For the latest standardized performance and holdings of Sprott Rare Earths Ex-China ETF, please visit REXC. Past performance is no guarantee of future results.

Key Takeaways

- Strategic, Not Just Industrial: Rare earths have become critical geopolitical assets, underpinning defense, advanced technologies and energy security.

- Rare Earth Demand Is Accelerating: Growth across defense systems, consumer electronics, AI, electric vehicles, and energy is boosting long-term demand for rare earth elements.

- Ex-China Supply Chains Are Emerging: China’s dominance over rare earth mining, refining and magnet production exposes supply chains to disruption and is driving the U.S. and its allies to rapidly build resilient, ex-China alternatives.

- A Compelling Investment Opportunity: This global realignment is creating powerful tailwinds for producers outside China, opening the door for targeted exposure.

Rare Earths Move to the Center of Strategic Policy

Rare earth elements (REEs) are critical to many strategic sectors of developed economies, including defense, high-tech industries and energy, making securing their supply chain a top national priority. China dominates the rare earth market by controlling roughly 70% of global mining, over 90% of refining capacity and the vast majority of magnet production.1 Specifically, governments and corporations are increasingly prioritizing secure, non-Chinese supply chains. Total investment across defense, the energy transition and AI is up 78% since 2020.2

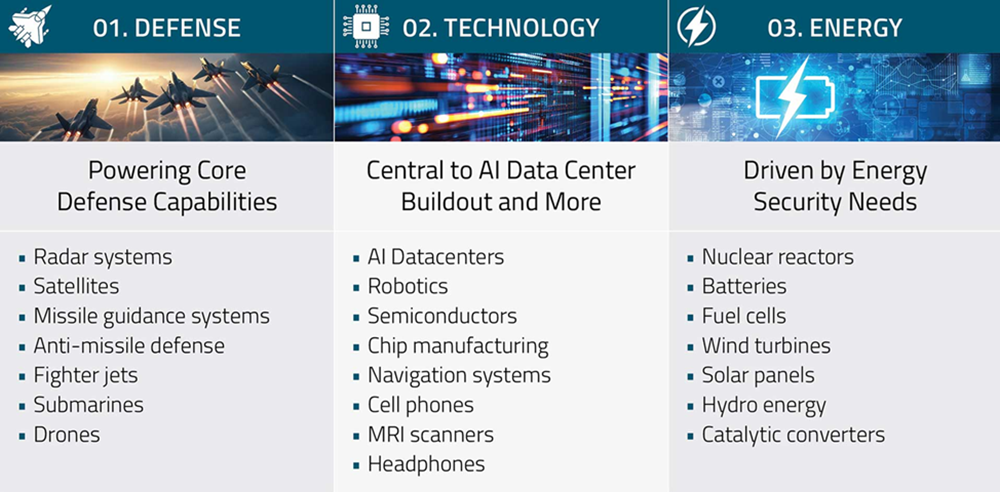

Figure 1. Why Rare Earths (REEs) Matter

Source: Sprott Asset Management.

What Are Rare Earth Elements?

