Key Takeaways

- Battery Storage Is Essential: As electricity demand grows, battery energy storage systems (BESS) are critical for maintaining grid reliability and supporting renewable energy.

- Lithium Powers the Market: Lithium-ion batteries, especially Lithium Iron Phosphate (LFP) chemistry, dominate energy storage thanks to their safety, durability and cost efficiency.

- Demand Is Surging: Record growth in renewable energy, electrification, AI and data centers is accelerating global deployment of battery storage systems.

- Supply Risks Support the Long-Term Case: Concentrated production, processing bottlenecks and rising demand could make securing future lithium supply increasingly challenging.

The Rise of Battery Storage

Global energy demand is continuing to increase, driven by economic and population growth, electrification and the explosion of artificial intelligence (AI) and data centers.

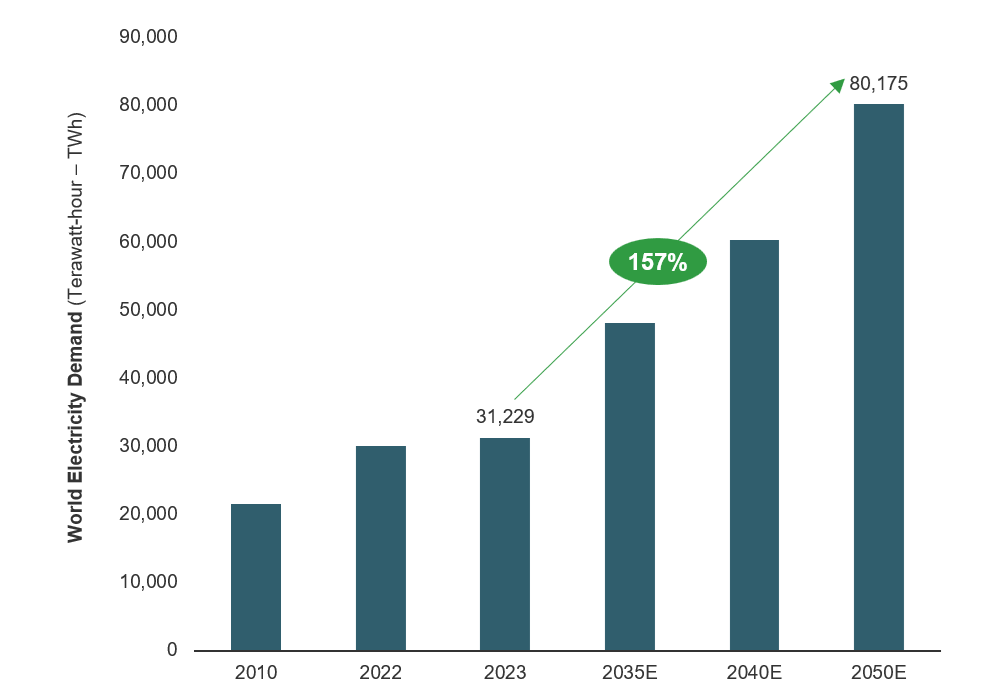

With electricity demand expected to continue to accelerate (Figure 1), maintaining grid reliability is becoming an increasingly complex challenge.1 Geopolitical tensions in the Middle East continue to highlight the vulnerability of global fossil fuel supply chains and underscore the need for resilient energy systems. While renewable energy, such as solar and wind, has experienced continuous growth, these sources are intermittent, creating challenges for balancing electricity supply and demand across the grid.

Energy storage is no longer optional in today’s world; it is essential to a reliable power system.

Battery energy storage systems (BESS) are a critical infrastructure layer that helps meet modern electricity demand. Rather than generating electricity, BESS provides the flexibility needed to balance supply and demand in modern power grids, restructuring how global power grids handle high-demand sectors like AI data centers.

According to the International Energy Agency (IEA), battery storage has become the world’s fastest-growing power technology. Lithium-ion technology currently dominates the global battery energy storage market, making lithium a critical material in today's energy transition. While alternative storage technologies continue to emerge, lithium-based batteries remain the industry's preferred solution for most grid-scale deployments.

Figure 1. Electricity Demand Is Estimated to Increase by 157% by 2050

Source: IEA World Energy Outlook 2025 Net Zero Emissions Scenario.

