Download PDF of Slide Presentation

In our webcast with Nasdaq, John Ciampaglia discusses the rapid emergence of technologies like AI, the race to upgrade power grids, continuing global decarbonization goals and growing middle classes. He gives an overview of how the critical materials behind energy—such as uranium, copper, nickel, lithium and more—are likely to remain growth-oriented investment opportunities for the long term, and how to invest in them in a single allocation.

Webcast Transcript

Jillian DelSignore: My name is Jillian DelSignore, Global Head of Investor Distribution Strategy at Nasdaq. Thank you so much for making the time to join us this afternoon. I'm pleased to be moderating our discussion, Investing in Critical Materials, with our expert from Sprott, who I'll introduce in just a minute. Before we get started, a few housekeeping items. There are going to be materials at the bottom of your console that you can access during and after the presentation today. You're going to find a PDF downloadable version of the presentation that John goes through and information on SETM, the ETF that he'll discuss as we get to the end of the discussion this afternoon.

There's going to be a survey after the webcast that we encourage you to participate in. Your feedback makes the events that we do that much better. We would appreciate the few minutes you took to take the survey this afternoon. We only have 30 minutes today, but we are going to do our best to take questions from you as we get to the end of the prepared comments, so please use the Q&A box if you have a question. If we don't get to your question today, someone from Sprott will follow up with you directly following the event. With that, let me go ahead and introduce our speaker today, John Ciampaglia, the CEO of Sprott Asset Management. John, welcome. Thanks for joining us.

John Ciampaglia: Thank you for hosting this event.

Jillian DelSignore: Absolutely. Why don't we go ahead? I'll let you kick us off and give us an overview of who Sprott is and who Sprott Asset Management is.

John Ciampaglia: Sure. Why don't I jump into the presentation? Sprott's been around since 1981. We have offices in Canada and the U.S., and I think we're best known for our expertise in all things related to metals and mining. That's our core competency. We're essentially a boutique asset management shop, and what's unique about Sprott is that we're also publicly traded on the New York and Toronto stock exchanges.

It's not always common for small boutique shops to be publicly traded, but I think it provides our clients with a lot of transparency about who we are and what we do. Our focus is on metals and mining. We do everything from physical commodities, covering gold, silver, platinum, palladium, copper and uranium. We do passively managed ETFs related to mining equities. We do active mining equities and private investments in the mining space related to mine finance, so private credit, debt, royalties, and streams.

If it has anything to do with mining, there's a pretty good chance we're involved somehow. I think that's important because we put much of that experience and expertise into developing our products, whether they're passively designed and rules-based or actively managed and specialized strategies. I think this gives us an advantage over the more generic supermarket firms, and we're very proud of our partnership with Nasdaq, which has helped bring many of these ETFs to life with its indexing expertise.

Let's get into the topic of critical minerals and materials today. People might be saying: well, what does that mean? It refers to a number of different minerals that are very important to a number of different technologies. There are a number of them that we've identified in the last few years that we think will grow in importance, mostly related to energy generation, transition, transmission, and energy storage, which is another way of saying batteries.

Interestingly, yesterday, the Harris presidential candidate announced as part of her platform that they would be looking at building strategic reserves of a number of critical materials, including things like cobalt and nickel, because of this push to reduce reliance on Chinese supply chains, which for many of these critical minerals they control. I think this has become a very interesting element of the investment thesis over the last two years, particularly since governments around the world are becoming increasingly concerned about over-reliance on nations with whom relationships over the last couple of years have become more tense. I'll get into that in a bit more.

Today, we will talk a little bit about what's driving all of this, including some of the technologies and growing energy needs around the world and how critical minerals fit into all of that. It's about surging energy consumption, and energy, according to this definition, really refers to electricity. And I'll give you some stats here. The U.S., in particular, is starting to grow its electricity demand, which has not happened in the last 20 years. If you consider all the energy efficiencies engineers have created over the last few decades, we haven't had an incremental electricity use for two decades. That's starting to change.

It's being driven by several factors. First and foremost, there is the reshoring of much manufacturing, in part because of the shift away from China. This is happening in semiconductors, electric vehicles, batteries, solar panels, and many new energy technologies in manufacturing. It's also happening because of increased demands being put on the grid from AI data centers.

