Let’s start with nuclear energy. It’s back!

After being unloved, forgotten and punished for a decade, it’s rising again. Some call it a nuclear renaissance but I like to think of it as a resurgence given the growing momentum.

Who would have thought that in just two years, public sentiment and government support would have shifted this strongly? Nuclear energy peeked out of the backstage shadows at COP26 in 2021. While the nuclear energy sector’s attendance that year was full of controversy, it marked the first public admission by governments that they had no chance of reaching net-zero targets without it. While there were outlier countries chasing energy unicorns, it was a watershed moment for nuclear.

By COP28, which recently concluded, nuclear energy took center stage with 22 countries pledging to triple their nuclear energy capacity by 2050. Wow!

Figure 1.

Source: Dean Calma/International Atomic Energy Agency.

From misplaced protests, misconceptions and exclusion, how did the nuclear energy rebirth come to be? A powerful combination of realities — geopolitical, economic and electron.

To quote Doomberg, “Energy is life.” A simple, yet powerful statement.

Without abundant, reliable and affordable energy, our day-to-day lives would be profoundly impacted. Energy systems are complex, globally integrated and, despite their massive size, can be impacted by geopolitical events.

Energy has been weaponized for decades, but let’s focus on the last 50 years. It was the OPEC-induced oil crises of the 1970s and 1980s that many of us can remember. This energy shock was the catalyst for a dramatic shift in energy policy adopted by many Western governments that led to the build out of nuclear energy.

Let’s fast forward to the energy crisis of 2022, which was created by Russia’s invasion of Ukraine. Unlike the OPEC oil crises, this one created more and larger shock waves because it impacted oil, natural gas and coal, not to mention other key minerals like nickel and palladium that Russia produces.

"What happened at COP28, the annual United Nations climate event held this year in Dubai was the greatest outpouring of global support for nuclear power the world has seen since the thunderous reception to Eisenhower’s Atoms for Peace call exactly 70 years ago,” wrote Seth Grae, President and CEO of Lightbridge Corporation and an ANS-badged COP28 delegate.

Most countries were impacted by the 2022 energy crisis, but Europe, the UK, Japan and Asia felt the brunt of it with sky-high energy and electricity prices resulting from their structural energy dependencies.

One country fared worse than others: Germany. Overreliance on Russian natural gas coupled with a foolhardy plan to prematurely phase out its nuclear energy proved to be a massive financial blow to its economy, wealth and citizens. An unfortunate and largely self-inflicted outcome.

Germany’s decision to gradually shut down its nuclear power plants was poorly thought out and naive. But there is a silver lining. It showed the world what happens when you sacrifice energy security for political ideals and aspirations that are not based on economic and electron realities.

Having committed to abandoning nuclear energy, Germany responded to the 2022 energy crisis by finding alternative sources of natural gas (LNG) and relying on, choke, coal. Not just any old coal, but lignite coal, also known as brown coal, which is the dirtiest kind.

Germany’s energy choices have been an undisputed disaster for its citizens, leading to massively higher energy and electricity prices, the potential deindustrialization of its economy and an electrical grid backed up by dirty coal.

I had to cringe when I learned that Germany is trying to implement an Energy Austerity Act in response to its ill-fated energy experiment. Not the most inspiring piece of new legislation. No doubt, governments around the world watched this drama unfold and revalued the numerous benefits provided by nuclear energy — security, reliability, affordability and baseload power.

Electron Reality

Let’s shift to electron reality.1 Renewables absolutely have a role to play in the energy transition but have to be deployed in the appropriate places and with a realistic contribution. Solar deployments are expanding at a record pace globally, while both onshore and offshore wind are suffering from a host of economic and electron realities.

As renewable energies scale, we are discovering a new challenge. The growing mismatch of energy production and demand over the course of the day. In several markets where the use of renewables has reached a saturation level, the cost of electricity from renewable sources can be zero or even negative when solar energy and/or wind are at peak production levels. Sadly, curtailments of renewable power are becoming more common to balance the grid.

What good is this if clean energy can’t be used efficiently? Yes, the race to develop large-scale energy storage systems is underway to address this mismatch but we have not yet achieved scalable and cost-effective batteries to store low-cost energy at peak times for use later.

Opportunity for Uranium

The global pivot back to nuclear energy creates opportunities and challenges. We need to rebuild supply chains that have long since disappeared. Everything from mining uranium, building nuclear power stations to reshoring the nuclear fuel supply chain will be of paramount importance. The good news is the pivot is already underway as the energy crisis in 2022 galvanized political will and unleashed market forces to break a lost decade of inertia.

“Growth in global policy support and demand for nuclear power, combined with the desire by many to ensure independent, secure sources of nuclear fuel, is expected to exert continued upward pressure on nuclear fuel prices,” said TradeTech President Treva Klingbiel.