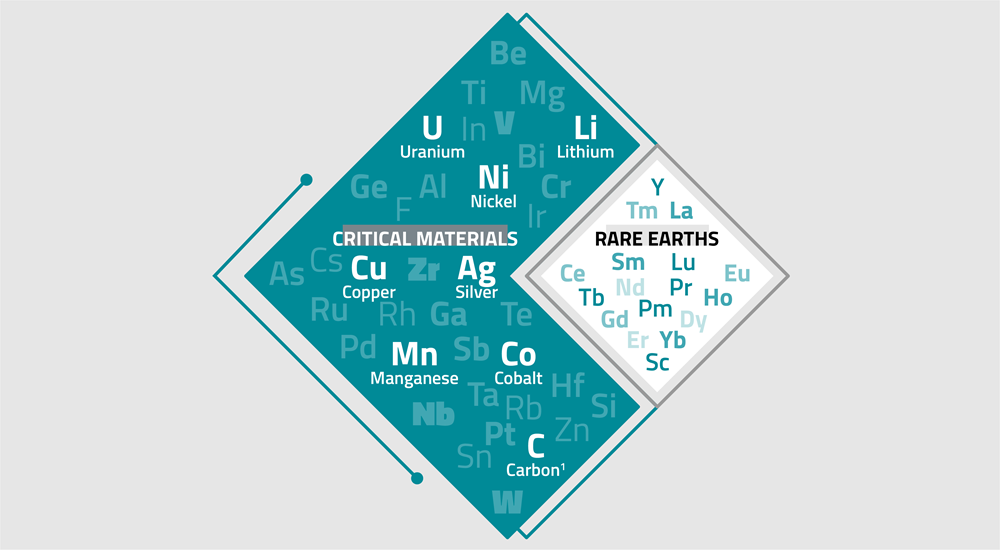

Rare earth elements are a subset of critical materials, consisting of 17 chemically similar elements essential to high-performance technologies. Critical materials—including uranium, copper, silver, lithium, nickel and rare earths—are essential inputs for electrification, energy storage, infrastructure and industrial production and are vital to economic stability and national security. Rare earths play a uniquely important role within this broader group and have distinct magnetic, catalytic and optical properties.

The largest industrial use of rare earth minerals is the production of permanent magnets, which account for over 80% of global demand by value.3 Rare earth magnets can be up to 2 to 7 times stronger than standard ferrite or ceramic magnets, making them the strongest permanent magnets available.

Figure 2. REEs are a Subset of Critical Materials

* Note: Graphite—reflected in Sprott’s list of critical materials focus—is an allotrope of Carbon.

Source: Sprott Asset Management.

Aubundant but Economically Challenging to Mine

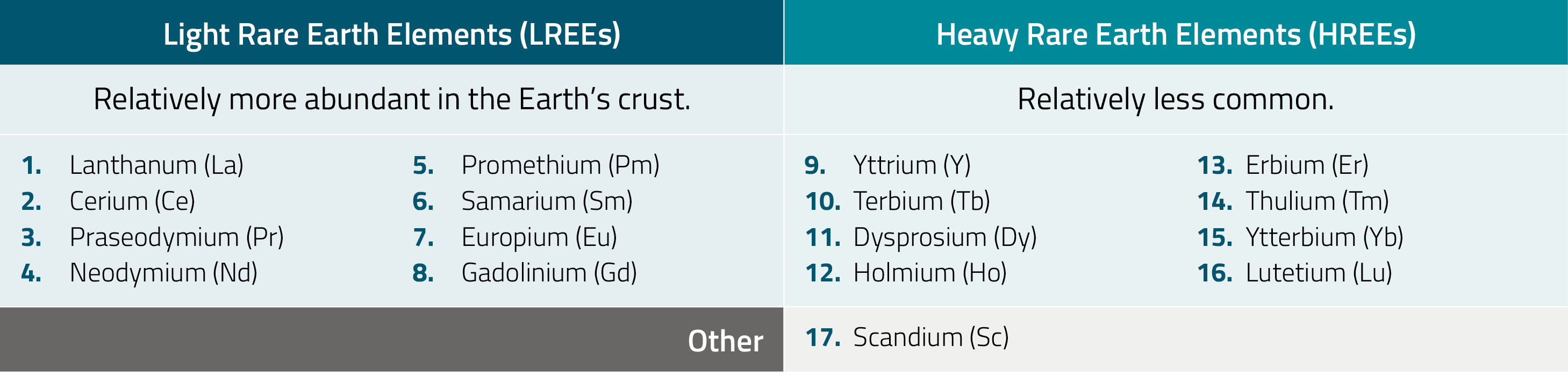

REEs are relatively abundant in the Earth’s crust, but they are dispersed, making most concentrations too low to support a mine’s viability. They are rarely found alone and occur as trace elements grouped together.

Deposits may lean towards higher groupings of light REEs or heavy REEs. These elements are not only commonly found together but also share similar properties, making their separation one of the most challenging and energy-intensive tasks in modern chemistry.