What Are Battery Energy Storage Systems (BESS)?

As global energy demand enters full swing, the world is experimenting with many forms of energy technologies. The issue with many of these sources is that they are intermittent and sometimes produce more energy than is needed at a given time. Enter battery energy storage systems, which store electricity during periods of excess supply and release it during times of excess demand.

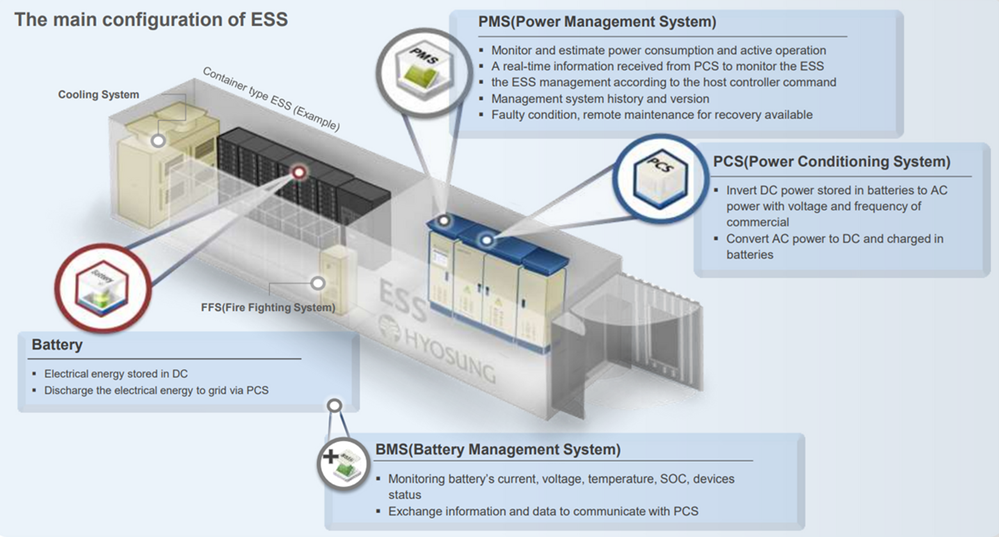

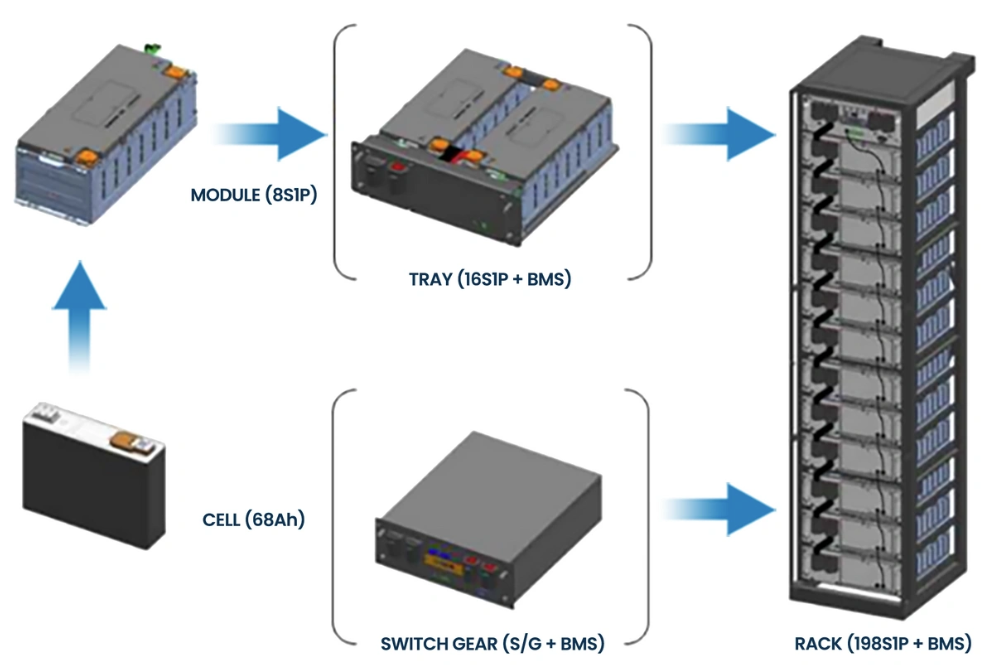

At its core, a BESS converts electrical energy into chemical energy to store it and then reverses the process to release electricity. BESS can range from small portable units to utility-scale structures the size of shipping containers. A standard system includes several integrated parts, as shown in Figure 2.

