithium miners ETF out there, which focuses on lithium miners. URNM and URNJ are complements to our physical uranium trust. URNM is an all-cap physical miners ETF, or uranium miners ETF. For somebody who may want some physical exposure to the miners or to the uranium, you'll get about 15 to 17% physical uranium exposure within URNM. URNJ is a fund that we launched back in February. It's listed on the Nasdaq, focused on those smaller producing or exploratory uranium mining companies and has had some really good success. That fund's already grown to about $150 million in assets and has been one of the top performing funds for the last several months as we've seen this uptick in uranium. It's done a nice job of capturing the move of the physical uranium market, but with the tilt of equities.

Then, finally, on the copper side, we have our junior copper miners ETF focused on the smaller copper miners and then the only nickel miners ETF out there. Not only are all these strategies pure-play, but no other funds exist catering to junior uranium, junior copper, or nickel miners. With that, Todd, I can hand it over to you for the Q and A.

Todd Rosenbluth: That would be great. We're going to put the poll question up for the audience. Do you plan on adding to or initiating a position in any of those Sprott ETFs that Steve touched on in the next six months? A simple yes or no would be great. While we keep that up, I want to combine a few different questions that came together. Green energy is a changing market. Do the funds provide exposure to emerging energy technology? What if technology changes and we need less lithium? I know it's a combo.

Steven Schoffstall: Sure. Going back to what I talked about, our strategy around these funds is to focus upstream, so those bringing the minerals out of the ground or bringing those minerals to market. From that standpoint, if there are new emerging green technologies and to the extent that they're using the same minerals, we would expect these funds to play a role in that because at the end of the day, they are supplying the minerals. One of the questions we get asked a lot about, and it relates to your second part of the question around new technology, is, well, what about solid-state batteries within EVs?

In actuality, those solid-state batteries, which many people point to as the next iteration, we're probably a decade to a decade and a half out from those being commercially viable. Still, they use a significant amount more lithium than our traditional lithium-ion batteries in today's EVs. To any extent, we would expect to see, in most cases, a lot of the same minerals being used and these ETFs and the miners that are held within these funds supplying those minerals. We would expect that to be well-positioned to potentially take advantage of any technological changes.

Todd Rosenbluth: Thanks. We might do one final question here. I'm in New York City. I don't see a lot of charging stations. I know electric vehicles require infrastructure. Is the lack of charging stations going to hamper EV adoption?

Steven Schoffstall: That's a great question, one we hear a lot. You don't see a lot of public charging stations. There are a number of private charging stations that are available. One of the things that is needed for that is to increase our infrastructure, which will mean a lot of copper. Not only does that mean copper for bringing out the transmission lines and allowing the EVs to be charged, but we also have to have reliable and renewable energy sources if we stay within that 2050 framework for net-zero greenhouse gases. That's one of the reasons we think nuclear energy has a very big role in the energy transition.

Solar is great when the sun's shining, and it can produce energy for parts of the day in different parts of the world where there's plenty of sunshine. Wind turbines are useful for areas that have significant winds that blow through and can power those, but nuclear energy is actually a clean and safe alternative that provides that base-load energy that's always on. You can dial it up, and you can dial it back to meet the energy needs. We're thinking that as we see more countries start to realize that nuclear power is going to be a major part of the energy transition, we're going to see that power, the EV infrastructure that we need. It might take some time to get there, maybe a little longer than what some projections are taking, but if governments and private companies are investing in that and committed to moving that direction, we expect that we'll get there.

Todd Rosenbluth: Well, thanks for that. I know you love all of your Sprott ETF children equally, which is why we didn't ask which ones people will buy, but just a broader subset of it, but exciting to see the broad lineup that Sprott offers. I know we didn't get to all of the audience questions. My apologies for that, but somebody from the Sprott team will certainly follow up with you if we haven't gotten to your question. Appreciate you sharing your expertise with me and the flexibility. We'll be tuning in next time, so thanks, everybody for your time today.

Steven Schoffstall: Thanks for having me.

Important Disclosures

An investor should consider the investment objectives, risks, charges and expenses of each fund carefully before investing. To obtain a fund’s Prospectus, which contains this and other information, contact your financial professional, call 1.888.622.1813 or visit SprottETFs.com. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

Diversification does not protect against loss. The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the fund, typically in blocks of 10,000 shares.

The Sprott Active Metals & Miners ETF is new and has limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott ETFs. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.