The uranium price is responding, with spot rising from $48 per pound to $91 in 2023,2 and the term contracting price approaching $100 caps. While there is lots of chatter about the impact of financial players in the market, the price gains this year have clearly been driven by utilities which purchased the most uranium in 2023 since 2012. UxC3 estimates that utilities have contracted more than 160 million in 2023, which the industry considers replacement rate contracting. Also of note, nearly 42 million kgU (kilograms of elemental uranium) of conversion term contracting (the second highest annual volume in the past decade) and nearly 50 million SWU (separative work unit)4 of enrichment term contracting (the most volume booked since 2009)5 reflects a renewed focus on the security of supply.

I often refer to the period from 2011 to 2020 as the lost decade for uranium and nuclear energy. A prolonged bear market spawns legacy issues that take years to form and solving them often takes an equal amount of time. This lost decade impacted the whole sector from the building of nuclear power stations to the mining and processing of uranium, and the nuclear fuel supply chain. It is a big challenge, yet an even bigger opportunity. If we want to expand our nuclear capacity over the coming decades, we are going to need to produce a tremendous amount of uranium.

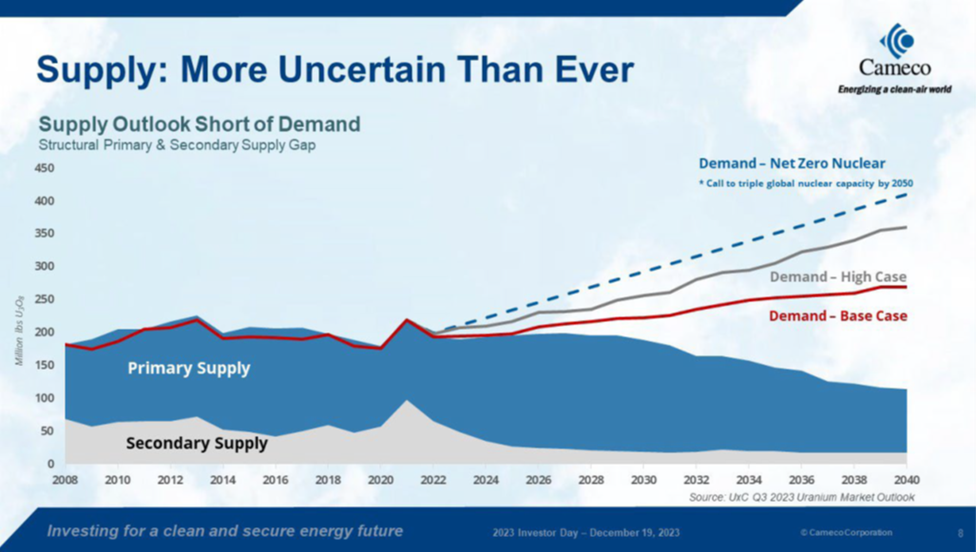

Where Will the Supply Come From?

We are often asked whether the price of uranium achieving/nearing incentive pricing levels will unleash a powerful supply response that will inevitably end the bull market. We don’t think so for the foreseeable future because of two realities. I’ll refer to my comment about it often taking “years to fix legacy issues” — a lack of investment in the sector during the lost decade coupled with long development lead times for capital-intensive and complex projects will translate into a slower-than-expected supply response. Cameco, at its Investor Day on December 19, 2023, estimated that there is a very significant level of uncovered utility requirements, adding up to 2.3 billion pounds of uranium through 2040.6

Figure 2.

Source: Cameco. Data as of December 2023. Included for illustrative purposes only. Past performance is no guarantee of future results.

Show Me the Drums

It’s “show me” time for the uranium mining sector. With the upward trajectory of the price of uranium generating renewed investor interest and government support, mining companies need to demonstrate that they can create real shareholder value by producing drums of uranium. The industry is responding by bringing a growing number of previously producing mines back online. This has been very encouraging and the natural first steps are to bring the easier pounds back into production.

While the cost structures and challenges vary from region to region, the real test for mining companies will be building new mines. This will not be easy as the lost decade has atrophied the industry’s collective workforce, knowledge and experience. The burden cannot solely fall on them. Governments need to step in and assist by streamlining the permitting process and provide the right financial incentives to help “crowd in” private capital. There’s little value if a world-class deposit stays stuck in the ground.

The Scramble to Reopen Uranium Mines

The easy pounds are coming out of the ground first. Restarts of existing uranium mines that have been on care and maintenance for as long as 2013 are slowly coming back to life after a one- to two-year ramp-up period.

Figure 3. Planned & Potential Uranium Mine Restarts

Source: Mike Kozak, Uranium Analyst, Cantor Fitzgerald, December 2023. Assumes certain mines will be restarted that have yet to be announced. Included for illustrative purposes only. Past performance is no guarantee of future results.

New Projects: Now or Never

We won’t fix the looming supply deficit without building new uranium mines, something we haven’t done in 20 years. Again, this is a big challenge, but a bigger opportunity as capital is finally flowing back into the sector. There are several promising uranium deposits that were discovered up to 10 years ago that we are hopeful will be built in this cycle. As corporate budgets for exploration return, new discoveries will be found. The industry doesn’t have a choice if it is to ensure diversified sources of supply. Mining is difficult and investors will need to be compensated for their risk capital. We don’t anticipate any major new mines to come online before 2030.