Many people are familiar with power loss during a favorite show or in the heat of summer, but critical infrastructure, such as data centers, utilities and industrial sites, requires reliable backup power. The core driver behind BESS expansion is the need for grid flexibility and renewable energy integration. Batteries can store excess solar/wind power and release it at peak demand, thereby stabilizing grids and facilitating deeper penetration of intermittent renewables.

Figure 2: BESS Structures

Source: Energy Toolbase, The Primary Components of an Energy Storage System that you Need to Know.

LFP Lithium-Ion Batteries: The Dominant Technology

Since their commercialization in the late 20th century, lithium-ion batteries have become the backbone of modern energy storage, powering everything from smartphones and laptops to electric vehicles (EVs). While EVs have been the primary driver of lithium demand in recent years, demand is increasingly being supported by grid-scale energy storage systems, data centers and commercial and industrial applications.

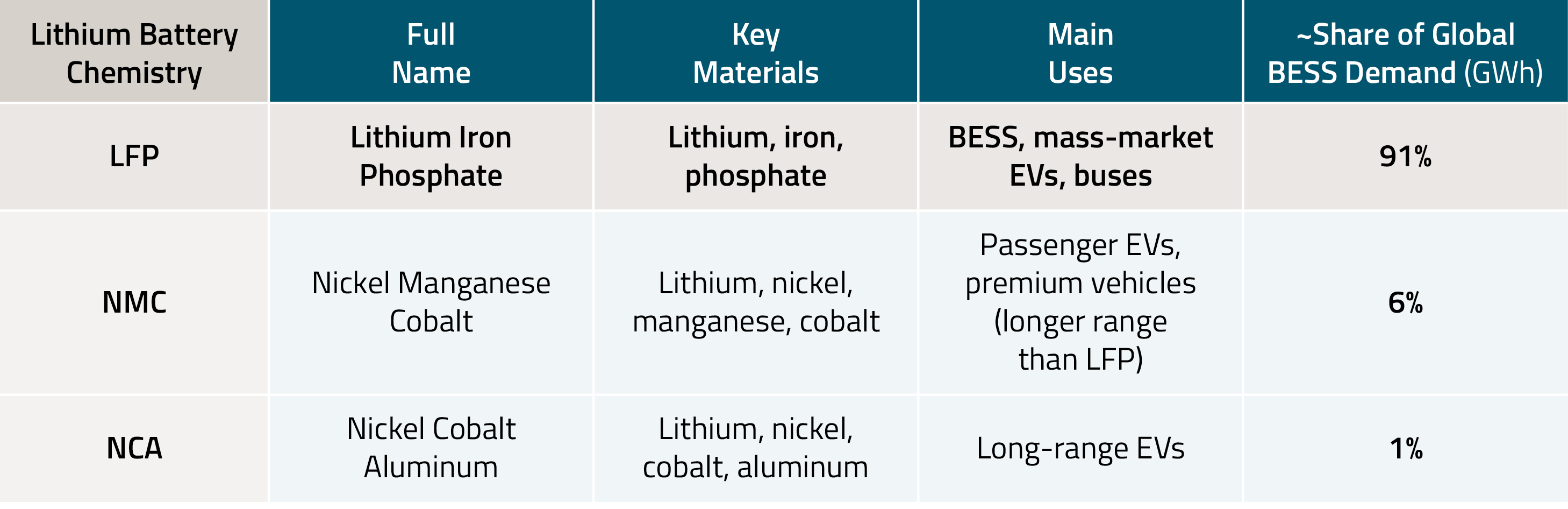

Lithium-ion batteries have emerged as the dominant storage technology as they offer a combination of high energy density, efficiency and scalability. Among the three major commercial lithium-ion battery chemistries, Lithium Iron Phosphate (LFP) has become the preferred choice for BESS (Figure 3). LFP batteries offer a compelling combination of safety, long operating life and cost-effectiveness. Their high thermal stability reduces the risk of fire, while their ability to withstand thousands of charge-discharge cycles makes them well suited to the daily demands of grid-scale storage.