The primary driver is from places like India and China, which still consume much lower levels of energy per capita than we do in the West. As they urbanize and people consume more electricity by buying their first air conditioner and washer and dryer, it's creating unbelievable demand for electricity. It's primarily driven by the East, but in the West, we're starting to see this shift returning to higher demand because of emerging technologies and clean energy. It's putting a lot of demand on these critical minerals.

Energy is key. If you look at the correlation between electricity consumption and GDP or income per capita, no poor country in the world consumes high amounts of electricity. There's a strong correlation between energy consumption, electricity consumption and overall wealth. As countries like India, China, and other emerging markets become wealthier, they are putting more and more demand on overall electricity. Part of electricity comes from traditional forms like coal and natural gas, but nuclear power has been a big part of the story for the last three years, and we've been talking about this very actively in the marketplace.

Many countries look at nuclear power for reliable base load power and clean energy. China is leading the world in terms of building out capacity. They have plans to build between four and six new nuclear reactors every year for the next 10 to 15 years. Just to put that into perspective, the U.S. has built two new reactors in the last 30, so a lot of the growth is being driven by China as it's trying to expand its electricity grid and reduce reliance on coal, which we all know is a dirty form of energy.

In the last two years, many countries that were previously on the path of phasing out nuclear power have shifted back to nuclear energy because it provides very reliable baseload power and energy security, which is becoming a new theme, much like it did in the 1970s.

The other key element that we're going to talk about is copper. Copper is the go-to material if you think about how we move electrons around. Copper is used for many industrial applications, but its usage is starting to skew higher toward energy transmission. That's everything from electrical grids, charging electric vehicles, batteries, solar farms, and wind farms. All of these things need to be wired into the grid, and the more recent application that copper is getting a lift from is its preference in AI data centers, which produce a lot of heat, which has to be dispersed. Copper is very effective in electrifying these data centers.

This has been topical for the last few months. There were a couple of interesting developments last week. In particular, Microsoft announced a deal, a power purchase agreement with the utility in the U.S. called Constellation Energy. Constellation is the largest provider of nuclear power in the U.S., and they just signed a 20-year power purchase agreement, which entails restarting a nuclear power station that has been turned off for the last five years. Microsoft has signed this deal with consolation Constellation because it needs reliable baseload power to power these data centers.

These data centers are very different than typical data centers. If you think about a data center that, say, Google is operating to store photos in the cloud or to do some online search, when you compare the power usage of one of those, compared to AI, it's about seven times more intensive. There is a race going on right now to build out AI. It is happening on a global basis. These data centers require a lot of power, and you're seeing that the utilities are struggling to generate a lot of extra power because the grid hasn't called for it for the greater part of 20 years.

Many of these technology companies, which are very deep-pocketed, whether it's Google, Microsoft, Apple or Meta, are solving the problem themselves. They're signing long-term power purchase agreements with the likes of Constellation. Microsoft also did a very large deal with Brookfield Renewable Energy a few months ago to source clean energy. We also recently saw Amazon Cloud Services buy a data center co-located right next to a nuclear power station in Pennsylvania so they could draw the power from the power station to the data center. This will be a new theme or driver of demand for renewable energy technologies and nuclear power. And copper is obviously the key element tying it all together.

This is the story I mentioned about Amazon buying the nuclear power data center from Talen. You can see this idea of co-location. This is very interesting because what the technology companies are quickly figuring out it's a two-stage problem. You have to source the electricity. You also have to have the grid to connect to your data center. In the U.S., building new transmissions, which are new high-voltage transmission lines, can take up to 15 years between all the permitting and legal fights that tend to come with it.

You're starting to see a lot of co-location, which means you co-locate what you need the energy for right next to the source of the energy. We think this is going to be a very popular theme. You're seeing a lot of strategic land purchases next to existing power stations as data centers want to build right next door to remove that obstacle to transmission.

Let's talk a little bit about the world's shift to cleaner energy. Everyone would prefer more energy and clean energy if it's possible. It depends on what resources a particular country has or its utility. We're not suggesting that the world is moving away from fossil fuels anytime in the foreseeable future. Still, we think investments in cleaner technologies are growing disproportionately as the world focuses on cleaner technologies. To put that into perspective, what was really interesting is in 2022, for the first time ever, the investment dollars that went into clean energy technologies matched the annual investment made in fossil fuels for the first time in history.