Rare earths’ properties are non-replaceable in many applications. They are indispensable for high-tech applications as their properties provide very specific characteristics. Small quantities can be mission-critical inputs with an outsized impact.

Figure 3. Light vs. Heavy REEs

Strategic REEs Demand Is Accelerating Across Multiple Sectors

Defense

REEs are essential inputs for modern defense applications because they enable high performance on platforms and are difficult to substitute. Permanent magnets are the core demand channel into defense, because they enable compact, high-torque motors.

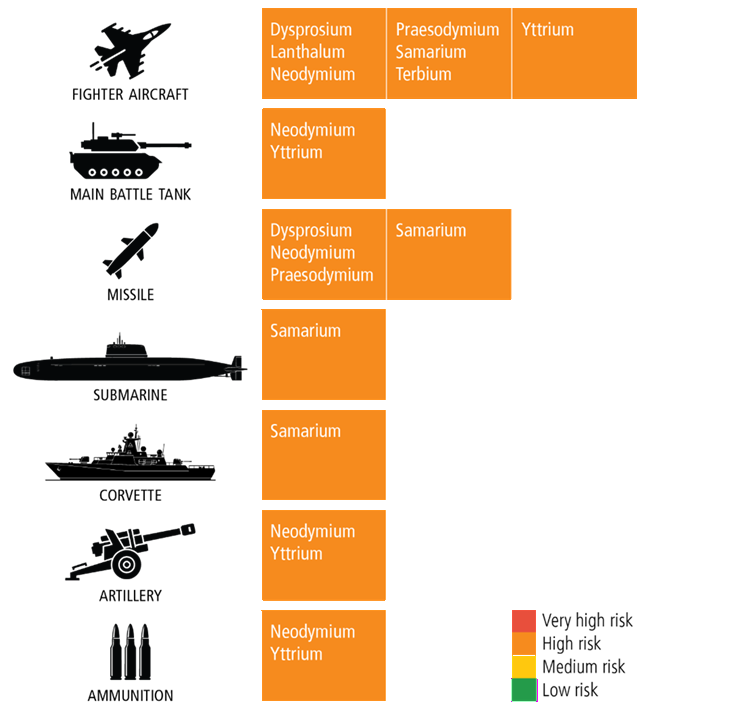

REEs are essential to precision-guided munitions, anti-missile defense, drones, aircraft, naval systems, communications and permanent magnets. For example, an F-35 fighter jet requires over 900 lbs of REEs, while naval vessels necessitate thousands of pounds.4 Rising global defense spending and a shift toward next-generation systems will continue to increase demand for REEs. The Pentagon requires 3,000 to 4,000 tons of highly specialized magnets annually, and projects a demand of up to 10,000 tons by 2030, according to the Commerce Department.5

Figure 4. Rare Earths are a High Supply Risk in Military Applications

Source: Strategic Raw Materials for Defense, The Hague Centre for Strategic Studies, January 2023; https://hcss.nl/wp-content/uploads/2023/01/Strategic-Raw-Materials-for-Defence-HCSS-2023-V2.pdf

REEs are also used in non-magnetic defense functions tied to defense infrastructure and communications, including satellite communications, fiber optic networks, lasers, radar and sonar systems. NATO identifies Rare Earth Elements among its 12 defense-critical raw materials, underscoring their importance to modern defense production and readiness.

Technology

Artificial Intelligence and Data Centers

AI and data center buildout are accelerating quickly. Annual investment grew from approximately $100 billion in 2015 to $500 billion in 2024.6 AI data centers are expected to consume 3% of rare earths by 2030, increasing the price inelasticity of end use.7

Rare earth magnets help keep data centers running cool and reliably. They are used in high-strength magnets that power efficient cooling motors. Hard disk drives used in cloud data centers incorporate REEs to achieve the magnetic performance required for reading and writing data. They are also in parts of semiconductor (chips) production and in key electronic components.

Consumer Electronics

Rare earth minerals are essential in many consumer products, particularly electronics, due to their unique magnetic, luminescent and electrical properties. They are found in smartphones, laptops, LED screens, cameras and electric vehicle motors.