As a result, LFP has become the most widely deployed lithium-ion battery chemistry globally. With EV adoption continuing to grow and grid-scale energy storage expanding rapidly, lithium demand is expected to rise substantially, with EVs and battery storage projected to account for 91% of global lithium demand by 2035.2

In our March report, Lithium Enters a New Era of Strategic Demand and Policy Support, we delved deeper into the rapid growth of BESS and its impact on pricing and demand in the lithium market.

Figure 3. Overview of the Major Lithium-Ion Battery Options

Source: BNEF, Energy Storage Market Outlook 1H 2026: More Records Ahead, 05/06/2026

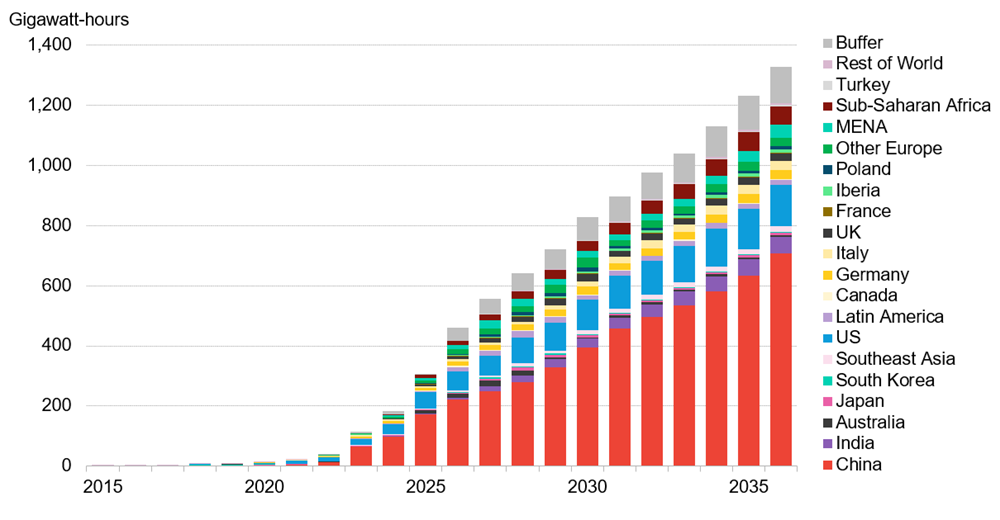

Battery Storage Growth Is Setting Records

The annual rate of BESS deployment is hitting new records every year. BloombergNEF (BNEF) reports 2025 to be another record year, with 112 Gigawatt (GW), or 307 Gigawatt-hours (GWh), of new energy storage additions globally (excluding pumped hydro), which accounts for a 48% surge year-over-year. By 2026, annual global installations could reach 158 GW/459 GWh, reflecting a further 41% growth.3

Figure 4. Energy Storage Hitting All-Time Highs (2015-2035E)

Source: Bloomberg NEF, Energy Storage Market Outlook 1H 2026. More Records Ahead, 5/6/2026.

China and the U.S. dominate the energy storage sector in terms of absolute volumes. China, in particular, has led the recent BESS boom, accounting for 54% of new global storage capacity in 2025.4 Many Chinese provinces had mandated pairing energy storage with new renewable power projects, which spurred huge investments. As a result, China alone deployed 61 GW of battery storage in 2025. The U.S. and Europe followed as the next-largest markets in 2025, each adding tens of GW of storage capacity, while other regions (e.g., Australia, the Middle East, Africa and Latin America) also began to scale up project pipelines. Figure 5 summarizes recent BESS deployment by region and projected growth.

Figure 5. BESS Cumulative Capacity by Region (GW)

Source: Bloomberg NEF.

Energy storage growth is being driven by several factors, including renewable energy expansions, electrification trends and data center demand.