This is being driven by a lot of government incentives. That's happening in the U.S. through a number of bipartisan bills that have been in place for the last two years. It's also happening in the European Union that they're trying to crowd in private capital using public incentives, whether those are tax credits, investment credits or even, in some cases, loans. The Department of Energy has a large amount of capital that it can disperse to companies to help further new technologies or, in some cases, develop things like lithium mines in Nevada. We think this trend is not going away, and we believe it will continue to grow.

As I mentioned, the Inflation Reduction Act, which you know is probably one of the worst-named pieces of legislation, is a clean energy bill. As I mentioned, there are many different elements of this to incentivize investments in a number of different technologies. A lot of this is about funding clean energy. Still, a lot of this is also about reducing reliance on China, which has become incredibly dominant in many different supply chains. Irrespective of who gets into the White House next year, we think a lot of these bills, which were bipartisan supported, will continue to support a lot of these industries and national security-type initiatives.

Let's tie it back to critical minerals. How does this all tie back into minerals? Well, as you can see, these different technologies are very mineral-intensive. If you think about nuclear energy, the primary mineral we're talking about is uranium. Electric vehicles are very mineral-intensive, and so is solar power. Electricity networks are all about copper and aluminum and, to a lesser degree, wind power and hydropower. These are putting new demands that nobody would have anticipated three, four or five years ago. We think these are long-term secular trends that are going to be in place for a decade or two.

EVs are a big story, and yes, we acknowledge that there's been a slowdown in sales in the U.S. and the European Union. I think part of that is because interest rates have made the cost of buying new vehicles more expensive. If you look at markets like China, which are really leading the world, over 50% of all new car sales are now categorized as new energy vehicles.

What is a new energy vehicle? That's a fully electric car, a plug-in hybrid electric car, or a hybrid car. All of these types of vehicles are very mineral intensive in the batteries. They use cobalt, manganese, and nickel. And Lithium is the primary electrolytes for all these different battery chemistries. Generally, we think the trend is up here in terms of EV adoption. We've had a slowdown, but we believe more and more EV vehicles will be on the road as the costs come down.

Why is it having a direct impact on some of these minerals? As I mentioned, they're much more mineral-intensive than a traditional internal combustion engine vehicle. You can see here the amount of minerals in kilograms. If you multiply each amount by 2.2, you'll get pounds. There's a lot more copper and things like manganese and nickel, creating new demand sources for many minerals that didn't exist five years ago.

Uranium has been a very successful investment for our clients in the last three and a half years; the price of uranium has gone from around $30 a pound to about $82 a pound in the last three years. Many countries have driven this shift back to nuclear power. What you're seeing in the U.S. are power stations scheduled to close, such as Diablo Canyon in California; governments have said there's no way we can turn these power stations off. We risk brownouts, which nobody wants to deal with.

You have power stations that have been turned off for two and five years and announced they will be turning back on with refurbishment. You're starting to see governments worldwide make investments in life extensions and grant longer operating licenses to many of these power stations. Japan is slowly restarting many of the power stations they have had turned off, creating a lot of future demand for uranium. The world produces about 150 million pounds of uranium right now, and the annual needs globally are about 180 million pounds, and that number only goes up.

The World Nuclear Association estimates that by 2040, the industry will consume 300 million pounds of uranium. That means the industry needs to figure out how to double production between now and 2040. It's a very big challenge. We have not developed a lot of new uranium mines because we were in a 10-year bear market. Still, the uranium price moving from $30 to $80 has acted as a very strong incentive and catalyst to restart many of these mines that were on care and maintenance for a number of years, as well as help finance the building of many new mines, and that's directly helping a lot of these uranium mining stocks, which have performed very well over the last five years.

We think this trend is quite durable. China is the backbone since they are building four to six new reactors yearly. India is another big build-out that will be happening, but countries like South Korea have also signaled they will be building more reactors. It's hard to know whether the U.S. will build more reactors after the last two. Still, we think utilities clearly realize they need to expand their grids. Governments are providing the right incentives to help accelerate that process, whether through regulatory approval processes, which in the past have been very onerous, and helping the permitting process for new transmission, which is very important for a whole host of different energy generation technologies.

Even though uranium has moved significantly over the last three years, we think there is more potential for the price to increase and further incentivize the doubling of production that we will need over the next fifteen years.