Electric Vehicles and Advanced Mobility

Electric vehicles (EVs) use REE permanent magnets in their electric motors, making them a major driver of demand. In 2024, rare earth demand for EV motors reached 37 kt, up 32% year over year.8 Despite regional slowdowns, mainly in North America, global EV adoption continues to grow. EV sales worldwide grew by over 20% in 2025, reaching 20.7 million.9

Robotics and Automation

Robotics may become one of the largest long-term demand drivers, with humanoids, drones, autonomous systems and industrial robots intensifying magnet demand. Sources estimate that there will be billions of robots by 2050, and the market, now valued at an estimated $3 billion, is projected by Morgan Stanley to reach $357 billion by 2040.10 REEs are critical for advanced magnets to provide the magnetic strength necessary to enable precision movements of robotic arms, hands and actuators.

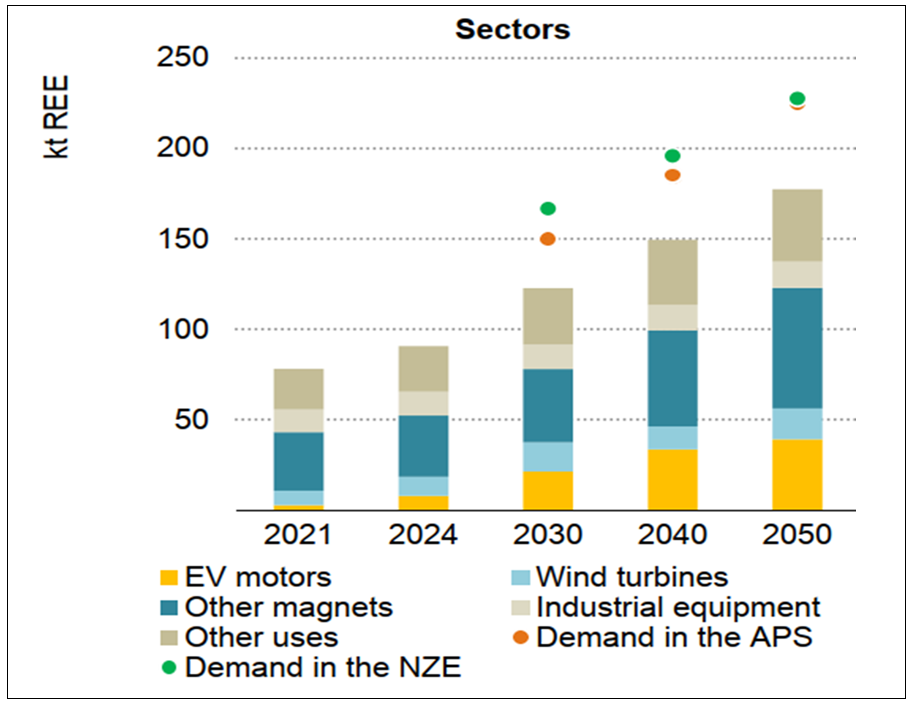

Energy

Electrification and energy security policies will continue to drive structural demand growth in magnet REEs. Under plausible scenarios (such as net-zero emissions by 2050), the IEA Critical Minerals Data Explorer forecasts clean energy demand growth from 2024 to 2050 of:

- Neodymium 320%

- Praseodymium: 318%

- Dysprosium: 353%

- Terbium: 332%

Wind turbines, nuclear power plants and grid systems rely heavily on rare-earth magnets. Magnets are the primary growth drivers for REEs, and total magnet REEs may more than double by 2050, as clean technologies rise from 18% to 42%.11

Wind turbines employ these permanent magnets to enable direct-drive (gearless) operation, reducing mechanical losses, cutting gearbox-related downtime, improving reliability and lowering maintenance costs. In nuclear power plants, REEs provide value in precision, reliability and safety systems, rather than power generation itself. This includes motors, pumps, control systems and instrumentation and monitoring. REE magnets are used in rotating equipment that supports electrical grid stability and voltage stabilization, including condensers, motors and generators.