Total global renewable additions reached roughly 800 GW in 2025 (16% year-over-year) with solar surpassing 600 GW of new capacity and wind adding approximately 160 GW globally.5 Global renewable capacity is expected to increase by 4,600 GW by 2030, with solar accounting for 80 percent of capacity growth.6

The rise in EVs, industrial electrification and grid modernization continues to increase overall electricity demand, increasing pressure on the grid and accelerating the need for storage solutions. Finally, hyperscale data centers7 require reliable, high-density backup systems and are projected to grow significantly, from 3,207 in 2026 to 3,558 by 2035.8 Global data centers’ power demand may rise 2.5x by 2030, to a level approximating Japan’s total power use.

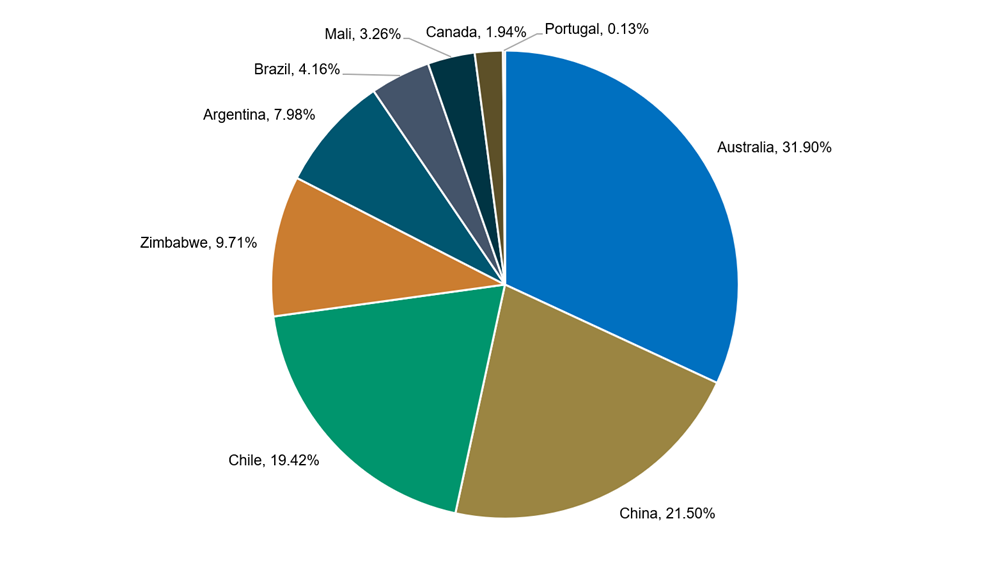

Lithium Supply-Side Constraints

Lithium's concentrated global supply chain is a major driver of risk and opportunity in critical materials markets and energy security. Australia, Chile, China and Zimbabwe account for over 80% of global lithium production.9

Figure 6. Lithium Production by Country, 2025

Source: USGS. https://pubs.usgs.gov/periodicals/mcs2026/mcs2026-lithium.pdf

After it is mined, lithium is processed into battery-grade chemicals, a process in which China currently controls 70% of global refining production. As governments seek to capture more value domestically, limit raw exports and develop full battery supply chains locally, investor uncertainty rises, project development slows and political risk impacts supply.

The rapid rise in lithium demand from BESS comes on top of booming ex-U.S. EV-related demand, raising concerns about whether supply can keep pace. Lithium mining and refining projects face technical and environmental hurdles. If supply expansions lag the steep demand trajectory, lithium markets could experience periods of deficit and price spikes.

The past few years have already seen extreme volatility. Lithium carbonate prices10 rocketed roughly 15× from 2020 to late 2022 amid a supply squeeze, then pulled back sharply in 2023-2025 as new supply became available. Grid-scale storage is broadening lithium demand beyond EVs, and analysts foresee the lithium market swinging from oversupply in 2025 toward a deficit, as rising demand outpaces supply growth.11

BESS Expands the Long-Term Lithium Opportunity

While electric vehicles have been the primary driver of lithium demand over the past decade, battery energy storage systems (BESS) are emerging as an increasingly important source for future growth. Unlike EV demand, which is influenced by consumer spending, economic conditions and government incentives, utility-scale energy storage is driven by long-term infrastructure investment. Utilities, grid operators and power developers plan projects years in advance, creating a demand profile that is often less cyclical and more predictable than the automotive market. As electricity systems become more dependent on renewable generation, energy storage is increasingly viewed as a critical component of grid infrastructure rather than a discretionary technology investment.