On copper, it's a very similar story. Copper is a very important mineral, and we've been mining copper for 5000-plus years, so we know how to do it well. There are lots of deposits around the world. The challenge is it's getting harder and harder to find high-grade, large deposits of copper because all of the easy stuff has been mined. You're finding that we haven't built many new copper mines in the last ten years. Many existing mines are getting a little bit towards the end of life. Many new deposits have ore grades substantially lower than where we were 20 or 30 years ago.

That will pressure the price of copper. That's starting to happen, and there's been a lot of M&A activity in the copper sector, some of it friendly and some hostile in the last two years. It signals the strategic importance that some of the world's largest mining companies in the world are signaling with respect to copper. For example, BHP, the world's biggest mining company, recently went hostile after another mining company with a diversified portfolio of mines, and they were really after the copper portfolio.

BHP has also made many friendly copper acquisitions in the last couple of years at very good premiums. Even gold companies like Barrick are starting to reposition their portfolio and their strategic focus on more copper. This is interesting, and the reason is very simple. They see the challenges with new production and finding new deposits and know the expected demand over the coming years. I think it's fair to say the copper market this year is in balance, but if these technologies continue to scale as anticipated, we will see supply deficits.

The other interesting thing is that these copper companies are opting to do M&A transactions rather than building new mines because the copper price right now, around $4.40 a pound, is still not high enough to incentivize them to spend the billions of dollars required to build new copper mines. Many of the copper CEOs have signaled that they need to see prices in the five to $6 a pound range before making these very large choices. I think the future for copper is very bullish.

Lithium is another one. It's a more nascent industry because prior to five years ago, with the introduction of electric cars, there weren't many applications for lithium. Lithium is the key electrolyte for every battery chemistry. Whether you're a nickel manganese cobalt-based battery or a lithium phosphate ion battery, which are the dominant forms in China, we need to produce a lot more lithium.

There are significant lithium deposits around the world, and right now, China controls about 80% of this supply chain, not the production of lithium, but the processing: turning lithium from its base form into a chemical form that is ultimately applied to these different batteries. The U.S. is very focused on this. There are a number of very large lithium deposits in the state of Nevada that the Department of Energy would like to see built, and the Department of Energy has extended several multi-hundred-million-dollar loans to these companies to help bring these mines to production.

Right now, the lithium market is somewhat out of balance, meaning there's an oversupply as new production has come online. A lot of that has come from China, which has been flooding the market with lithium. The market will find its footing, but in the longer term, we think lithium will see a lot more demand.

Jillian DelSignore: John, may I jump in for a quick second? This has been great, and maybe as a bit of background, you talked about Sprott like this is all you all do. Hearing about this and hosting another webcast with one of your colleagues makes so much sense looking at the long term. Where is the puck going in terms of how we're allocating? It also feels tricky from an investment perspective, so I think it's a perfect segue into, "How do we access this?" Right? How do we access the metals? Is there a way we can access the whole theme? How do you all think about creating products to capture this for investors?

John Ciampaglia: It's a great question, and it's something we think very carefully about because you're right: whether you're a sophisticated institutional investor or a do-it-yourself investor, this is a technical topic. Many of these mining companies are in very different stages of development. How do you analyze them? Do you want to spend the time and effort doing that? Or do you want to use ETFs as a popular way to gain exposure to the theme?