Figure 5. IEA Magnet Rare Earths Demand Forecasts

Note: NZE represents “net-zero emissions.” APS represents “announced pledges scenario.”

Source: “Global Critical Minerals Outlook 2025”, International Energy Agency (IEA), May 2025. Magnet rare earth elements are neodymium, praseodymium, dysprosium and terbium. The Stated Policies Scenario indicates where the energy system is heading based on a sector-by-sector analysis of today’s government policies and policy announcements; the Net Zero Emissions by 2050 Scenario indicates what would be required in a trajectory consistent with meeting the Paris Agreement goals. Magnet rare earth demand forecast is measured in kt or units of 1,000 metric tonnes.

China’s Dominance Creates Strategic Risk

How China Built Rare Earth Control

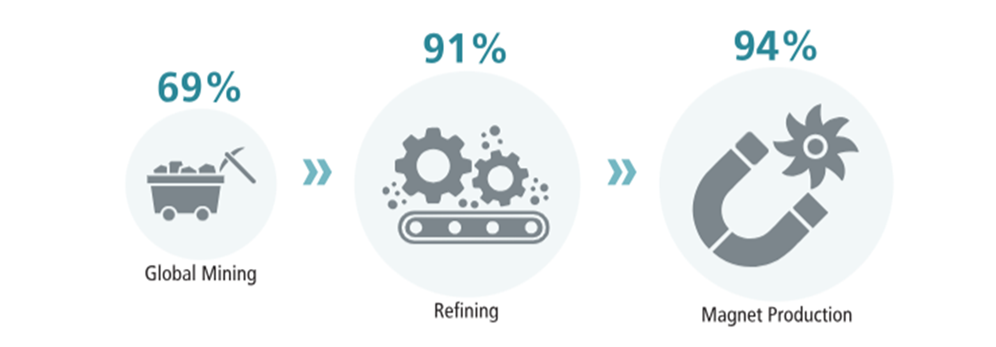

China did not always dominate the rare earths market. In fact, the U.S. led the charge for decades in the 20th century. But once China saw the opportunity in rare earths and replicated the mining process domestically, it established a commanding position. Twenty years ago, China accounted for only 50% of permanent magnet production. Today, China comprises 94% of total production. Additionally, they account for 69% of REE mining and 91% REE refining.12

Figure 6. China Dominates the Rare Earths Supply Chain

Source: Sprott Asset Management.

China’s market leadership was driven more by policy than by geology alone. Over several decades, Beijing built a coordinated, whole-of-government framework that supported production and pricing while deploying supply chain diplomacy to expand overseas mining assets and influence. This approach enabled Chinese producers to scale more quickly and at lower cost than many of their Western counterparts. At the same time, China pursued a sustained consolidation strategy, centralizing control across the sector to reinforce pricing leverage and market power.

Why This Matters

Recognizing their industry dominance and the power they can wield, China began to assert export controls that directly impacted trade. In 2025, China introduced several restrictions that included not only the REEs themselves, but related compounds, metals and magnets. Later in the year, they expanded these to include "internationally made" products containing China-sourced materials or manufactured using Chinese technologies, even if they are traded domestically.13 However, China has since suspended these additional export controls until November 2026.