The lithium story now extends beyond EVs to the electrification of everything.

The growth potential of battery storage may also be underestimated. Global electricity demand is accelerating due to the electrification of transportation, industrial activity, AI and data center expansion. At the same time, countries are continuing to add record amounts of solar and wind capacity, increasing the need for flexible storage solutions that can balance intermittent energy generation. As grids modernize and a greater share of electricity comes from renewable sources, battery storage deployment could exceed current forecasts, creating an additional source of lithium demand beyond what many market participants have traditionally associated with the energy transition.

Meeting this growing demand will require significant new lithium supply, yet bringing new production online remains challenging. Lithium projects often face multi-year permitting timelines, financing hurdles, technical complexity and processing bottlenecks before reaching commercial production. Although lithium prices have retreated from their 2022 highs, the industry's ability to develop sufficient new supply remains uncertain. As battery storage joins EVs as a major source of lithium consumption, the market's focus may increasingly shift from short-term price fluctuations toward the longer-term challenge of securing enough lithium to support the expansion of global energy infrastructure.

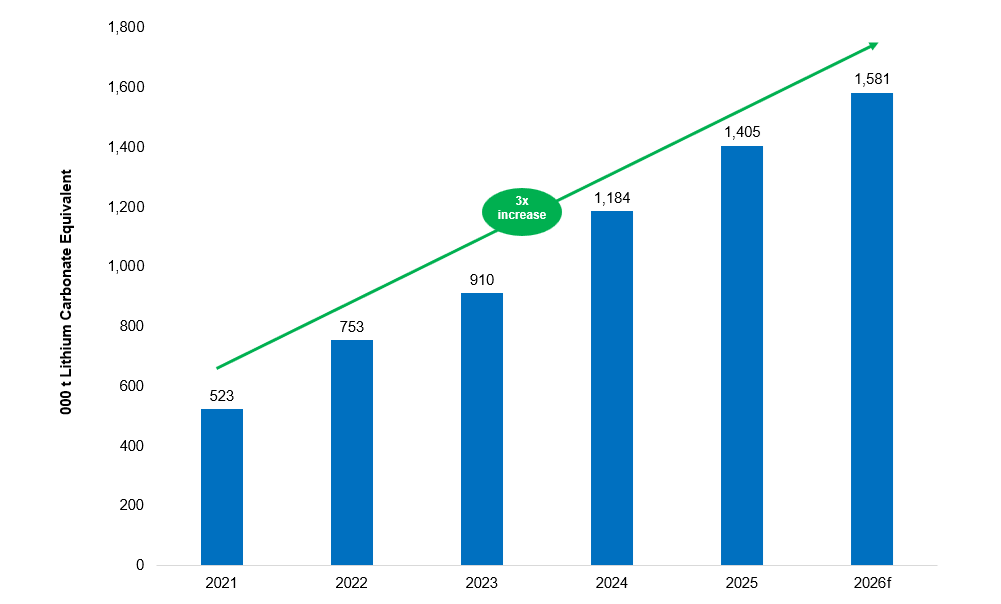

Figure 7: Lithium Demand Continues to Climb (2021-2026f)

Lithium demand is forecast to rise threefold from 2021 to 2026.

Source: Bloomberg. Data as of 6/15/2026.

The Race to Secure Lithium Supply

Governments and corporations are making long-term moves to secure lithium supply, including direct investments, domestic projects and reshoring efforts. Previously funding projects through subsidies, governments have pivoted to direct ownership and financing. The U.S., Canada and the European Union are all undertaking policy changes to reduce their dependence on foreign lithium supply and building local battery ecosystems.

For example, the U.S. government recently took an equity stake in Lithium Americas' Thacker Pass project as part of its efforts to secure a domestic lithium supply. Countries are expected to continue to increase focus on domestic mining, refining and battery manufacturing. Additionally, governments are forming critical materials alliances and bilateral agreements to secure supply. As countries build reserves and prioritize long-term procurement frameworks, lithium is increasingly being treated as a strategic asset.