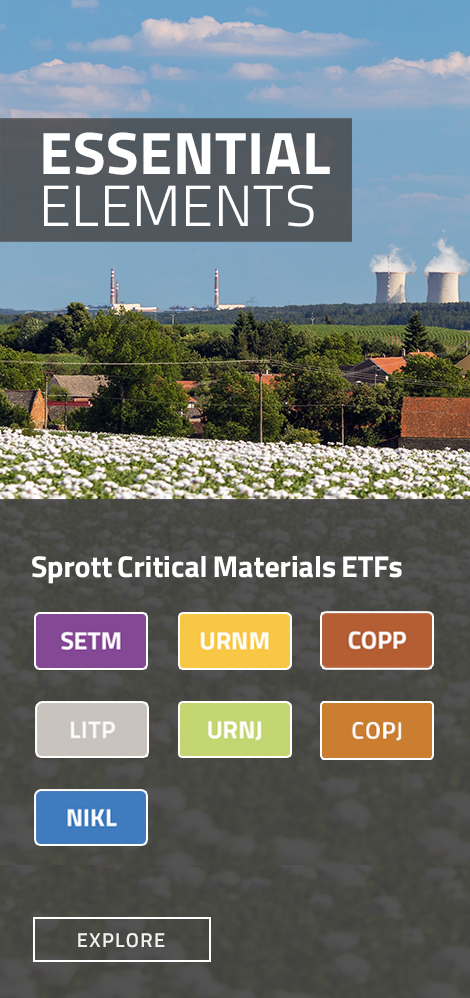

That was the catalyst for our launch of a number of uranium funds. We broaden that to a broader suite of minerals that includes copper, lithium, nickel, and then a diversified all-in-one solution that we'll discuss in a minute. That allows investors to gain exposure to a broader basket of these metals. I think the key takeaway I would leave with people is that while the ETFs we have are rules-based and passively managed, we at Sprott play a key role in the development of the indexes with Nasdaq. We have a contribution arrangement with them, where we do a lot of the upfront building of the initial investment universe to score the companies.

One of the big challenges is a lot of these companies have multiple exposures to metals. If you're going to own BHP, what do you own? Well, you own an iron ore company with some copper exposure and some uranium exposure. What we've done in that universe construction's first step is go company by company and first determine what exposure I get from these companies in terms of their revenue streams and/or their asset bases.

That's a lot of work. We do that every six months. We re-score these companies to help provide that pure-play exposure. If you're really trying to get exposure to energy transition materials, you don't really want exposure to iron ore, which is hugely economically sensitive to things like the Chinese economy, which right now is kind of sputtering. We've tried to put our knowledge as active managers into designing these indexes in partnership with Nasdaq.

We've created a whole suite. We sometimes find investors want to express their view or their thesis with a specific metal because they've done a lot of research into one. Or, in the alternative cases, they don't want to pick a particular metal. They'd rather take a diversified approach, and that's the Sprott Energy Transition Materials ETF,* which gives you exposure to a number of different minerals. Maybe I'll just show you the snapshot of what that looks like.

For example, today's fund is about a quarter of copper equities, about a quarter of uranium-related equities, and a little under a quarter in lithium. Then you've got rare earths used for permanent magnets that go into electric vehicles and wind turbines. Silver, you may be wondering why silver is in this. Well, about 20% of all the silver in the world is consumed by solar panels. Silver is hugely conductive, excites the electrons in the solar panels and makes them more energy efficient. We're seeing more silver consumed for things like solar panels.

Nickel is important for batteries, specifically nickel-based batteries, which are the dominant chemistry in, say, a Tesla or some Western-based carmakers. Manganese is another key metal for batteries, etc., and graphite. We tried to give people exposure to the metals that we think are going to be the primary beneficiaries long term, but it's a dynamic process.

Every six months, these indexes get rebuilt from scratch. We're looking at each company, how it's evolving, and how its exposures change. There's a lot of M&A activity going on right now in the space. Many mining companies are also spinning off assets because they know that copper-related assets, for example, carry much higher valuations than, say, iron ore-based assets. There's a lot of activity in the space, and I think having an index that's moving with the market is important. Let's open it up to some questions.

Jillian DelSignore: Well, we're at time. I don't know if we'll have time to answer any questions, but I was going to say, why don't we land on the sales team? Because I was going to say, if you did put a question into the Q&A box, which we do have a couple of, you can see that Sprott does have a set of salespeople that will be able to reach back out and contact you directly to answer the questions that you had. John, that was fantastic. As I mentioned, this is the core of what Sprott does. I can't think of a better person to be here and educating us today on why and how it's important to think forward, including things like this in a portfolio, but also how to access it through your products.

Thank you for the time and the education, and thank you, everybody, for the time this afternoon. We look forward to having you on the next webcast.

John Ciampaglia: Thanks very much.

*Please note: Effective October 1, 2024, Sprott Energy Transition Materials ETF will change its name to Sprott Critical Materials ETF. The Fund’s underlying index, the Nasdaq Sprott Energy Transition Materials Index will change its name to the Nasdaq Sprott Critical Materials Index. The Fund's investment objective and ticker, and the Index's selection methodology and ticker will remain the same.

Important Disclosures

An investor should consider the investment objectives, risks, charges and expenses of each fund carefully before investing. To obtain a fund’s Prospectus, which contains this and other information, contact your financial professional, call 1.888.622.1813 or visit SprottETFs.com. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

Diversification does not protect against loss. The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the fund, typically in blocks of 10,000 shares.

The Sprott Active Metals & Miners ETF is new and has limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott ETFs. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.