A Multi-Mineral Chokepoint Accelerates Western Response

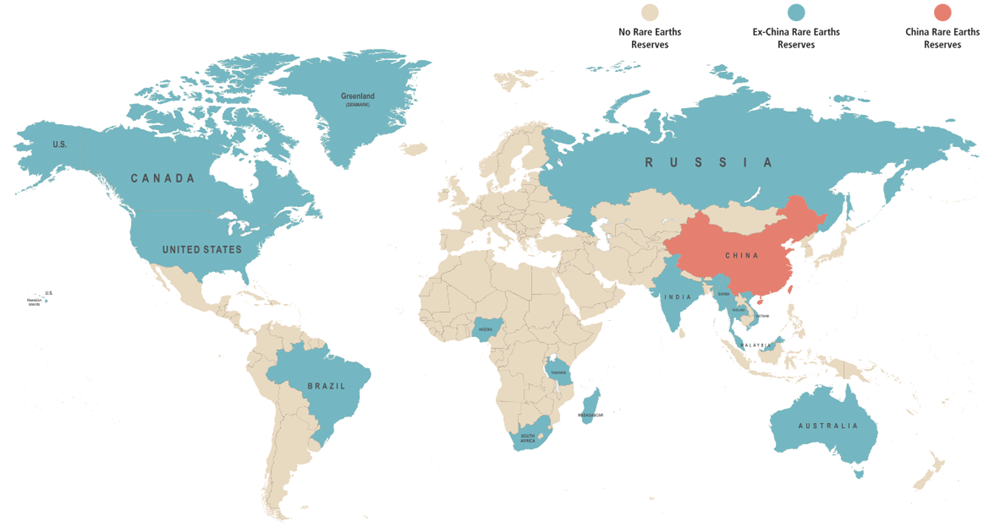

While rare earths are now on the critical mineral lists of most major economies, most countries remain import-dependent and subject to significant supply risks. Increasingly critical to economic prosperity, rare earths now sit at the intersection of defense readiness, energy security and technological competitiveness.

This crucial disruption in the pipeline has prompted countries outside China to join forces strategically. The U.S. is starting by partnering with Australia and Japan, with initial investments expected to exceed $1 billion. These partnerships focus on accelerating, streamlining and deregulating permitting timelines, implementing price floors and establishing strategic stockpiles.

Stockpiles aim to create inventory reserves for use across the countries involved. Price floors are intended to reduce volatility, improve investment certainty and incentivize excess Chinese capacity. The acceleration of permitting timelines will enable these countries to start mining their own REE supply, further reducing dependence on China.

Why Ex-China Rare Earth Capacity Matters for Investors

To diversify away from China, the ex-China market is heavily motivated to build strength and presence. China’s recent export controls triggered a price bifurcation, leading some REEs outside China to trade at several times the premium to China’s domestic market. This price bifurcation creates an opportunity to accelerate ex-China mining, separation and refining capacity.

Additionally, the expansion and leverage of ex-China projects are being supported through government-backed financing. With rare earth reserves distributed across the globe, a more diversified and resilient supply chain is emerging. The U.S. and its allies are investing heavily to secure supply beyond China, creating powerful tailwinds for global producers. U.S.-based entities, including the Department of Defense, have committed billions of dollars to MP Materials14 so far to support buildouts, heavy rare-earth separation, and mine-to-magnet platforms. More investment is planned for building out downstream processing capacity. Australia is also pledging billions to finance its first fully integrated rare earths refinery.

Figure 7. A New Ex-China Rare Earth Supply Chain is Taking Place

Rare Earths as a Strategic Theme

Rare earths have moved beyond mere commodities: they are now strategic geopolitical assets. National security, AI, electrification and defense spending will likely continue to create durable demand.

Nations are rapidly building diversified energy systems, including nuclear and renewables, to insulate themselves from geopolitical, macroeconomic and financial shocks. As deglobalization gains momentum, demand for energy sources other than trade-dependent fossil fuels is increasing.

As countries continue to re-focus their priorities amid shifting economies and ongoing geopolitical challenges, ex-China supply chains will be at the center of policy, capital and strategic objectives. For investors, understanding the importance and value of rare earths means harnessing the future of global power, technology and security.