Lithium Is the Backbone of Energy Storage

For much of the past decade, lithium was viewed primarily as an EV commodity. Increasingly, however, it is becoming a foundational material for electricity infrastructure. As storage systems become a permanent feature of modern grids, lithium demand may be driven not only by transportation but by the global need for reliable power.

Lithium is no longer just a commodity; it's a strategic asset in the race for energy security.

Increased electricity demand and the global energy transition have changed the critical materials landscape, driving skyrocketing demand and prompting countries to secure supply to remain competitive. The market's focus on lithium has expanded beyond electric vehicles to include battery storage and data infrastructure.

Battery storage is a high-growth segment within the energy transition and is critical to enabling a reliable, low-carbon grid. Lithium is enabling this transition and has become the dominant material underpinning battery energy storage systems.

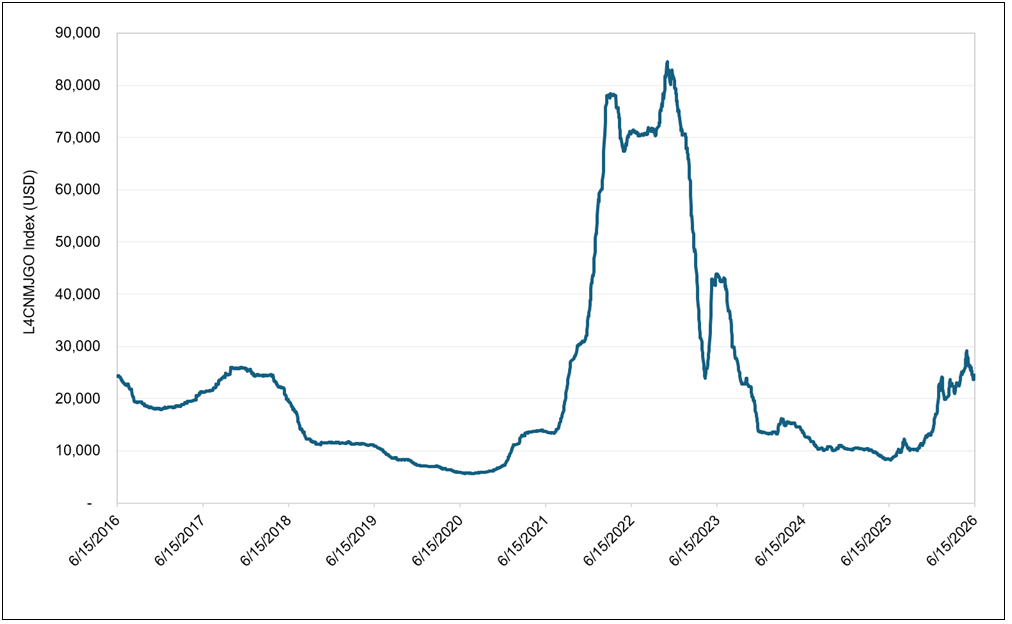

Lithium is in the spotlight given its strong performance over the past year, with the spot price gaining 52.31% year-to-date as of May 31, 2026, and rising 206.58% over the past 12 months. Lithium has entered a new phase where the market is no longer trading on a simple surplus narrative.

Figure 8. Lithium Spot Price Regains Momentum (6/15/2016-6/15/2026)

Source: Bloomberg and Sprott Asset Management. Data as of 6/15/2026. The Lithium Spot Price is measured by the L4CNMJGO Index. You cannot invest directly in an index. Past performance is no guarantee of future results.

In a world where energy security is becoming as important as energy production, lithium's strategic value may ultimately be measured not by the number of electric vehicles it powers, but by the reliability of the grids it helps sustain.

Footnotes

Important Disclosures

Unless otherwise specified, the reader should assume any companies mentioned are not current holdings of LITP.

An investor should consider the investment objectives, risks, charges, and expenses of each fund carefully before investing. To obtain a fund's Prospectus, which contains this and other information, contact your financial professional, call 1.888.622.1813 or visit SprottETFs.com. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

Diversification does not protect against loss. The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the fund, typically in blocks of 10,000 shares.

The Sprott Active Metals & Miners ETF is new and has limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott ETFs. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.