Stuck Between a Bear and a Dragon

In the last uranium cycle, we saw a massive supply response from Kazakstan. It emerged from a small producer in the early 2000s to becoming, what I believe to be, the equivalent of OPEC in uranium today. Naturally, as the current cycle progresses, one would ask whether Kazakstan can bring on meaningful new supply as a low-cost provider. Time will tell. State-owned Kazatomprom (KAP) has announced it will expand production to licensed nameplate capacity in 2025. This could go a long way to fill the looming supply gap, but the market remains skeptical. Ongoing supply chain issues have prevented KAP from hitting its currently reduced production goals since 2021. What if the supply chain bottlenecks are solved? It’s possible, but most of its future production has already been contracted forward to China. Russia has also secured part of future production from jointly owned deposits in Kazakstan to ensure their own security of supply.

Race Against Time

The nuclear fuel supply chain remains susceptible to further disruption. U.S. legislative efforts to finally sanction Russian nuclear fuel services appear to be imminent and could prompt retaliation by Russia. While uranium is the building block, conversion and enriched uranium are important steps in the fuel cycle. With Russia controlling meaningful percentages of global capacity in both conversion and enrichment, risk mitigation strategies by the West are underway with the reshoring of the supply chain. Western enricher Urenco announced it will expand its facilities in the U.S., Netherlands and Germany, while Orano will expand its plant capacity in France. On the conversion front, the long-awaited restart of the Converdyn facility in the U.S. is helping to alleviate the bottleneck that has helped support rising uranium prices since 2022. Cameco will also ramp up production to capitalize on record conversion prices.

What’s Next?

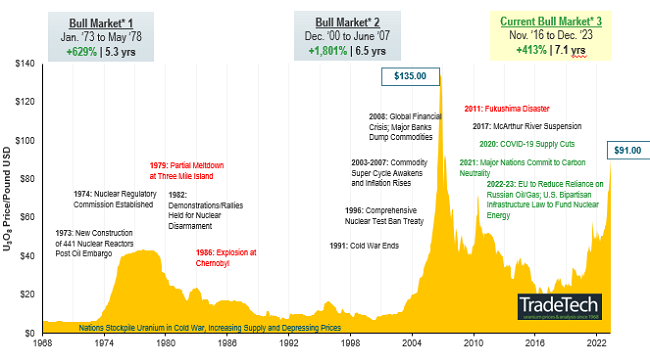

With the spot price of uranium recently reaching $90 per pound, we believe we have hit another inflection point in this bull market. Uranium contracting by utilities is accelerating, ending an extended era of inventory destocking. Security of supply is now the focus and priority. Some utilities appear to be well covered, while others that questioned the wave of market signals since 2021 are less so. Geopolitical risks remain a wild card that could create a market calamity.

The industry will require significant capital investments to meet its ambitious expansion plans. Thankfully, investor interest in the sector is growing globally as the opportunity becomes better understood and the legacy stigma fades. As the sector grows and recapitalizes, it will attract ever larger institutions, drawn by a compelling investment thesis and improving liquidity. While 2023 was a momentous and rewarding year for nuclear energy, uranium and the miners, we remain bullish on the long-term prospects for the sector.

Figure 4. Uranium Bull Market Continues (1968-2023)

Click here to view enlarged version

Source: TradeTech, month-end prices. Data as of 12/31/2023. TradeTech is the leading independent provider of uranium prices and nuclear fuel market information. The uranium prices in this chart dating back to 1968 are sourced exclusively from TradeTech; visit https://www.uranium.info/. Included for illustrative purposes only. Past performance is no guarantee of future results.

Footnotes

| 1 | “Electron Reality” refers to the science of clean energy, with all forms relying on the flow of electrons to generate electricity. The "electron reality" underscores the interconnectedness of different clean energy sources and the importance of optimizing electron transport throughout the energy chain. |

| 2 | Source: Tradetech, December 23, 2023. |

| 3 | UxC, LLC (UxC) is one of the nuclear industry’s leading market research and analysis companies. |

| 4 | The Separative Work Unit (SWU) is a unit that defines the effort required in the uranium enrichment process, in which uranium-235 and -238 are separated. |

| 5 | Source: UxC Weekly, December 18, 2023. |

| 6 | Source: Cameco Investor Day, December 19, 2023. |

Important Disclosures

An investor should consider the investment objectives, risks, charges and expenses of each fund carefully before investing. To obtain a fund’s Prospectus, which contains this and other information, contact your financial professional, call 1.888.622.1813 or visit SprottETFs.com. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

Diversification does not protect against loss. The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the fund, typically in blocks of 10,000 shares.

The Sprott Active Metals & Miners ETF is new and has limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott ETFs. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.