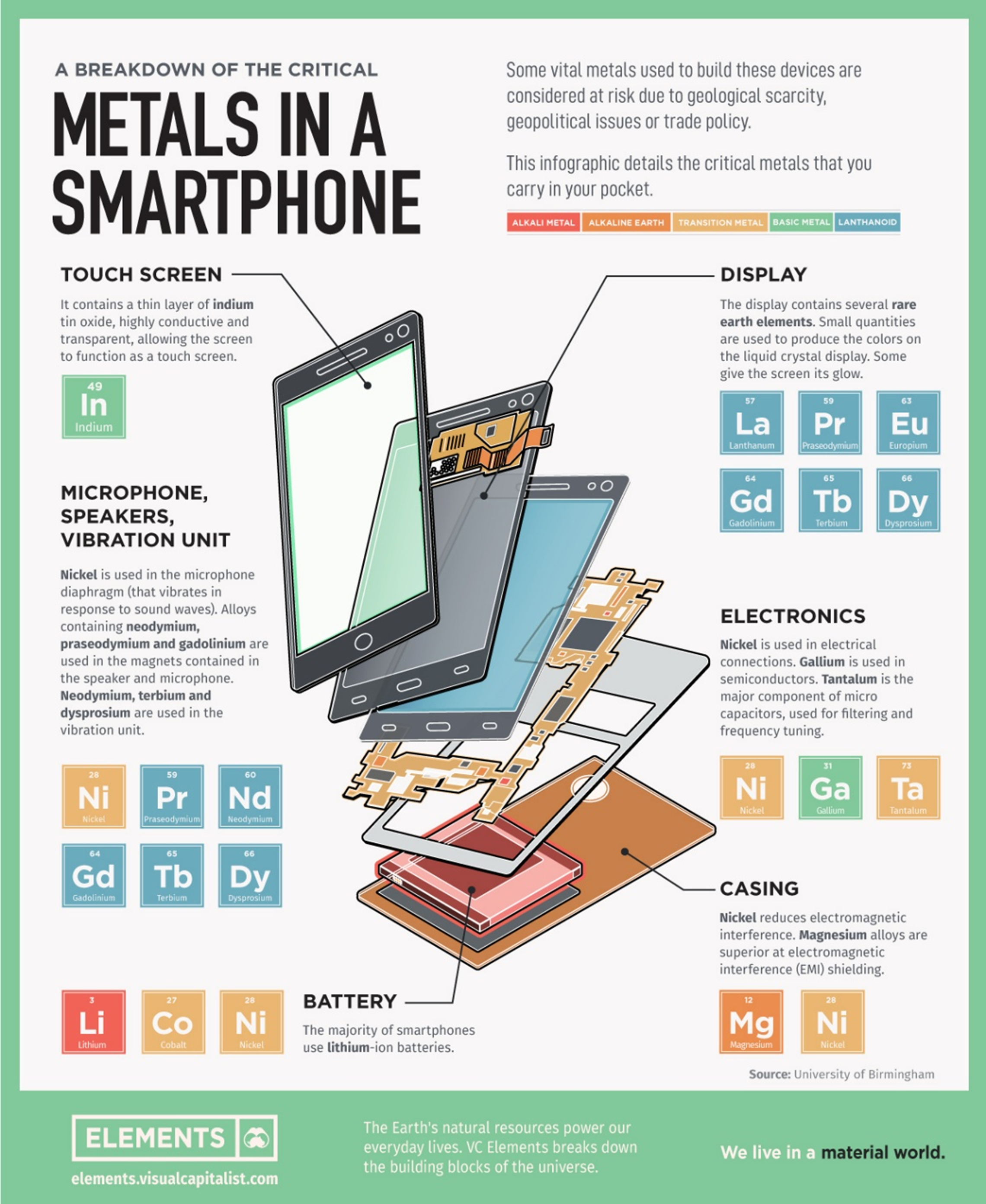

Rare Earths: Power in the Palm of Your Hand

Source: Visual Capitalist. Visualizing the Critical Metals in a Smartphone.

Footnotes

Important Disclosures & Definitions

An investor should consider the investment objectives, risks, charges, and expenses carefully before investing. To obtain a Sprott Rare Earths Ex-China ETF Statutory Prospectus, which contains this and other information, visit https://sprottetfs.com/rexc/prospectus, contact your financial professional or call 888.622.1813. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the funds, typically in blocks of 10,000 shares.

The Sprott Rare Earths Ex-China ETF and the Sprott Active Metals & Miners ETF are new and have limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott Rare Earths Ex-China ETF. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.